Incorporated in 2007, the Company is a leading integrated power infrastructure services companies in India providing comprehensive erection, testing and commissioning of boilers, turbines and generators (“ETC-BTG”) and balance of plant (“BOP”) works, civil works and operation and maintenance (O&M) services. Power Mech Projects Limited was founded by Kishore Babu in 1999. Company’s operations include three principal business lines:

- Erection Works;

- Operation & Maintenance (O&M) Services; and

- Civil Works.

The company has an established track record of successfully executing ETC-BTG and BOP contracts for large power projects including for 800 MW unit capacity super-critical projects. They have been engaged on ETC-BTG projects for the first two ultra-mega power projects (UMPPs) in India as well as for 16 super-critical power projects in India. They were also one of the first companies in India to carry out the overhauling of a super-critical 660 MW turbine and providing AMC services for an ultra-mega power project (UMPP).

Clientele

They have worked on various projects for Bharat Heavy Electricals Ltd, NTPC Ltd, Doosan Power Systems India Private Ltd, Adani Power Ltd, Larsen & Toubro Ltd-Thermal Power Plant Construction BU, Thermal Powertech Corporation India Ltd, GE Power Services (India) Private Ltd, CLP India Private Ltd, BGR Energy Systems Ltd, Siemens Ltd, Jindal India Thermal Power Ltd and Reliance Infrastructure Ltd.

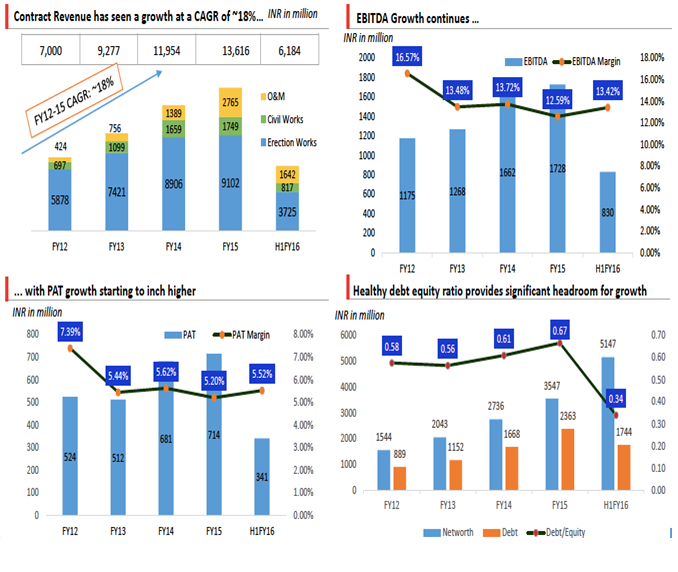

Financials

Power Mech Projects had reported a net profit of Rs 71 crore on sales of Rs 1,356 crore in the financial year ending March 31, 2015. Over FY2013-15, Power Mech projects had registered a CAGR growth of 20.5 per cent in its revenue, while its net profit grew at a CAGR of 9.8 percent.

“In the course of preparing for IPO, Power Mech created a win-win situation by raising capital without dilution, reduce its debt and restructured their shareholding to get into a position for expansion of its core business with ease in the near future”

The IPO

In 2014, Power Mech decided to come up with an IPO. The company offered 4,269,000 equity shares to the public through two routes :

| Particulars | No. of

equity shares |

| Fresh Issue | 21,28,000 |

| Offer for sale | 21,34,500 |

Fresh Issue

The objective of the fresh issue of the share was:

- Repayment / pre-payment/ advance payment, in full or part, of certain borrowings availed by the company and repayment of buyer’s credit and retirement of foreign letter of credit;

- Funding working capital requirements of the company; and

- General Corporate Purposes

The IPO proceeds are to be used for funding working capital requirements of the company

(INR 120 crore) and for general corporate purposes (INR 24.5 crore).

Offer for sale

- Indian Business Equity Fund backed by MotilalOswal PE group had invested INR 40 crore in the company in tranches starting in 2009 and in the pre-IPO stage held 19.89% stake, which posts the offer for sale, would be 2.24%.

The Power Mech initial public offering (IPO) was raised up to INR 273.2 crore and was subscribed 38 times.

The institutional investor category was subscribed 27 times, high net worth individual segment saw a whopping 133 times subscription. The category meant for retail investors was subscribed around three times.

Ahead of its IPO, the company had raised INR 82 crore from anchor investors, which included DSP BlackRock, SBI Mutual Fund, and IDFC Mutual Fund. Power Mech had fixed a price band of Rs 615 and Rs 640 per equity share for its IPO.

PRE- IPO

Capital Restructuring History

- July 23,1999

The company started with 1000 equity shares of face value of INR 10 @ INR 10 each of issue price.

- November 27, 2009

As on November on 2009, Preferential allotment of 2,500,000 compulsorily convertible preference shares to India Business Excellence Fund; and 7,500,000 compulsorily convertible preference shares to India Business Excellence Fund I backed by Motilal Oswal group was done.

Over a period of time, the company issued equity shares and through preferential allotment raised cumulative equity shares to 90,00,100 of the face value of INR 10 @ INR 10 each of issue price.

| Date | Particulars | Issue Price | Number of shares | Cumulative number of shares |

| January 18, 2011 | Conversion of compulsorily convertible preference shares into equity shares held by:

IBEF – 2,500,000 prefrence shares converted to 438,166 equity shares &IBEF-I – 7,500,000 prefrence shares converted to 1,314,498 equity shares |

142.64 | 17,52,664 | 1,07,52,764 |

| November 26, 2013 | Conversion of compulsorily convertible debenture into equity shares held by: IBEF I – 1125 debentures converted to 562,500 equity shares | 200 | 1,87,500 | 1,09,40,264 |

| June 26. 2014 | Bonus issue equity shares in the ratio of 10:1.2. IBEF & IBEF-I were not allotted any bonus shares | – | 10,80,000 | 1,20,20,264 |

| July 16, 2014 | Conversion of compulsorily convertible debentures into equity shares held : IBEF-I – 1125 debentures converted to 562,500 equity shares | 200 | 5,62,500 | 1,25,82,764 |

Shareholding Pattern (Pre-IPO & Post-IPO)

Details of Promoters contribution and lock in

| Paritculars | No of Equity Shares | % of Pre-issue capital | % of Post issue Capital |

| Promoter/Promoter Group | 95,25,068 | 75.7 | 64.75 |

Pursuant to Regulations, an aggregate of 20.00% of the fully diluted post-Issue capital of our Company held by the Promoters shall be locked in for a period of three years from the date of Allotment.

Selling Shareholders of the company

| Pre-Issue | Post Issue | |||

| Name | No of equity shares | % of Pre-issue capital | No of equity shares | % of Post-issue capital |

| Indian Business Excellence Fund I | 1877073 | 14.92% | 187773 | 1.28% |

| Indian Business Excellence Fund | 625691 | 4.97% | 186991 | 1.27% |

| TOTAL | 2502764 | 19.89% | 374764 | 2.55% |

The Company had 570 Shareholders as of the date of this Draft Red Herring Prospectus. India business excellence fund exited most of its investments at a handsome profit in about 5 years.

Steps towards IPO

- In 2009, the company raised capital of INR 40 crores in the form of equity and compulsorily convertible preference shares from PE investors.

- Improved net worth enabled the company to raised long-term loans.

- The capital + debt raised enabled the company to scale up its business about three times in terms of the top line in five years (INR 1379 crores in FY15 from INR 494 crores) and improved parameters in all other aspects.

- In 2014, the company entered into an MOU with Chengdu Pengrungrun New Energy Development Co. Limited, Hong Kong In order to establish a joint venture entity in Hong Kong for the distribution of equipment and spare parts, including boilers, turbines, and generators, for O&M projects in India.

- In addition, the company is in the process of setting up a large heavy engineering fabrication facility at Noida for non-critical equipment and spare parts. The company has also entered into a Cooperation Agreement with Shanghai Electric Power Generation Service Co. with respect to repair and overhauling contracts in the power sector in India.

FINANCIAL PERFORMANCE OF POWERMECH PROJECTS LIMITED ( POST – IPO)

In its pre-IPO stage, Power Mech has achieved a 38% market share while in the highly profitable O&M business it holds a 60% market share in private IPPs; backed with a huge order book. It created core capabilities to provide end-to-end solution in the power sector

The company has achieved a scalability in its niche business through its great management handled by a first generation entrepreneur, capital restructuring , business restructuring through JV route and strategic changes for expansion in domestic and also now in international markets.

The company in the Pre-IPO stage did not go through any structural change through any merger/acquisition or amalgamation for raising the capital and thus not diluting its equity capital.

The only capital raised by the company was the through entry of the Indian Business Excellence Fund by issuing compulsory convertible preference shares and compulsory convertible debentures which would then be converted into equity shares.

At the time of the IPO, the management’s calculative move resulted in the exit of a PE investor by bringing down its equity stake from 19.89% to a mere 2.55% in the company through an offer for sale route at an exorbitant price.

Thus these steps taken in the course of preparing itself for the IPO created a win-win situation for the company and the investor as the company was able to raise the capital by not issuing additional equity shares and also not paying any money to the PE investor for exiting the firm.

Post-IPO: the company has outlined future strategic moves that it would take for the expansion of its operations while focusing on its higher margin business by leveraging technical expertise in achieving the same.

{kind=link}