In order to make government-owned general insurance companies profitable and achieve economies of scale, finance minister Arun Jaitley in this year’s budget announced a plan to merge three insurers – National Insurance, United India Insurance and Oriental Insurance. The other company New India Assurance, which is the largest state-owned general insurance company in the country, will remain as it is as it is already listed in the bourses.

However, if the proposed merger goes through, the combined entity will be much bigger than New India Assurance both in terms of premium collections and assets under management. According to data from Insurance Regulatory and Development Authority of India (IRDAI), gross direct premium (within and outside India) of New India Assurance was Rs 21,598 crore in FY17. The company accounted for 16.5% of the gross direct premium of non-life insurers including standalone health insurers in FY17.

In contrast, the gross direct premium of the three companies which are likely to be merged is Rs 41,462 crore, accounting for around 32% of the total gross direct premium in FY17. The merged entity will also subsequently go for listing. The merged entity may be valued at Rs 60,000 crore based on its investment book, net worth and real estate. Thus a single merged entity of the three companies will be bigger in size and the valuation will improve significantly. Moreover, the merger will lead to better pricing and better underwriting profitability.

Table 1: Gross direct premium of general and health insurers (All figs in Rs. Crores)

| Within & Outside India | 2015-16 | 2016-17 |

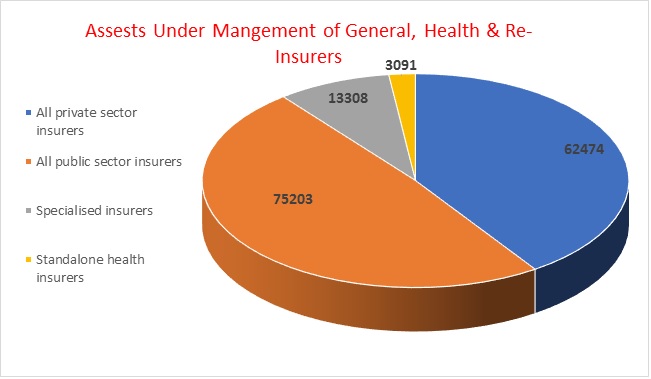

| All private sector insurers | 39694 | 53805 |

| All public sector insurers | 50644 | 63060 |

| National Insurance | 12019 | 14282 |

| New India Assurance | 17763 | 21598 |

| Oriental Insurance | 8612 | 11117 |

| United India Insurance | 12250 | 16063 |

| Specialised insurers | 4842 | 8247 |

| Standalone health insurers | 4153 | 5858 |

| Grand total | 99333 | 130970 |

The general insurance industry was nationalised in 1973 by taking over the existing private non-life insurance companies. That way, four government general insurance companies and one reinsurance company (General Insurance Company) were established. Later in 1999, the government opened up the insurance sector to private sector players. The entry of new private non-life insurers resulted in a decline in the market share of government-owned non-life insurance companies or gross direct premium and dropped to around 48% in FY17 from 56% in FY12.

Table 2: Insurance Claim Ratio for FY 16-17 (%)

| All private sector insurers | 79.1 |

| All public sector insurers | 100.02 |

| National Insurance | 97.25 |

| New India Assurance | 91.28 |

| Oriental Insurance | 112.11 |

| United India Insurance | 107.08 |

| Specialised insurers | 120.22 |

| Standalone health insurers | 56.47 |

All the four government-owned general insurance company offer general insurance as well as cover for threats from accidents such as fire, engineering, aviation, liability, marine, motor and health insurance. Overall, the general insurance industry reported highest ever year-on-year growth of 32% in gross direct premium in FY17 because of crop insurance as compared to just 14% year-on-year growth in FY16.

Will the merger help?

In theory, it will help as the merger will create a giant entity, achieve scale and strengthen the company’s balance sheet. The merger will also help the government to sell stake and add to the disinvestment kitty. Last year, the government sold stakes in New India Assurance and General Insurance Corporation (GIC Re) to add money to the disinvestment kitty. The merger will bring more synergies and consolidation of market share and add to the enterprise value. The merged entity and the subsequent listing once done will improve operational efficiencies and will positively impact policyholders in the long-run.

However, there are fears that the merged entity will control about one-third of the total non-life insurance business in the country and such a monopoly may lead to less focus on customer services. As the general insurance industry is very fragmented, consolidation will help the new merged entity to tap new markets, especially in new areas like health insurance as the government plans to roll out the massive National Protection Scheme covering 10 crore households. At present, there are 24 general insurance companies, six standalone health insurers and one reinsurance company.

However, despite strong demographic profile, the penetration of general insurance is still abysmally low at 0.77% in 2016 as compared to the world average of 2.81% in 2016, according to data from Swiss Re Sigma volumes. In terms of profitability, private insurance companies have lower claims ratio than state-owned companies. In order to increase the penetration, general insurance industry will have to work on transforming product portfolio, operating models and focus on digital penetration.

The idea of selling stake in government-owned general insurance companies was first mooted by finance minister Arun Jaitley in his budget speech of 2016 where he indicated that the companies would be listed on stock exchanges. He also highlighted that public shareholding in government-owned companies is a means of ensuring higher levels of transparency and accountability. Since then, the government-owned insurers were working on listing. But now with the government deciding to merge the three insurers, the companies will have to go back to their drawing boards once again.

In 2016, the insurance regulator, Insurance Regulatory Development Authority of India allowed all non-life insurance companies including standalone health insurers with over 10 years of existence (for life insurance companies, it is 8 years) to mop up money through listing from the primary market. The regulator had also underlined that all companies meeting the stipulation on minimum years of existence for listing for listing should initiate steps to get listed by 2020.

The insurance regulator had also scrapped the usual embedded value norm for listing non-life insurance companies. Embedded value is an actuarial practice used to value an insurance company. In other words, it is the present value of the future profits expected from the business. Instead, these companies will be required to make additional disclosures on risk factors which are specific to these companies such as reserves, asset-liability mismatch, adequacy of premium and current financial position.

Not is a sound position

The general insurance industry plays an important role to protect people and material in case of any unforeseen incidents, calamities and health disorders. So, in such a case it is very prudent the companies are well capitalised and have adequate reserves. According to the solvency standards set up by the regulator, companies have to maintain a solvency ratio of 1.5.

Every insurer shall maintain an excess of the value of assets over the amount of liabilities of not less than an amount prescribed by the Irdai, which is referred to as a Required Solvency Margin. This ratio measures to what extent an insurance company has capital to meet claims from all the business it has covered. Two companies — United India Insurance and Oriental Insurance have solvency ratio of 1.15 and 1.11, respectively as on March 2017. National Insurance has solvency ratio of 1.9. Topping the list among government-owned insurers is New India Assurance with 2.19 as on March 2017, which is even higher than many private sector insurance companies. So, for United India Insurance and Oriental Insurance, a lower-than-prescribed ratio means the companies should not underwrite new policies. So, there were serious concerns on the underwriting performance and it was considered more appropriate to merge the three companies.

Moreover, the profitability of most general insurance companies including the four government-owned has been under pressure for quite some time because or increasing underwriting losses and higher claims, especially in health and motor insurance. So, rationalisation of costs after the merger will help bring down the combined ratio, which is a measure of profitability after factoring in the incurred losses and expenses.

Challenges for capturing synergies

To get substantial benefits out of the merger, post-merger top management must look at various aspects so that not only administrative cost is optimized but also cost of servicing the claims are also rationalised so that customers also get the cover at minimum premium. The merged entity should be able to come out with the unique products to increase its reach. Challenges to get substantial synergy benefits are

HR and cultural

The biggest challenge for the merger to work will be to align the workforce and systems. All the three companies work on different technology platforms that have to be brought together. The proposed merger may render about 15,000 staff redundant.

Products and Policies

Secondly, the products offered by the three companies have to be rationalised as they offer various type of products to their customers. Agents and commission for them also needs to be optimized an to develop new and integrated distribution channel,

Legal

The government will have to amend the Insurance Nationalisation Act for the merger to take place and the share transfer will not be a problem, as 100% is held by the government. The process is likely to be completed by the end of financial year 2018-19.

Infrastructure

The merged entity will have 30 regional offices as against 90 of the three firms put together at present and around 900 branches. So, more than physical merger, emotional integration of the companies is more important to achieve the desired results.

Customers

Ensuring a smooth renewal and claim settlement process will have to be a top priority of the merged entity. Though most of the products are of shorter term, health insurance products are of longer term and there could be trail of claims. Even servicing the products with varied characteristics could be a challenge for the merged entity.

Things about the merger will be clearer once the road map is made public after consultations with all stakeholders. While the merger will be a pragmatic move, it has to properly managed. It is the implementation which will be the key to reaping the benefits of the merger. It will require seamless integration of people and process. Policy holder servicing issues will have to be tackled efficiently.