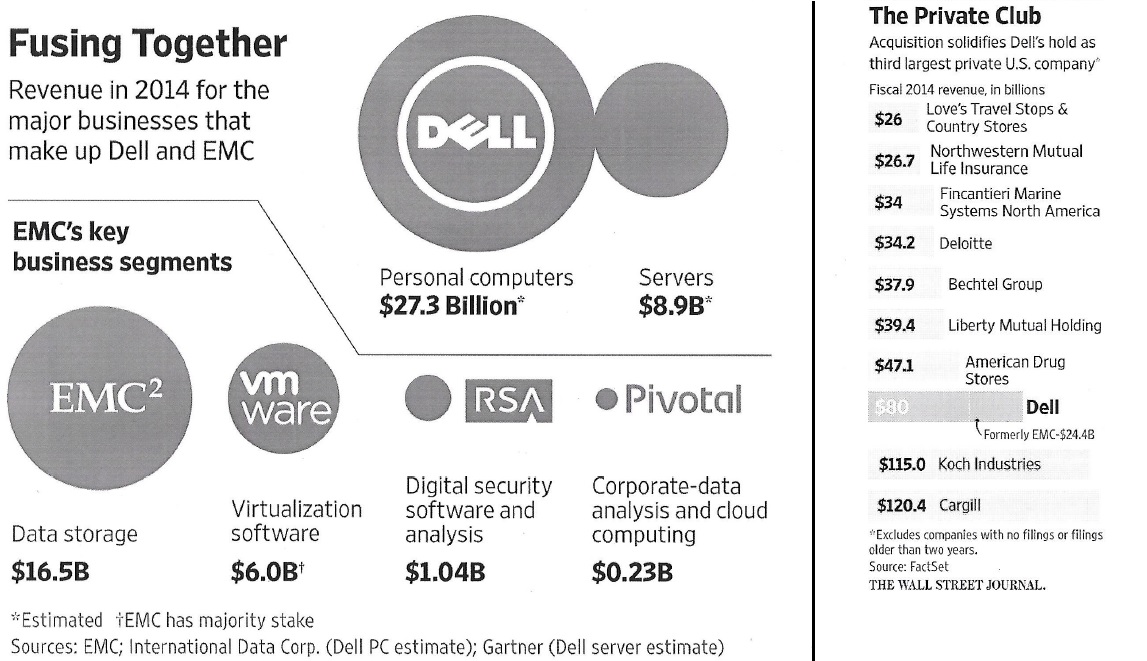

In a biggest-ever technology acquisition, PC maker Dell and private-equity player Silver Lake Partners have acquired data storage provider EMC for $67 billion in a cash-and-shares deal. The $33.15 per share deal works out as 28% premium above EMC’s closing price on October 7 when the media reports first cropped up of the probable transaction. Or even more relevant, a 35% premium to shares of EMC trading at an average of $24.64 per share over the past 30 days before the announcement of the deal. The merger agreement includes a 60-day ‘go-shop’ provision that allows EMC to solicit bids from other parties and pay a discounted breakup fee to Dell if a deal is made with another company. Privately-held Dell is raising about $40 billion in debt financing to make this deal happen. The transaction is expected to close between May and October 2016 and the combined conglomerate will focus on paying down the debt in two years after the closing of the deal.

For Michael Dell, chairman and chief executive officer of Dell, the deal can position him as an enterprise player purely focused on data storage in the changing technology landscape. With this deal, Dell gets a controlling stake in VMware, a $34-billion cloud-computing software vendor, which was 85% owned by EMC. As Dell is not competitive on storage, EMC will help it to build a full portfolio to compete with Hewlett-Packard, Cisco, and IBM. “The combination of Dell and EMC will create the industry leader” in the $2 trillion information technology markets where they have complementary portfolio technologies and other resources, Dell said during the conference call. “The transaction also strengthens both companies in the increasingly competitive global marketplace,” he underlined.

Post-merger operations

The firm will have three technology centers – in Austin, Texas, near where Dell is based in Silicon Valley and in Massachusetts, EMC’s base. The company officials have said that there are no immediate plans for layoff related to the transactions. Michael Dell will head the company as chairman and chief executive officer. The acquisition will make Dell the number three player in enterprise technology by revenue, trailing Hewlett-Packard and IBM. The deal will enable Dell to incubate new enterprise products, including cloud-based technology offerings. “An acquisition of the EMC storage business would immediately make Dell the market share leader in storage and help the company diversify away from the PC market,” Robert W Baird & Co analyst Jayson Noland said in a research report. Similarly, Forrester Research analyst Glenn O’Donnell says the combined company represents a serious competitive threat to Hewlett-Packard.

Marius Hass, chief commercial officer and president of Enterprise Solutions of Dell in an interview to CRN had underlined that the company will do extreme diligence to make sure there is zero customer disruption and there is zero partner disruption. However, what remains to be seen now is that how the two massive companies with entrenched cultures come together into a single entity.

Done Deal for EMC

However, off late EMC was facing headwinds as the IT industry moved more functions to the cloud. Instead of building and maintaining data centers, companies are offloading lots of functions to data centers run by Amazon, Microsoft, and Google. Tech analysts have been downgrading EMC stocks since January this year because of lower guidance and the company resorted to cost-saving methods, including mass layoffs and corporate reorganization. Even VMware has been slow with its entry into the cloud market and seeing its business threatened by a flood of cheaper alternatives

Terms and valuation of the deal are value creation opportunity for EMC shareholders and may be with synergy with Dell business, it may be able to improve both top line and contribution on services and products supplied by it .

Will Dell gain?

Back in the nineties, Dell focused on manufacturing custom built-to-order personal computers through its website and retained its position as the number one PC manufacturer for 10 years. But with the advent of tablets, mobile phones, Dell lost the edge in the PC market. Moreover, even in the PC market, competitors like HP had caught up with Dell’s manufacturing process and the company could no longer claim the price advantage. By 2011, Dell slipped to number three slot in the PC market behind HP and Lenovo. The company delisted itself from the public markets in 2013 to ward off quarter-to-quarter pressure for steady earnings and other trappings of managing a public company. So, diversification remained the only answer for Dell to stay in the business. In fact, both Dell and EMC has no option but to come together even to survive in its core business

Dell has about $12 billion in debt and would need to raise $40 billion more to do the deal, which some are questioning whether it would be able to do. How fast combined entity will be able to deleverage itself will be key to the success of the transaction. It is certainly possible that the combined Dell-EMC entity could sell assets to generate additional cash in the future, including anything from a partial sale of VMware, which is easiest to do as it is listed.

Will the deal reshape the tech market?

First of all the acquisition is not as unique as Oracle’s purchase of Sun Microsystems or Hewlett-Packard’s buyout of Digital Equipment Corporation with competitive platforms. Dell is already a major reseller of EMC products and the latter generated 8% to 9% of its revenue from its relationship with Dell. And for Dell, the partnership accounted for 50% of its storage revenue.

Dell’s corporate rival Hewlett-Packard issued a statement rejecting the probability that the Dell-EMC combination will cause its business to suffer. “This is a real opportunity for HP. Two of our largest competitors are attempting a highly distracting, multi-year merger, just as we are launching two new, focused companies. The massive debt burden Dell and EMC are taking on undoubtedly means that they will have to radically reduce R&D, and integration inevitably will create disruption as they rationalize product portfolios, channel programs, and leadership. While Dell and EMC are sorting out their future, Hewlett-Packard Enterprise and HP Inc. will be working to take share and advance our technology leadership in key areas like converged infrastructure, private cloud, all-flash storage, personal systems and printing,” it said.

Similarly, networking giant Cisco said the acquisition wasn’t surprising considering the recent wave of acquisitions in the enterprise tech space. “The announcement by Dell and EMC is no surprise. We’ve been calling out industry consolidation for years and have seen this ‘merger of equals’ movie many times. There is no lack of opportunities for Cisco, and we are focused on growth opportunities that position us for where the market is going. EMC continues to be a Cisco partner, and we are seeing great momentum as we deliver value together for our customers, specifically through VCE,” it said.

Questions have been raised as to why the two aging technology companies would seek to bind themselves to endure the winds of technological change. For sure, the deal does not address the existential plight of the two companies at a time when the core business of both the companies is under attack and facing steady decline. The deal is just another sign of panic among old guard information technology players trying to make sense of new world IT business. The strategy of Dell is exactly opposite of Hewlett-Packard. Both strategies may work or may not work. It is in the interest of the customers of both the companies that both are successful so that they can get more efficient technology and products. Irrespective of how it plans out, it is win-win for EMC shareholders and they should exit and book their profits.

{kind=link}

{kind=link}