The Indian chemical industry is at an inflection phase. Falling global crude prices, tough competition and weaker fundamentals will drive mergers and acquisition activities in the industry. While commodity chemicals will likely comprise most of the M&A activities, significant volumes are expected in specialty and agricultural chemicals segments.

In order to be profitable in business and grow, chemical companies are exploring inorganic growth through acquisitions. Limited growth opportunities in the organic route and hassels in various environment approvals will ensure companies look for growth avenues through acquisitions. Small Indian companies will seek partnerships for scaling up or look for exit routes through sell-offs. Consolidation of companies and products will help companies to leverage its potential synergies and look at new business opportunities in a fast-changing environment of consumer demand. Moreover, stressed balance sheet of some companies will force them to look for buyers to sell and pare debt.

Globally, chemical companies are known looking for early cyclical – firms that see the first signs of a pick-up in demand because of an economic upturn. Well prepared firms who can take the acquisition route to grow will stay ahead of the curve at the time of economic recovery. The purchase of product lines at a reasonable valuation will complement companies’ existing offerings and allow them to move to lucrative areas for growth.

To put some perspective, according to Mergermarket Intelligence, a global M&A tracking firm, the Indian chemicals industry is likely to see rising M&A deals in 2017 because of the slowdown in Chinese manufacturing sector and growing appetite of multinationals to expand their presence in India. It underlines that the main areas of interest are specialty chemicals, aroma chemicals, agrochemicals, flavour and fragrances, and niche chemicals.

Chemical industry’s matrix

India is the third largest producer of chemicals in Asia and the eighth largest in the world. An analysis by Deloitte shows that the industry could grow at 11% per annum to reach the size of $224 billion by 2017. The industry is largely connected to key economic sectors such as agriculture, agro-commodities, services and manufacturing. The Indian chemicals industry has a diversified manufacturing base that produces world-class products. There is a substantial presence of downstream industries in all segments. India has a strong presence in the exports market too in the sub-segments of dyes, pharmaceuticals and agro-chemicals. India is the world’s third largest consumer of polymers and third largest producer of agrochemicals.

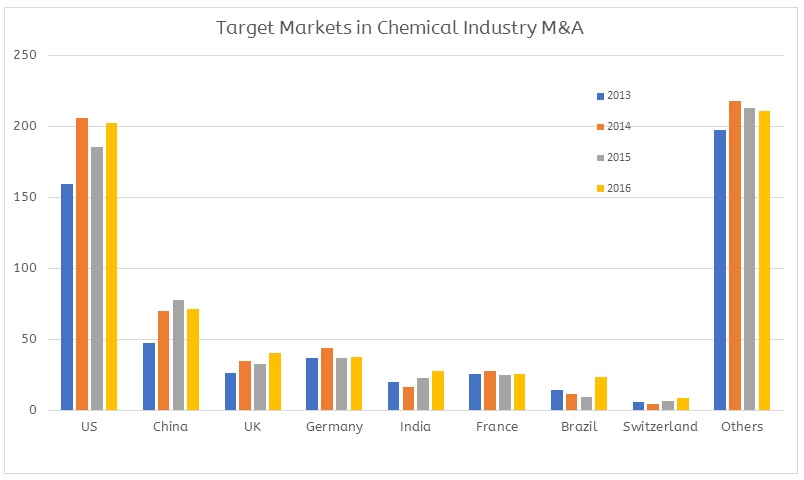

Figure 1: Target Countries (Source: Deloitte)

For instance, in 2010, American chemicals major Huntsman Corporation took over Gujarat-based chemicals producer Laffans Petrochemicals and the ownership of the company’s 60-kilo tonne ethylene oxide derivatives facility at Ankleshwar. Huntsman brought money, technology, and expertise to meet the growing needs of the Indian market, which was necessary to take the business to the next level. The Texas-based Huntsman is a global manufacturer and marketer of differentiated chemicals to industries such as chemicals, plastics, automotive, aviation among others. Huntsman India has its facilities at Navi Mumbai and had technical collaboration with Laffans since 2009. Laffans was set up in 1994 to manufacture ethylene oxide derivatives and in 2010 the company had earned $53 million in revenues. The company’s Ankleshwar plant was set up under technical assistance from Reliance Industries and is in proximity to the Hazira plant of Reliance. Post-deal, the chemicals business of Laffans became an integral part of Huntsman Performance Products, giving the division its first dedicated production plant in the country.

Past deals

European specialty chemical major Lanxess acquired the chemical and wind power assets of Mumbai-based specialty chemical manufacturer Gwalior Chemical Industries Ltd (GCIL) for an aggregate value of 82.4 million euros (Rs 536 crore) in 2009. Gwalior Chemicals made benzyl products and was one of the leading global producers of sulphur chlorides for the agrochemicals, pharmaceutical as well as flavor and fragrance industries. The deal marked the first Indian acquisition by Lanxess and was in line with its long-term strategy of expanding in India, which is the second most important Asian market for the company after China. Before acquiring GCIL, the company took over the business and production assets of China-based Jiangsu Polyols Chemical and later continued to purchase Chinese companies available at attractive valuations.

In June 2015, German specialty chemicals maker Evonik Industries acquired Monarch Catalyst, a family-owned enterprise founded in 1973 by Dr. K. Muthukumar and Shantibhai Vadalia with its production site in Dombivli, near Mumbai. Evonik has a presence in almost 100 countries around the world. It serves life sciences and fine chemicals, industrial and petrochemical market segments. In fact, the Monarch deal highlighted the continuing attractiveness of Indian chemical sector for strategic foreign investors. In November 2014, Japan-based Nihon Nohyaku Co. Ltd acquired 74% stake in Hyderabad Chemical Ltd for an undisclosed amount. Hyderabad Chemical is an agrochemical manufacturer with its own distribution network and research and development function.

Last year, Purnendu Chatterjee-led The Chatterjee Group (TCG) has picked up a majority stake in Mitsubishi Chemical Corporation’s (MCC) Indian unit in Haldia in West Bengal for an estimated $48 million (Rs 322.27 crore) which has given TCG management control of the sick company. According to the share purchase agreement, of the 6.4 billion shares of MCPI (MCC PTA India Corporation) – the Haldia-based Indian entity of MCC, TCG bought 5.8 billion shares or 90 per cent stake in the company with MCC retaining 600 million shares. MCC PTA has been making losses for several years as revenue declined owing to cheaper imports from China. The Competition Commission of India cleared the acquisition.

Even joint ventures between Indian and foreign companies in the chemical industry have picked up pace. In February this year, American automotive chemicals manufacturer Penray Inc and India’s automotive specialist Talbros Gardx Performance Products have announced a partnership that will see Penray’s chemical additives, functional fluids and car care products marketed throughout India using the Talbros sales, marketing and distribution expertise. Penray has a 65-year history of developing, manufacturing and marketing products targeted at professional mechanics and workshops that service light, medium and heavy-duty vehicles. In addition, many Penray products are suitable for use in servicing motorcycles and motorbikes. The partnership with Penray will provide Talbros with a line of chemical products needed to service the millions of petrol- and diesel-powered cars, trucks and motorcycles in India. Included in the line will be car care products, cleaners, functional fluids, professional installer kits and service chemicals.

Similarly, last year Dutch specialty chemicals major AkzoNobel and Atul Ltd, a Lalbhai Group company, have signed an agreement to set up a manufacturing joint venture for the production of monochloro acetic acid (MCA) in India. The two companies plan to install a MCA plant at Atul’s facility in Gujarat, building on Atul’s status as a leading supplier of crop protection chemicals (which uses MCA as a key raw material) and AkzoNobel’s leading global position in MCA, with plants in the Netherlands, China, Japan and the US. The JV will use chlorine and hydrogen manufactured by Atul to produce MCA, taking advantage of Atul’s existing infrastructure and AkzoNobel’s latest eco-friendly hydrogenation technology.

In the same trend, Pidilite Industries Ltd, a maker of adhesives, sealants, construction chemicals, consumer adhesives and specialty chemicals, entered into a joint venture agreement last year with Industria Chimica Adriatica Spa (ICA), a leading wood finish manufacturer based in Italy. Pidilite will have 50% of the shareholding in the JV and the balance will be held by ICA and India-based distributor Pratik Mehta. Such joint ventures with foreign companies will help Indian companies to scale their business operations and tap new markets with specialized products.

Global perspective

Worldwide, companies have been doing acquisitions to stay competitive. Transactions such as Bayer Corporation’s $66 billion deal for Monsanto, China National Chemical Corporation’s $43 billion acquisition of Syngenta AG and Potash Corporation’s $22 billion merger with Agrium were among last year’s big global M&A deals. Mega deals have become the norm with 41 deals valued over $1 billion over the past three years, as compared to $30 deals between 2011 and 2013. Though valuations have soared, many companies continue to pursue M&A as a strategy to achieve growth and spur innovation.