JSW is aggressively betting on the expansion of its power generation business. Power Generation business has a huge gestation gap in terms of time from setting up the business to make it profitable. Therefore to make it short, instead of Greenfield expansion which requires a long gestation period, JSW Energy has chosen an inorganic way of expansion i.e. merger and acquisitions.

JSW Energy concludes acquisition of two hydro power plants and announces acquisition of Bina thermal plant from Jaiprakash Power Ventures Ltd.

The deal will strengthen JSW Energy’s power generation business and help Jaiprakash to deleverage its debt laden Balance Sheet

THE TRANSACTION

Transaction I: – JSW Energy concluded acquisition of 100% of the securities of Himachal Baspa Power Company Limited (HBPCL) a WoS of Jaiprakash Power Venture Limited (JPVL), which has two operating hydropower assets:-

- 300 MW Baspa – II HEP and

- 1,091 MW Karcham Wangtoo HEP

Transaction II:- JSW Energy to acquire 100% stake in the 500 MW Bina Thermal Power Plant located in the Sagar, Madhya Pradesh from JVPL.

ABOUT THE GROUPS

JSW GROUP

JSW group is a $11 billion conglomerate, a part of the O.P. Jindal Group. JSW has set up business facilities in various core sectors of India. The group has following verticals:-

- Steel

- Energy

- Infrastructure

- Cement

JSW Steel Ltd, JSW Energy, JSW Infrastructure, Ispat industries Ltd are subsidiaries of JSW Group. The group has 3 listed companies JSW Holding Limited, JSW Steel Limited and JSW Energy Limited.

JAYPEE GROUP

The Jaypee Group is a conglomerate based in Noida, India. It was founded by Jaiprakash Gaur which is involved in well-diversified infrastructure conglomerate in India with interests in Civil Engineering and Construction, Cement, Power, Real Estate, Expressways, Hospitality, Golf Courses, Sports and Education (non-profit).

Jaypee group has three listed Companies Jaiprakash Associates Limited, Jaiprakash Power venture limited and Jaypee Infratech limited.

Both the groups have a significant presence in the Infrastructure sector. The sector is capital intensive with long gestation. If the earnings do not start early enough, it will culminate into huge cost overruns.

Currently, Infrastructure sector is facing serious downturn as a result of lack of strong government policy. In such subdued scenario, Merger &Acquisition is proving to be a saline for many companies.

ACQUIRER COMPANY- JSW ENERGY LIMITED

JSWEL was incorporated in 1994 as the energy vertical of the JSW Group. The company has been in the power generation business since 2000 and later ventured into the transmission, distribution and trading business as well. The Company has an operational capacity of 4,531 MW. The company was one of the earliest private entrants into the power sector after liberalisation. JSW Energy is a full-spectrum integrated power Company with presence across the power value chain like

- Power generation

- Power transmission

- Mining

- Power Plant equipment manufacturing

- Power trading

Jaigad Power Transmission Limited (Power Transmission vertical of JSW Energy) is a Joint Venture between JSW Energy and Maharashtra State Electricity Transmission Company Ltd.

Toshiba JSW Turbine and Generator Private Ltd. has been incorporated with a shareholding of 75% by ToshibaCorp, Japan and 25% by JSW Group to manufacture highly efficient super- critical Steam Turbines and Generators for thermal power plants,

JSW Energy is working on power solutions in the states of Karnataka, Maharashtra, Rajasthan, Himachal Pradesh and Chhattisgarh.

An earlier acquisition of acquisition HBPCL marks the entry of JSW Energy into hydro power generation business making the company largest private sector hydro power generator in India.

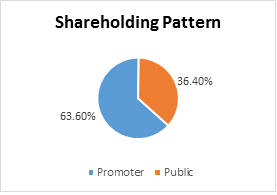

Shareholding Pattern

TARGET COMPANY- JAIPRAKASH POWER VENTURES LIMITED

JVPL currently owns and operates 2,951 MW of power capacity, which includes 1,791 MW of hydro capacity and 1160 MW of thermal capacity. With the ongoing commissioning of 2nd unit of 660 MW of its 1,320 MW Nigrie Thermal Power Plant in MP, and upon completion of the 1,980 MW Bara Thermal Power Plant in UP, it will have a generation base of 5,500 MW.

Currently selling off its business is the only option available with JPVL as firstly, no investor will be ready to invest in a debt-laden company and secondly, the company has lost almost half of its market cap in a year hence further dilution could result in losing a majority in the company.

TRANSACTION I

JSW Energy concluded its last year announced acquisition of 100% of the securities of HBPCL from JVPL, which has two operating hydro power asset:-

- 300 MW Baspa – II HEP and

- 1,091 MW Karcham Wangtoo HEP

STEPS OF THE TRANSACTION

- Formation of SPV i.e. the acquisition of the Baspa Project and Karcham Project happened through Himachal Baspa Power Company Limited (HPBCL), a Special Purpose Vehicle.

- The assets of Baspa Project and Karcham Project, which was earlier part of JPVL, have been transferred to HPBCL on a slump sale basis.

- Later on, JSW Energy acquired 100% Stake in HBPCL.

Valuation of both the hydro plants

JSW Energy acquired both the plants for an Enterprise value (EV) of INR 9275 crore. An additional consideration of INR 300 crore may become payable upon receipt of certain additional consents and approval related to the Karcham Wangtoo HEP on or before September 2020. Thus, EV 9575 (9275+300) implies value per MW about INR 6.88 crore.

Enterprise Value as per valuation report

INR in crore

| Particulars | Amount |

| Enterprise Value of Karcham Project | 8262 |

| Enterprise Value of Baspa Project | 1353 |

| Total | 9615 |

| Consideration paid by HBPCL to JPVL | 3750 |

The difference in Enterprise value and Consideration is due to a debt of the transferred undertakings.

The total consideration of INR 3750 crore has been paid by HBPCL to JVPL partly in the form of equity shares and non-convertible debentures.

HBPCL issued 1, 25, 00,000 equity shares of face and paid up value of INR 10 each aggregating to INR 1250 crore and 25, 00, 00,000 13% debenture of face and paid up value of INR 100 each aggregating to INR 2500 crores to JPVL. If we assume the same consideration will be paid by JSW Energy to JVPL, the actual immediate outflow by JSW energy to buy 100% stake is around INR 1250 crores.

TRANSACTION II

JSW Energy Ltd. has entered into a binding Memorandum of Understanding (MoU) with Jaiprakash Power Ventures Ltd. (JVPL) of the Jaypee Group to acquire 100 per cent stake in the 500 MW Bina Thermal Power Plant located in the Sagar, Madhya Pradesh.

The plan to acquire BINA Power Project will enhance the capacity to JSW energy to over 5000 MW.

In 2008, JPVL acquired Bina plant from Aditya Birla Group. The plant was set up by the Aditya Birla Group to set up a Thermal Power Plant at Bina but didn’t pursue it after the initial process.

The performance of BINA Thermal power Plant

In million units

| Actual Performance | |||||

| FY- 2014-15 | Gross | Net Saleable | AuX% | PLF % | PAF % |

| Total | 2444.74 | 2236.95 | 8.50% | 55.36% | 92.47% |

Aux:- Auxiliary Consumption PLF:- Plant load Factor PAF:- Plant Availability Factor

Further, Plant supply its 70% of the installed capacity on long-term basis to the government (Madhya Pradesh Power Management Company) as per the tariff approved by Madhya Pradesh Electricity Regulatory commission and the balance being sold as merchant power.

Valuation of BINA Thermal Plant

Both the companies are silent about the price of the deal. However, if we assume the EV of the BINA plant around INR 3000- 3500 crore, implied value comes to INR 7 crore JSW is paying for per MW. JPVL has taken rupee term loan of approximately INR 2260 crore for Bina thermal power plant. Hence, Purchase consideration will be around INR 1000- 1250 crore.

RATIONALE

JSW ENERGY

The deal not only helped JSW to enter into hydro power segment but also making JSW, the largest private sector hydro power generator in India. Further, The Bina plant will help JSE to achieve 5000 MW production level. In future, electricity generated from these plants can be used in JSW group’s other verticals such as steel and cement. These two power plants were the cash cows of the JPVL, generating most of its earnings. Hence the transaction could be EPS accretive within a shorter span.

JPVL

The deal is a sequel to selling its hydro-power plant for JPVL. The sale of its power project is an outcome of JPVL plan to deleverage its debt-laden Balance Sheet.

If the whole of this INR 13,075 crore (Assuming EV of BINA plant INR 3500 crore +INR 9575 is used to retire debt, the company’s debt-equity ratio would improve from 4.24 times to 2.20 times.

With the sale of these two plants, Jaiprakash Power has only one hydro power asset remaining— 400 MW Vishnuprayag Hydro Power Plant in Uttarakhand and one 1320 MW Nigrie Super Thermal Power Plant in Nigrie.

PEER COMPARISON

INR in Crores

| Particulars | JSW Energy* | JPVL* | Adani Power |

| As on 31st March 2015

(Consolidated)# |

|||

| Net Revenue | 9380 | 4140 | 19,065 |

| EBIT | 3063 | 2346 | 3582 |

| EBIT Margin | 32.65% | 56.67% | 18.78% |

| PAT | 1349 | 151 | (1,279) |

| Net Profit Margin | 14.38% | 3.64% | – |

*:- HBPCL figure in included in JPVL and excluded in JSW Energy.

#:- Includes revenue from other businesses also.

Estimated current position

INR in Crores

| Particulars | JSW ENERGY | Adani Power |

| Total Borrowing | 17,825 | 41,383 |

| Debt Equity Ratio | 2.37 | 7.22 |

| Capacity (MW) | 4531 | 10,440 |

| Debt/MW | 3.93 | 3.96 |

| Market CAP

(As on 21st September 2015) |

13,933 | 7,100 |

| Mcap/MW | 3.07 | 0.68 |

Above figures are subject to error.

It seems the inorganic strategy for expanding its power generation business is helping JSW Energy very well to stay ahead of its peer. Though JSW Energy is half in terms of capacity, JSW Energy’s Market Cap is almost double than that of Adani Power. The increase in debt level will pull down JSW Energy’s interest coverage ratio. However in the long term, debt level will come down if acquisition worked well for them.

CONCLUSION

The transaction is win–win for both the parties to the transaction considering their core objectives. AS JPVL is having limited options to pare its debt urgently, so a sale of its family jewel also may be justified. For JSW Energy, it is God sent opportunity to quickly scale up operations at a depressed price. If JSW energy is able to sustain its growth post acquisition, it will definitely have to look for further acquisition opportunities.

{kind=link}

{kind=link}