Mahindra & Mahindra Limited (“M&M” or “Acquirer”) is a flagship company of Mahindra Group which is engaged in the manufacturing and sale of passenger cars, Heavy, Medium & Light commercial vehicles, Tractors, etc. The equity shares of the company are listed on nationwide bourses.

SML ISUZU Limited (“SML” or “Target”) is a listed company in India primarily in the business of manufacturing and sale of light commercial vehicles (LCVs) and medium commercial vehicles (MCVs) in the automobile industry and has a product portfolio comprising buses, trucks, and specific application vehicles. Incorporated in July 1983 as Swaraj Vehicles Ltd, changed its name to Swaraj Mazda Limited SML started commercial production in 1885 with promoters like Punjab Tractors Limited & Mazda Motor & Sumitomo from Japan. In 2006, SML signed a technical collaboration with Isuzu Motors.

In 2009, Sumitomo acquired a stake from Punjab Tractors, which was, by that time was acquired by M&M. Thereafter, the company was renamed to its current name, and Isuzu raised its stake to 15% in SML, which continued to be classified as a public shareholder.

Proposed Transaction:

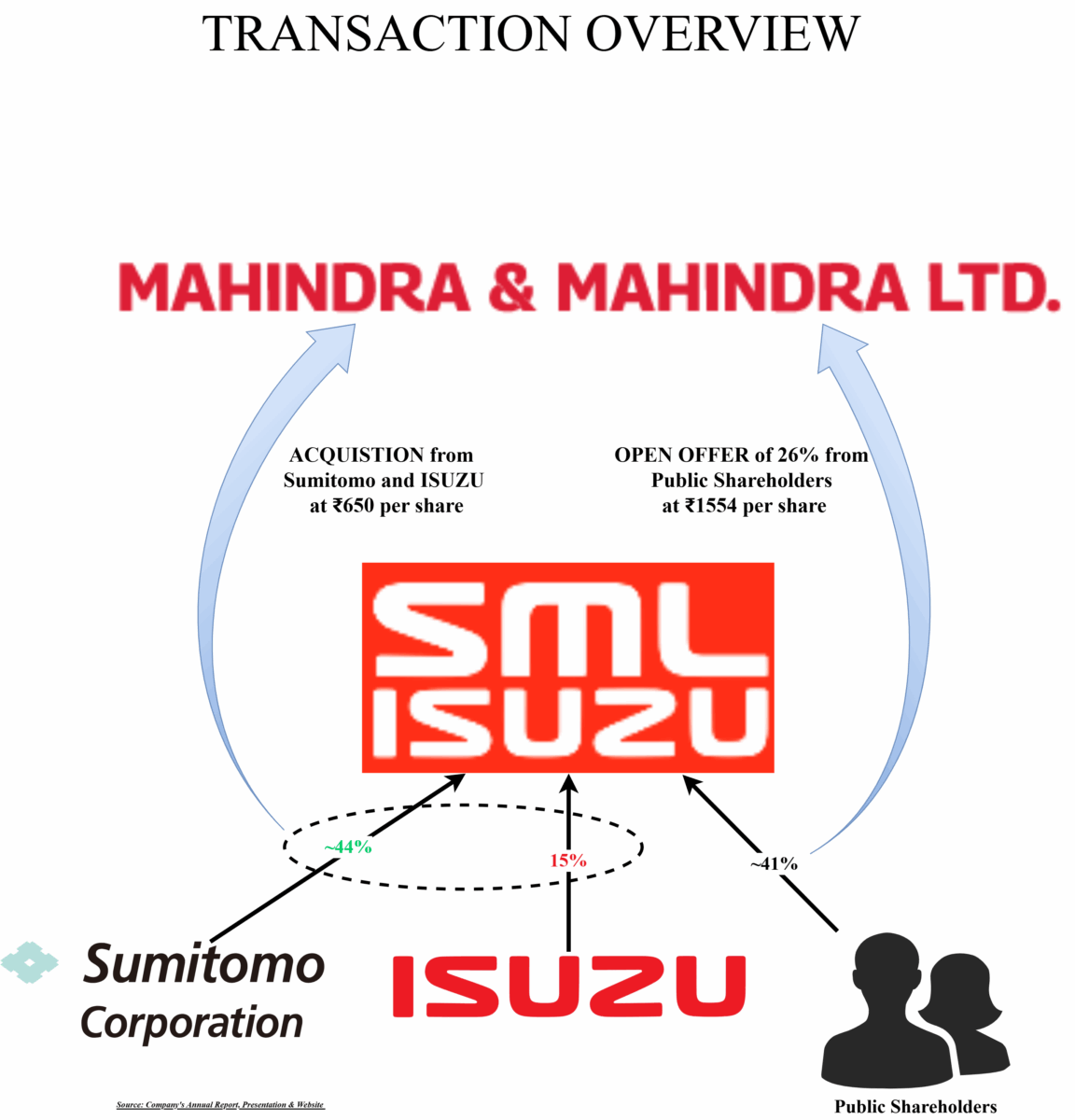

M&M has proposed the acquisition in the following manner:

- Purchase of 43.96% equity stake from Sumitomo Corporation, Japan and 15% equity stake from Isuzu Motors Limited in SML. The consideration for this is proposed at ₹650 per share amounting to a total of ₹555 crores.

- Secondly, an open offer to purchase up to 26% of equity shares from public shareholders of SML for a consideration of ₹1554 per share pursuant to the provisions of the SEBI takeover code regulations.

With two different considerations, M&M will buy circa 85% (if all shares are tendered in the open offer) for a consideration of ~₹1139 crore.

Rationale for the Deal & Immediate Actionable

M&M acquired a majority stake in Punjab Motors in 2007 which made it an indirect shareholder of SML. They sold their stake in SML to Sumitomo Corporation in 2009, but M&M got introduced to SML capabilities and its culture.

Over a period of time, M&M started losing its market share mainly in Light Commercial Vehicle (LCV) from 5% to 3%. From 2023, it has started to refocus on the LCV segment. M&M has also become 4th Original Equipment Manufacturer in the Commercial Vehicle Segment.

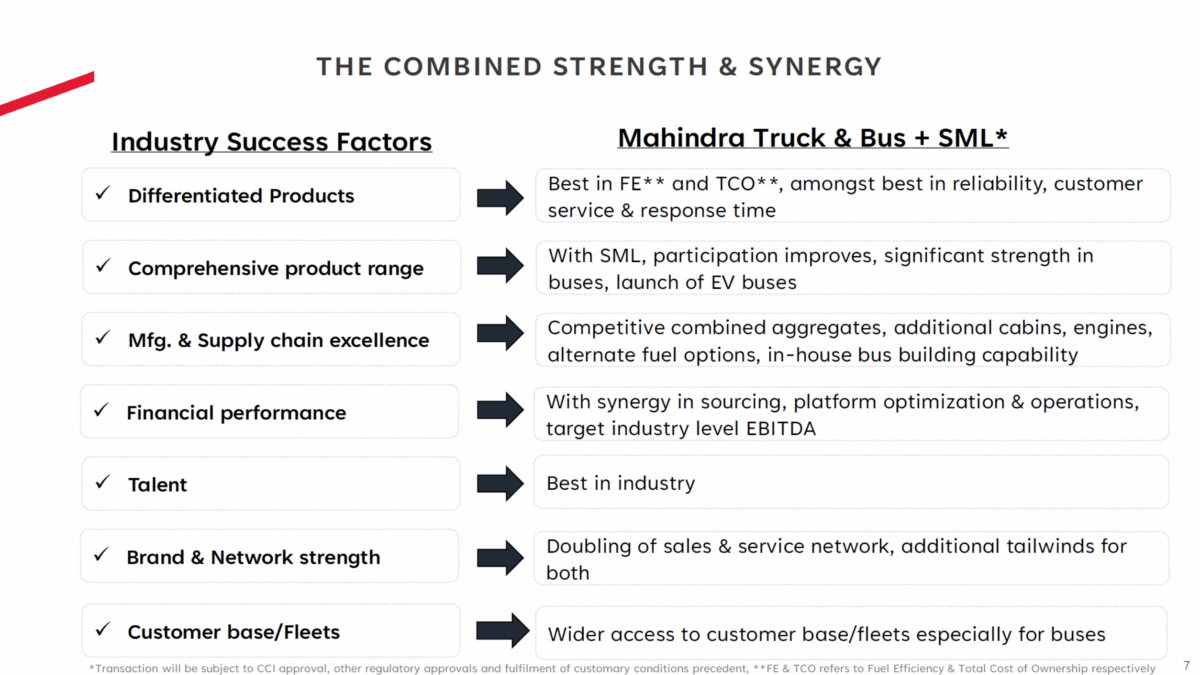

M&M management has decided to focus on the bus segment. SML holds circa 16% market share in light & medium buses which M&M is looking to leverage along with its light commercial vehicle segment. SML has developed CNG technology in buses and has launched pilot electric buses which becomes the sweet spot for M&M to capture.

SML, with experience in the past, has become a natural choice for M&M. The transaction should help M&M to grow its market share & capabilities inorganically. Other than that, M&M has chalked down multiple synergies like sharing of platforms, manufacturing & supply chain efficiencies, improved financials and others. One of the important synergies will also be on distribution side where M&M & SML will try to have complimentary access across both dealership which shall provide better after-sales to customers. Unlike other big players, M&M has a limited distribution channel which hinders their after-sales support. With SML, they will be able to create more robust distribution and servicing chain.

- Brand with more than 4 decades of history at good valuation

- To improvise market share mainly in intra-city bus segment

- Swift entry into CNG & EV buses

- Enhancing after-sales experience through complimentary access to SML dealerships

- Additional manufacturing capability in North India

Further to achieve its ambition of having 10-12% market share in FY 2031 & 20 %+ by FY 2036, enough capacity is available with SML (in terms of land) and no incremental capex is required as of now to streamline the existing facility of SML. Top management of SML shall continue to remain as it is and SML brand will continue to be operated. As per M&M, there is no need for immediate consolidation of M&M & SML businesses to derive envisaged synergies. Thus, SML is likely to operate as a separate listed entity with M&M as a promoter.

As Isuzu will make an exit, there won’t be any further technological support provided to SML. SML will change its name post-completion of the proposed acquisition. M&M will not look for any other acquisition in the near future and focus on integration of SML with M&M.

Total Consideration & Funding

Japan’s Sumitomo Corporation and Isuzu Motors have been looking to exit SML Isuzu for a while now. As a part of a broader plan to move away from non-core businesses, they feel it is the right time to finally offload their stake.

M&M is offering ₹650 per share to the promoters’ entity of SML. The price, which is more than ~60% less than the market price., It is one of the steepest discounts seen in recent times for a strategic acquisition. While, if the open offer is successful, M&M will spend a larger amount to acquire 26% stake from public shareholders than the 59% stake from SML’s promoters and technology partner.

The reason for the difference cited by M&M is, ‘the equity shares of SML are thinly traded and does not reflect fair pricing’. The open offer price is derived using pricing norms prescribed under the SEBI Takeover Code Regulation.

For Mahindra, it’s a chance to buy a CV brand with profitable operations, in-house R&D, a CNG and EV-ready product line and a manufacturing plant in Punjab… all for less than half its worth utilising through its surplus funds.

Key financials

In relation to SML, M&M is too large and has revenue of circa INR 76,155 for FY 2024 from the automotive segment (excluding tractors).

M&M Strategy

The deal gives Mahindra a share in the ILCV (Intermediate Light Commercial Vehicle) bus segment with access to SML’s 16% market share. M&M thus instantly shall become the fourth-largest original equipment manufacturer with a 21% market share in the bus segment.

And why does Mahindra believe buses and trucks could be a big opportunity?

Well, because buses and trucks make up less than 8% of India’s vehicles (excluding two and three-wheelers), but they account for 35% of road transport emissions. And if India wants to cut these emissions, this is where the axe must fall.

This brings us to e-buses. India’s bus fleet is massively under-electrified. India currently has around 11,000 e-buses on the road — but that number is rising quickly. FY24 alone saw 3,600 new e-buses sold, up about 80% year-on-year. And as per CareEdge, that annual number could cross 17,000 units by FY27. And companies are winning. As of FY24, five players (Tata Motors, Olectra Greentech, PMI Electro, JBM Auto, Switch Mobility) control 88% of India’s e-bus market.

E-buses, in particular, are low-hanging fruit. They run on fixed routes. They have predictable charging needs. And most importantly, they’re owned or funded by governments who are willing to spend, subsidise and experiment. For context, the central government has announced over ₹28,000 crores in e-bus funding since 2015.

So, for Mahindra, which is a leader in SUVs, tractors and electric three-wheelers, this looks like the right time to cash on this segmental opportunity as well.

Sure, it basically has no presence in this growing ecosystem right now. But with SML’s in-development Hiroi.ev, a 12m city bus platform, and experience in staff and fleet of buses, Mahindra suddenly has a product plus a platform to compete. It may not chase rental orders right away. But it can target private fleet operators, mobility contracts, and tier 2 or 3 transport networks. And all of these are currently seen as fast-growing segments.

And lastly, the strategy also fits into the company’s grand EV plan. It has committed to investing ₹12,000 crores in the EV business MEAL (Mahindra Electric Automobile Limited) over the next three years and introduce variants under its different verticals.

Conclusion

The deal in a potentially high-growth industry is between an uninterested promoter and a willing strategic and financially strong buyer who has the capabilities to nurture and grow the business and take this to new highs. The deal shall still require approval from the Competition Commission of India. So, in the most likely scenario, it will create substantial value for all stakeholders, including customers.