With an ambitious vision to achieve ₹50,000 crore in revenue by 2030 across its automotive and non-automotive segments, the Anand Group is taking decisive steps to streamline and scale its operations. The consolidation of its privately held automotive businesses under the umbrella of Gabriel India Limited—its listed arm—forms the cornerstone of this transformation.

Anchemco India Private Limited (the “Transferor Company” or “Anchemco”) is engaged in the manufacture and supply of brake fluids, radiator coolants, diesel exhaust fluids (DEF) / ad-blue, and products include Polyurethane (PU) and Polyvinyl Chloride (PVC) adhesives primarily for filtration products and sound insulation applications. The registered office of the company is in New Delhi. Anchemco is in the process of shifting its registered office to Maharashtra to align with the registered office of other involved companies. The entire share capital of Anchemco is directly and indirectly owned by Asia Investment Private Limited.

Prior to this scheme, Business of Anchemco Anand LLP was transferred to Anchemco India Pvt Ltd via slump sale on August 08, 2023. Further, Ansysco Anand LLP was merged with Anchemco on April 01, 2025. Anchemco was incorporated in 2022, all the current business of Anchemco can be attributable to transferred businesses.

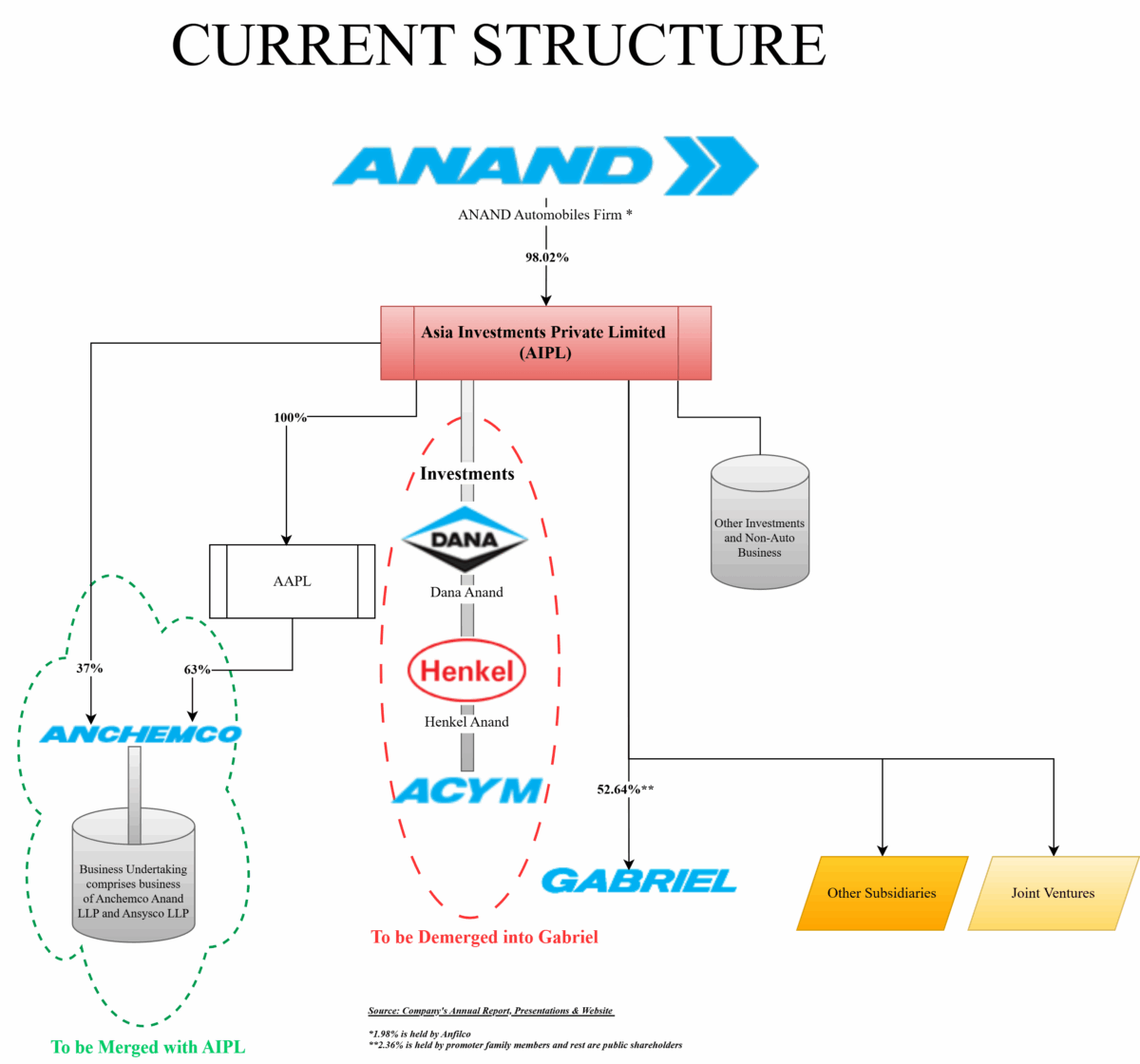

Asia Investments Private Limited (the “Transferee Company” or “Demerged company” or “Asia Investment” or “AIPL”) is primarily engaged in making investments in subsidiaries / joint ventures and providing management advisory services. The company is a non-registered Core Investment company. The company is entirely owned by Anand Group and holds 52.64% stake in Gabriel India Limited and other key entities of Anand Group. The registered office of Asia Investment is in Mumbai. Other key entities of the Anand Group owned by Asia Investment Private Limited, of which the investment shall transfer to Gabriel India Limited as a part of the proposed demerger, are:

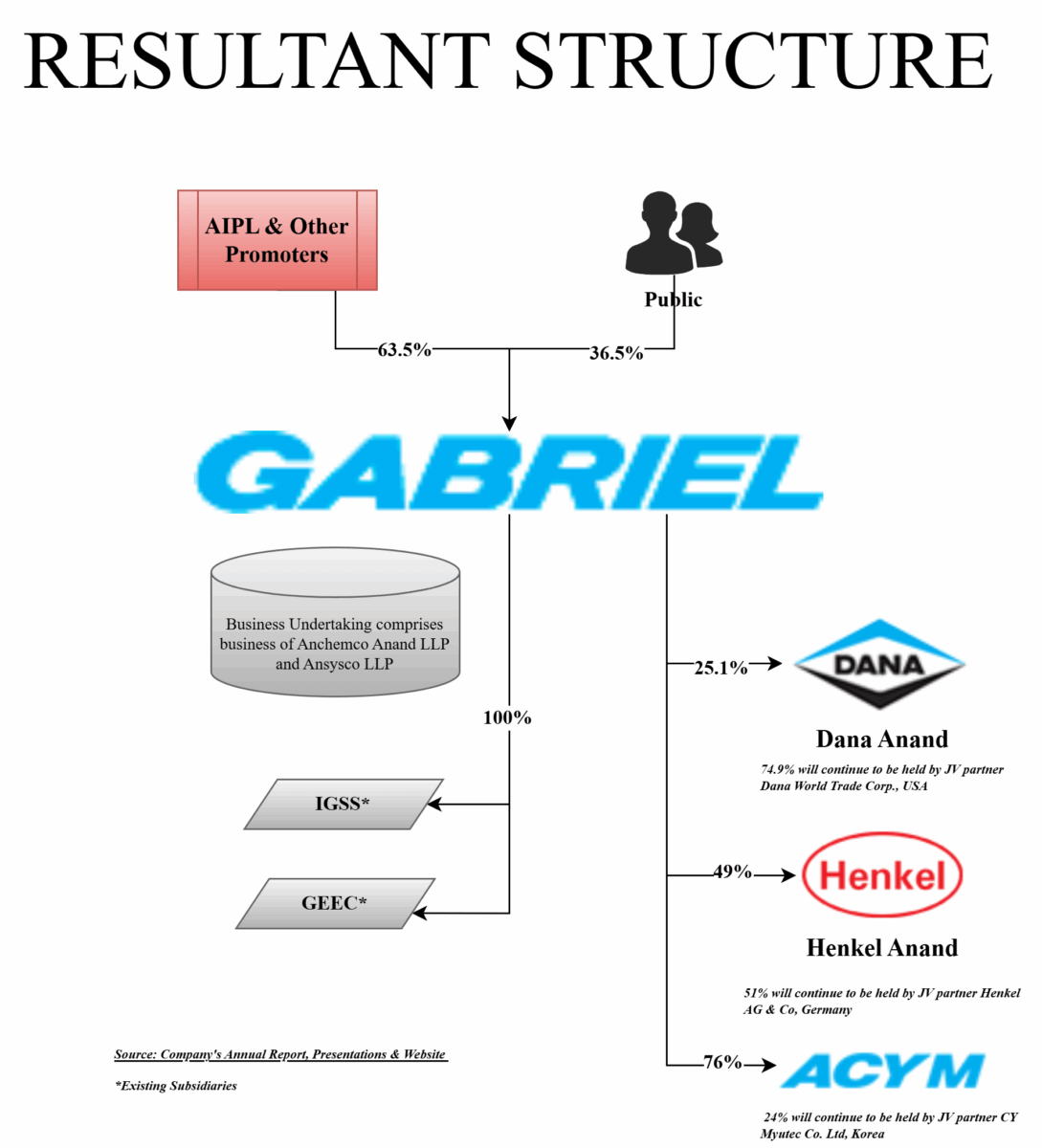

Dana Anand India Private Limited: Dana Anand India Private Limited is a joint venture between Dana Inc. and the ANAND Group. It is a global leader in designing and manufacturing drivetrain products, including transmissions for EVs, for the OEMs of utility vehicles and commercial vehicles, off-highway, EV’s, and the related aftermarket segments. Asia Investment owns 25.1% stake in this company while remaining stake has been held by Dana group.

Henkel ANAND India Private Limited: Henkel ANAND India Private Limited is a joint venture between ANAND Group and Henkel KGaA (Germany) and is a leading supplier of BIW (body in white) and NVH products and solutions to every major OEM in country. Asia Investment owns 49% stake in this company while remaining stake has been held by Henkel Group.

ANAND CY Myutec Automotive Private Limited: ANAND CY Myutec Automotive Private Limited is a joint venture between ANAND Group and CY Myutec engaged in the manufacturing of brass and steel automotive synchronizer rings and aluminium forgings. Asia Investment owns 76% stake in this company while remaining stake has been held by CY Myutec group.

Gabriel India Limited (the “Resulting Company” or “Gabriel”) is engaged in the business of manufacture and distribution of ride control products catering to all segments in the automotive industry. The equity shares of the Resulting Company are listed on BSE Ltd and National Stock Exchange of India Limited. The registered office of the company is located in Pune.

The Proposed Transaction

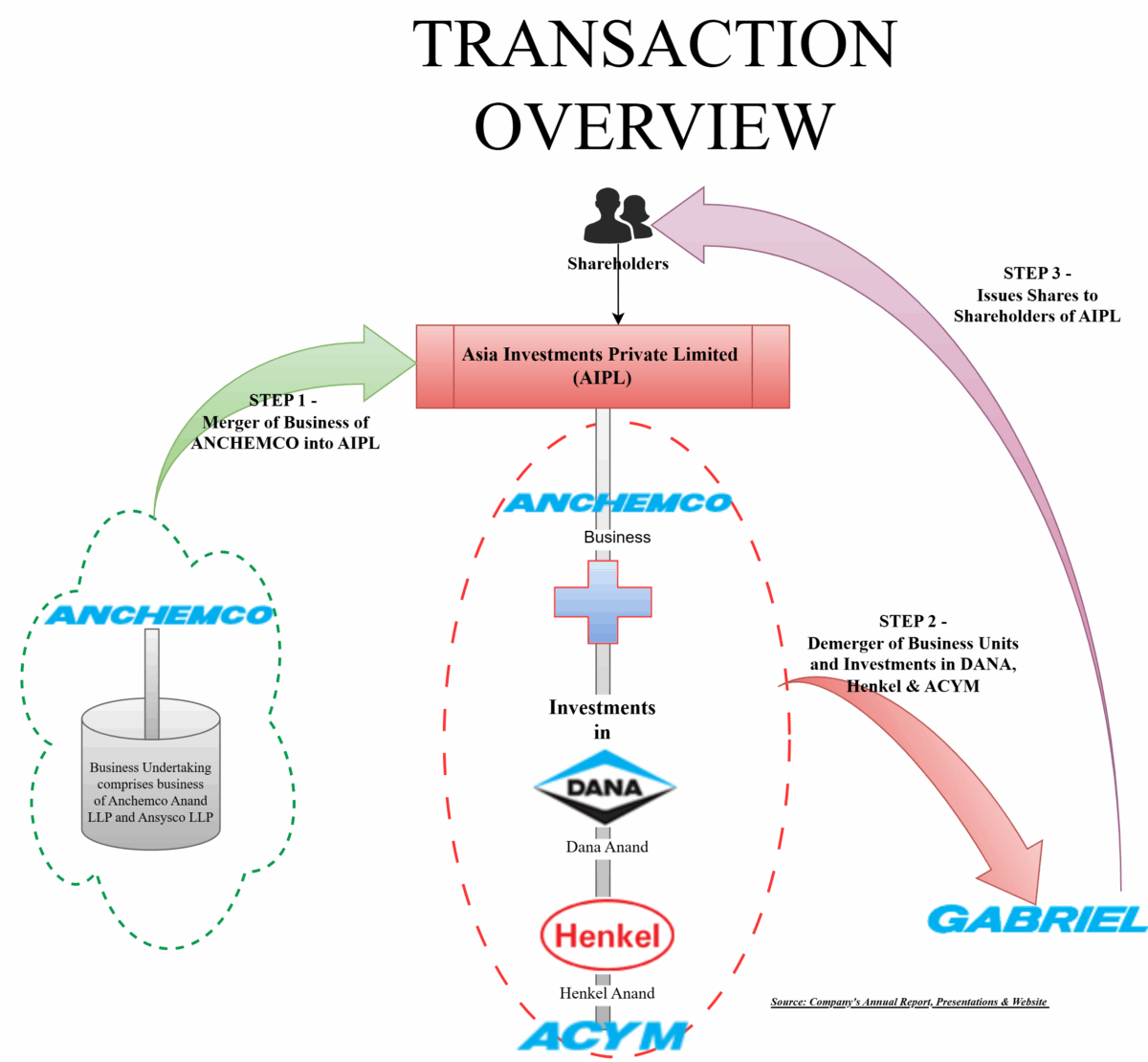

The Board of Directors of Gabriel has approved a Composite Scheme of Arrangement (“Scheme”) proposed to be filed under Sections 230-232 of the Companies Act, 2013 for

Step 1: Amalgamation of Anchemco India Private Limited with and into Asia Investments Private Limited and,

Step 2: Demerger of the Automotive Undertaking of Asia Investments Private Limited into Gabriel India Limited.

Demerged Undertaking” or “Automotive Undertaking” means the entire business undertaking comprising of business of Anchemco (engaged in manufacturing of brake fluids, radiator coolants, diesel exhaust fluid (DEF) / ad-blue, and PU/ PVC based adhesives) and investments in Dana Anand India Private Limited, Henkel ANAND India Private Limited and ANAND CY Myutec Automotive Private Limited into Gabriel.

The above transaction shall have two appointed dates: 1st April 2025 for the merger of Anchemco into AIPL and 1st April 2026 for the demerger.

The choice of prospective effective date for the demerger—i.e., a full year after the merger—warrants consideration.

In our view, one of the key reasons appears to be AIPL’s current lack of business activity. Post-merger, however, AIPL will acquire Anchemco’s business, thereby housing business undertaking.

A prospective demerger date ensures that AIPL has a full financial year of business operations, which:

- Establishes a clear operational and accounting track record,

- Facilitates identification of the “Undertaking” to be demerged under the Income Tax Act,

- Strengthens the substance of the demerger, especially since the undertaking will also include significant investments in three joint ventures.

Thus, the structure ensures that the demerged assets—including the JV investments—are first consolidated under AIPL, then hived off as a defined undertaking after demonstrating one year of integrated operations.

Further, transaction has been thoughtfully structured to capture multiple facets. Anchemco is being first made ready to have a good amount of business operations. It will first get merged with the holding company, AIPL which then demerge the business along with investment in different JV’s into Gabriel which essentially usher in parking JV’s under Gabriel in tax efficient way and without any involvement of JV partners/JV entities.

Noteworthy element is that as part of the demerger, AIPL will not transfer its holding in Gabriel which would have resulted in direct shareholding of Gabriel in the hands of promoter shareholders.

This Scheme will consolidate the business of the Demerged Undertaking of AIPL in automotive components and products like drive train products including transmissions for EVs, Body in White and NVH Products and solutions, brass and steel synchroniser rings, aluminum forgings, brake fluids, radiator coolants and diesel exhaust fluids (DEF) / Ad-Blue for 2W, 3W and 4W vehicles and trucks and PU and PVC based adhesives into Gabriel. This inclusion, together with the recently added sunroof business, will transform Gabriel from a mono-product suspension company into a diversified, technology-driven mobility solutions provider, and reducing the dependency on a single product line by expansion into new segments, geographies, the aftermarket product range, and railways product range.

Rationale for the proposed transaction:

The Scheme is designed to strategically reposition Gabriel as a diversified mobility solutions provider by rationalising the corporate structure and, in the process, enhance stakeholder value. The scheme, inter-alia, expected to yield the following benefits:

- Consolidate the business of the Demerged Undertaking of the Demerged Company in automotive components and products like drive train products including transmissions for EVs, Body in White and NVH Products and solutions, brass and steel synchroniser rings, aluminium forgings, brake fluids, radiator coolants and diesel exhaust fluids (DEF) / Ad-Blue for 2W, 3W and 4W vehicles and trucks and PU and PVC based adhesives in the Resulting Company, thereby transforming the Resulting Company from a mono-product suspension company into a diversified, technology-driven mobility solutions provider, and reducing the dependency on a single product line by expansion into new segments, geographies, the aftermarket product range and railways product range;

- Optimize the Resulting Company’s supply chain, enhance marketing strategies and strengthen customer relationships, establishing a robust foundation for growth;

- Enables the Resulting Company to position as a preferred global OEM partner, delivering platform flexibility and ensuring alignment with future industry needs;

- Enhancing the Resulting Company to project as a preferred partner for future foreign collaborations in the automotive components space, and enhancing its presence in foreign markets, specifically the US and European markets, ensuring its potential to attract capital for future growth and fostering the development of new technologies.

Consideration for the merger & demerger

The entire share capital of Anchemco India is directly and indirectly owned by Asia Investment. Thus, upon merger of Anchemco India with Asia Investment, no consideration will be issued. Upon demerger, Gabriel will issue shares to the shareholders of Asian Investment (Promoters) and as a result, cumulative promoter holding will get increased. Gabriel will issue 1158 fully paid equity shares of Re. 1 each, for every 1000 equity shares of Rs. 10 each held in Asia Investment.

Financials & Valuation

Broad valuations assigned to private businesses are as follows:

| Particulars | Amount |

| No. of Equity shares issued for demerger | 3,35,86,081 |

| Price Per share- Gabriel (as on 30th June 2025) | 695 |

| Value of shares issued in crore | 2334 |

| Combined EBITDA (On proportionate basis) | 276 |

| Combined net debt (On proportionate basis) | 36 |

| EV/EBITDA assigned | 8.60 |

| Gabriel EV/EBITDA | 29 |

One must consider major businesses are in three JVs which will be subsidiaries of Gabriel post transaction hence have holding company discount.

Conclusion

The proposed restructuring by the Anand Group is a strategically calibrated move aimed at consolidating its automotive component businesses under the publicly listed entity, Gabriel India Limited. The transaction structure has been well thought to capture commercial and regulatory aspects and because of consolidation of all private companies in the group in the listed company it will make transparent structure for investors and institutions alike.

This transformation will reposition Gabriel from a mono-product suspension manufacturer into a diversified, technology-led mobility solutions provider with enhanced capabilities across drivetrain systems, adhesives, cooling fluids, and structural components. The inclusion of high-margin joint ventures and recent additions like the sunroof business will not only expand Gabriel’s product offerings but also significantly strengthen its positioning with global OEMs, especially in the EV and export-oriented supply chains.

No doubt results into additional stake for the promoters in the listed company and enables Gabriel to raise substantial funds for organic and inorganic growth maintaining control with promoters. With improved operational leverage and sharper strategic focus, the transaction may help unlock long-term value for all stakeholders. Let’s see how synergies play out in future.