Hindware Group has once again announced a major corporate restructuring—yet another chapter in its long history of reorganisations aimed at unlocking shareholder value. Over the past decade, the group has undergone multiple cycles of demergers, consolidations, and realignments. However, these changes have yet to yield meaningful or sustained value creation. With the latest scheme of arrangement, the key question remains: Will this time be different?

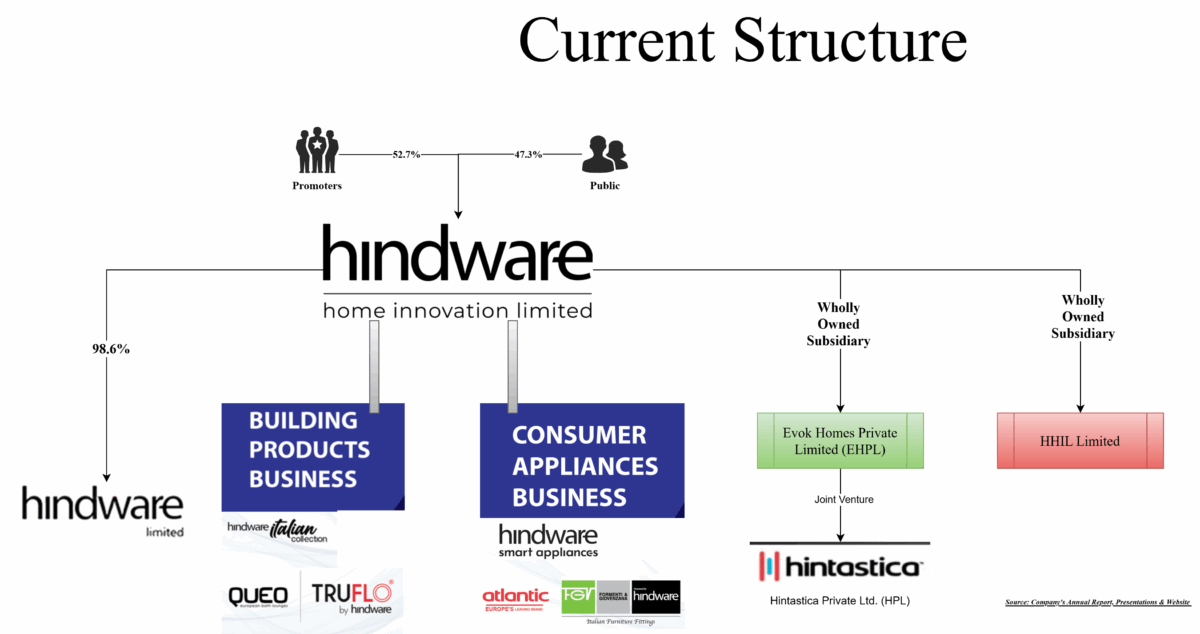

Hindware Home Innovation Limited (“HHIL” or “Demerged Company” or “Transferor Company”) is a listed company having two distinct segments:

(i) Consumer Products Business, which inter-alia comprises of kitchen appliances, consumer appliances, fixtures and fittings, offline retail, water heaters, carried through a joint venture company, Hintastica Private Limited, and online retail undertaken through its wholly owned subsidiary i.e., Evok Homes Private Limited; and

(ii) Building Products Business, which inter-alia comprises of sanitaryware, faucets, tiles, other bath fittings, pipes, fittings and related building products. The Building Products Business is being carried out through its subsidiary, i.e., Hindware Limited.

In the last 5-7 years, HHIL has undergone several group restructurings including:

- 2020: Starting of HHIL pursuant to the demerger of marketing/distribution businesses from HSIL into HHIL and Brilloca Ltd. (now Hindware Ltd.)

- 2022: Acquisition through slump sale of AGI Greenpac Limited’s manufacturing operations to strengthen Building Products.

- Name change from Somany Home Innovation Limited and Brilloca Ltd to HHIL and Hindware Limited, respectively.

- Joint venture creation for water heaters.

- 2025: Fundraising via an INR 250 crore rights issue to absorb losses.

- EVOK- the retail business was shut down due to unsustainable losses.

Despite the consistent efforts, the HHIL failed to turn around its consumer product business and in pursuit of new initiatives, forgot to grow its core business.

Hindware Limited (“Transferee Company”), along with its subsidiaries, is, inter alia, engaged in the Building Products Business which primarily comprises of sanitaryware, faucets, tiles, other bath fittings, pipes, fittings and related building products. The demerged company owns 98.6% of the transferee company while the remaining capital is owned by certain employees of the company.

HHIL Limited (“Resulting Company”) is a wholly owned subsidiary of the demerged company which is incorporated to facilitate the demerger of Consumer Product business.

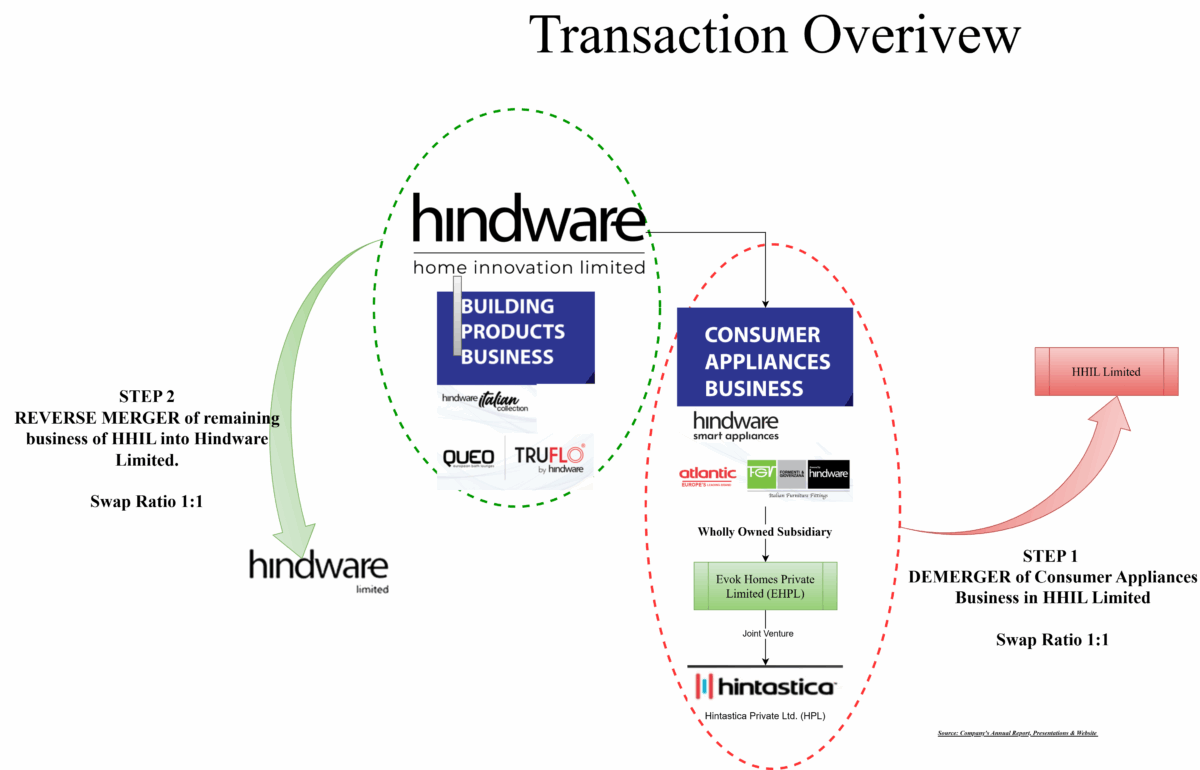

The Transaction

The Board of Directors of Hindware Home Innovation Limited has approved a Composite Scheme of Arrangement between itself, HHIL Limited and Hindware Limited and their respective shareholders and creditors (“Scheme”) under Sections 230 to 232 of the Companies Act, 2013,

The Scheme inter-alia envisages:

- Demerger of the “Consumer Product Business” from the Demerged Company into the Resulting Company on a going concern basis and

- Amalgamation of the remaining HHIL (post demerger, primarily holding investment in Hindware Ltd.) into Hindware Ltd., in a reverse merger.

The turnover of the Demerged Undertaking is 100% to the total turnover of HHIL in the financial year ending 31st March 2024. The appointed date for both demerger & merger shall be 1st April 2025.

Essentially, the entire business of standalone HHIL shall get demerged and the remaining HHIL will be left with only investment in the transferee company. The remaining HHIL will get merged (reverse merger) with Hindware Limited.

Reverse merger makes sense as merging operating company may have compliance challenges (change of registrations, vendor code, contracts, etc.); however, from the record date till listing of the equity shares of Hindware Limited, the public shareholders will face liquidity vacuum as shares won’t be available for trading. Further, the complex structure may create initial pricing anomaly.

Rationale for the transaction

As per the management, the past year has been a period of profound strategic introspection for the business, during which they have vigorously identified critical areas to not only recapture market share, but also to significantly bolster overall profitability. As a result, one of the options which they decided on is to split the businesses.

Both the undertakings of the demerged company have different:

- distribution channels, influencers, competition, challenges and opportunities for its business and products;

- capital requirements, working capital and associated risk and returns in carrying on their respective business;

- skills required for manufacturing, technology, installation and customer service and manpower requirements; and

- strategic and financial investors’ interest.

Thereafter merger of HHIL with Hindware Limited is to streamline the ownership structure for Hindware Limited. The merger is evitable as post demerger, HHIL will be purely holding company and may attract NBFC compliances and importantly will likely to have holding company discount.

Swap Ratio

For demerger of consumer product business

1 (One) fully paid-up equity share having a face value of INR 2 (Two) each of the Resulting Company, credited as fully paid up, for every 1 (One) fully paid-up equity share having a face value of INR 2 (Two) each of the Demerged Company.

Effectively, post demerger, the shareholding pattern of the resulting company shall be a mirror-image holding of that of the demerged company.

Swap ratio for merger

1 fully paid-up equity share of INR 2 each of the Transferee Company, credited as fully paid up, for every 1 fully paid-up equity share of INR 2 each of the Remaining Transferor Company.

As post-demerger, HHIL shall consist of only investment in Hindware Limited. After calculating the swap ratio, transferee company was not able to meet the minimum paid-up capital requirement of INR 10 crore as mandated for any listed company for IPO.

In order to ensure SEBI compliance and since remaining HHIL is the only holding company, the management of HHIL decided to maintain the shareholding pattern of HHIL in Hindware Limited. Thus 1:1 swap ratio has been proposed.

To safeguard the employee stake in Hindware Limited (circa 1.4% which is held through partly paid-up shares), Hindware Limited will issue additional partly paid-up shares to employees to compensate for any dilution. One needs to ponder any additional tax burden of employees pursuant to this?

To avoid tax, Hindware Limited will re-organised its partly paid-up shares for 900,000 partly paid shares (face value INR 2 at a premium of INR 450 with INR 1 paid up) to 15,25,424 partly paid-up shares (face value INR 2 at a premium of INR 264.68 with INR 0.59 paid up).

| Particular | No. of partly paid up shares (a) | Issue price of INR 2 per partly paid up shares (b) | Total Value in Crore (c) = (a*b) | Paid-up value per share (d) | Total paid up value (d/2) * (c) |

| Earlier | 900,000 | 452 | 40.68 | 1 | 20.34 |

| Revised | 15,25,242 | 266.68 | 40.68 | 0.59 | 12.00 |

Financials & Valuation

Interestingly, the revenues of the consumer product division & building division are down in 2025 compared to 2024. The consumer product division continues to incur operating losses. Further, segment assets & liabilities for Consumer Product business has also shrinked in FY 2025 compared to FY 2024.

Consumer product business is way smaller than the core building business. Building business is also expanding and trying to regain the market share it lost over a decade to its competitors.

The assigned valuation of remaining HHIL (investment in Hindware Limited) as per valuation report is circa INR 1408 crore. The market capitalisation as on 26th March 2025 (being valuation date) of HHIL was circa INR 1600 crore. This suggests that most of the current value lies within the Building Products business. It will be interesting to see how a standalone consumer product business listed entity will fetch valuation and be able to sustain its operating losses. Probably, the management may consider the option of inviting a strategic or financial partner for the consumer product business.

Clearly, the division is yet to pick up and facing challenges from competition. Margin pressure is building up and post standalone listed entity, it will be challenging to survive unless some strategic steps are taken.

Conclusion: More Form Than Substance?

Looking at past restructurings and growth in market cap, one really need to ponder whether over diversification has ushered in lack of focus and delivered no value to shareholders? The success of new restructuring hinges on execution, not just rearranging business.

Unless backed by meaningful operational improvements or strategic investments, the restructuring may end up as another cosmetic reshuffle with no real value for any stakeholders.