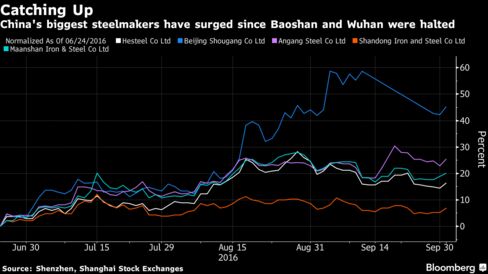

The listed units of Shanghai Baosteel Group Corp. and Wuhan Iron & Steel Group Corp. rose by their daily limit after resuming trade on Monday, playing catch-up with rival Chinese steelmakers that had rallied during their halt for merger talks.

Baoshan Iron & Steel Co. surged 10 percent in Shanghai to 5.39 yuan a share, from 4.90 yuan on June 24, its last day of trade before a halt as its parent entered talks to create China’s biggest steelmaker. Wuhan Iron & Steel Co., the listed unit of Baosteel’s acquisition target, also gained 10 percent.

The companies’ shares are resuming after a period in which steel prices rose in China, pushing up valuations. Hesteel Co., the listed unit of China’s top steelmaker currently, has gained 16 percent in Shenzhen since June 24. Maanshan Iron & Steel Co. Ltd., listed in Shanghai, is up 20 percent, while the Shanghai Composite Index has advanced 6.5 percent.

China’s government approved the merger of Baosteel and Wuhan Steel as part of reforms to reshape heavy industry as it battles structural oversupply and dwindling profits. The merger is the biggest in a decade for the global steel sector and a big step for China’s long-stated goal of bringing together the country’s largest mills. Baosteel’s listed unit is taking over Wuhan Steel’s listed subsidiary in a deal whereby each Wuhan share will be swapped for 0.56 shares in Baoshan.

Baosteel’s higher profitability versus its target brings “material dilution risk” for Baoshan shares in the short term, analysts from Goldman Sachs Group Inc. said in a note on Sept. 23. Wuhan Steel’s higher debt-to-earnings will weaken Baosteel’s financial capacity and is credit negative for the acquirer, according to Moody’s Corp. Standard & Poor’s placed Baosteel on the watch for a credit downgrade after the tie-up was announced.

Recent Articles on M&A

Source: Bloomberg.com