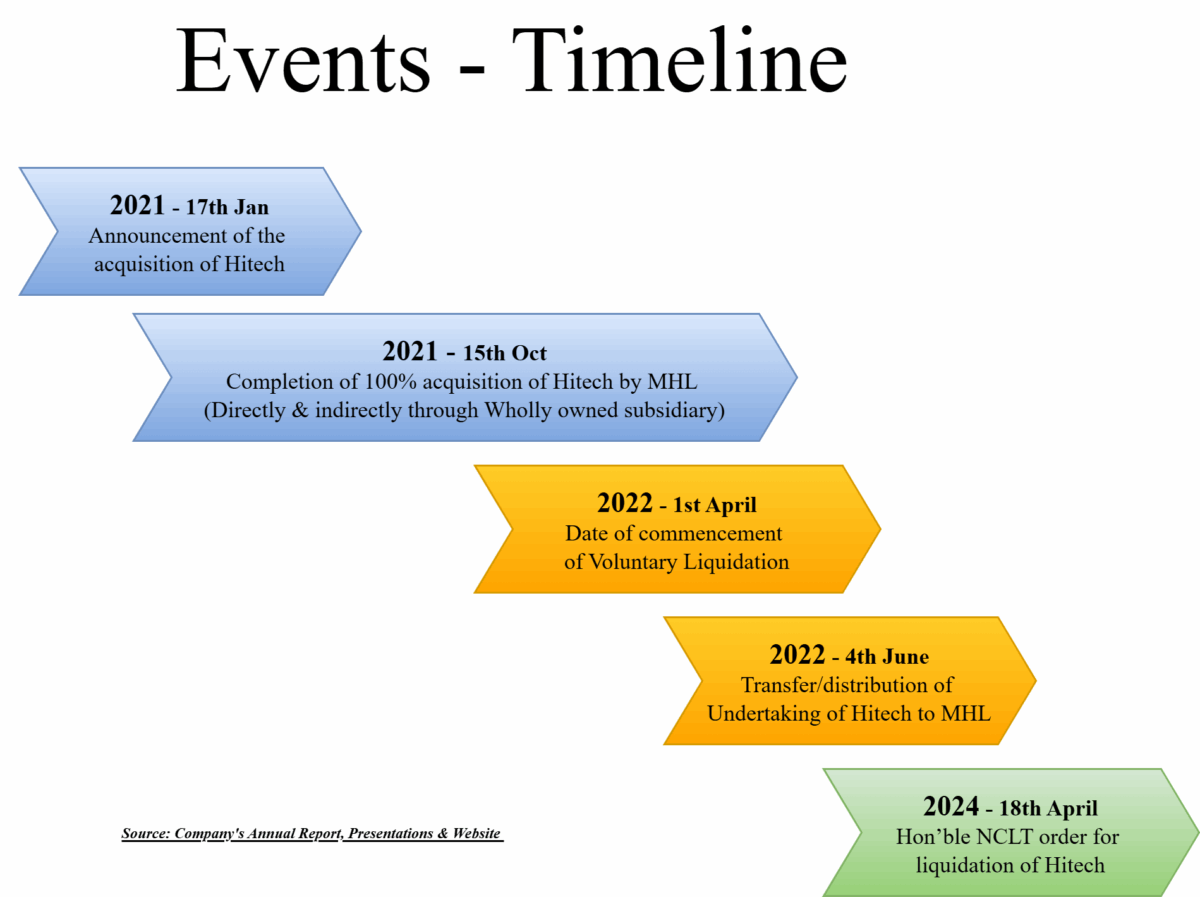

In 2021, Metropolis Healthcare Limited (“MHL”) announced a proposed acquisition of 100% equity shares of Dr. Ganesan’s Hitech Diagnostic Centre Private Limited and its subsidiary (‘Hitech’) for consideration in the form of cash of INR 511 crore plus MHL’s equity shares worth circa INR 100 crore. Though the proposed acquisition went through turbulence and at one time it appeared that the deal may not happen, MHL successfully closed the transaction in October 2021 with the entire cash consideration of INR 636 crore.

Later in February 2022, MHL announced that the Hitech has principally decided on a voluntary liquidation under Section 59 of the Insolvency and Bankruptcy Code, 2016 read with Insolvency and Bankruptcy Board of India (Voluntary Liquidation Process) Regulations, 2017 and the same was approved by its shareholders at its extra-ordinary general meeting held on 1st April 2022 (“Voluntary liquidation commencement date”). Thereafter, the appointed liquidator of Hitech transferred the entire business undertaking of Hitech including its investment in its subsidiary on a going concern basis to MHL, being a shareholder of Hitech.

The consolidation of Hitech business with MHL was achieved through voluntary liquidation and not as merger or demerger as normally followed for such transactions. Let us understand the nitty-gritties and broad reasons for choosing liquidation over a merger or demerger.

The dates of key events are depicted below:

Accounting Treatment

Acquisition and Voluntary Liquidation Period

MHL recorded the unrelated acquisition transaction & other transactions as follows:

- Standalone balance sheet for FY 21-22 of MHL showed the investment in Hitech (under investment in subsidiaries and joint venture) as ₹63,142 lacs in non-current assets.

- Consolidated balance sheet for FY 21-22 of MHL reflected Goodwill of ₹36,445 lacs. While in the Notes to account Goodwill amount is ₹28,181 lacs along with values for the Brand name as ₹29,387 lacs and non-compete fees as ₹3,229 lacs.

| Particulars | Amount (₹ lacs) |

| Identified tangible assets | 2,088 |

| Hitech Brand | 29,387 |

| Non-Compete Agreement | 3,229 |

| Total Intangible Assets | 32,616 |

| Purchase Consideration | 63,142 |

| Goodwill after other adjustments | 28,181 |

The notes mentioned Goodwill after other adjustments, and it is not clear about these adjustments and the difference in value of ₹8,224 lacs as shown in the balance sheet.

| Particulars | Amount (₹ Lacs) |

| Goodwill as per notes to account | 28,181 |

| Goodwill as recorded in balance sheet | 36,445 |

| Difference | 8,264 |

- Announcement of the voluntary liquidation was done in April 2022. But MHL has given effect of the liquidation as per the requirements of Appendix C to Ind AS 103 “Business Combination”, to as if it had occurred from the beginning of the preceding period (i.e., October 22, 2021) and accordingly preceding period figures (i.e., in FY-21-22) had been revised. Pursuant to the above and distribution of business Hitech to MHL the following entries were passed in the books of MHL for FY 21-22:

- MHL had recorded all the assets, liabilities and reserves of Hitech, at their carrying values and in the same form as appearing in the consolidated financial statement of MHL as on the voluntary liquidation commencement date, by applying the principles as set out in Appendix C of IND AS 103 ‘Business Combinations’ read with ITFG Bulletin 9; Issue 2; Situation B and prescribed under Companies (Indian Accounting Standards) Rules, 2015 issued by the Institute of Chartered Accountants of India.

- The financial statements of MHL reflect the financial position based on consistent accounting policies.

- Any loans, advances or other obligations (including but not limited to any guarantees, letters of credit, letters of comfort or any other instrument or arrangement which may give rise to a contingent liability in whatever form) that are due between MHL & Hitech, if any, ipso facto, stand discharged and come to end and the same is eliminated by giving appropriate elimination effect in the books of account and records of MHL.

- Investments in shares of Hitech held by the MHL have been adjusted against Share Capital of Hitech and the difference between the cost of investment of Hitech in the books of MHL has been adjusted against the balance of reserves and surplus of MHL post-liquidation.

- The identity of the reserves has been preserved and appear in the financial statements of MHL in the same form in which they appeared in the financial statements of Hitech.

The voluntary commencement date is carefully chosen as 1st April 2022, as in the consolidated financials of MHL, all intangibles relating to Hitech get recorded which can be classified in the standalone balance sheet of MHL in accordance with the above.

As evident from the table, effectively, the investment in the subsidiary, i.e., Hitech, was classified as goodwill, brand and non-compete fees.

Post-Liquidation Period

| Particulars (as on 30th Sep, 2024) | Amount (₹ lacs) |

| Total Equity | 1,10,580 |

| Investment in Subsidiaries | 3,665 |

| Goodwill | 41,542 |

| Other intangible assets | 38,039 |

| Total Assets | 154,154 |

Post liquidation, as well, goodwill & intangibles are maintained and effectively the investment amount in Hitech has been preserved. If MHL had announced the merger, its investment in Hitech would have been cancelled and an equivalent adjustment would have been made by adjusting (debit) to reserve & surplus which would have ushered in significant correction of net worth. This has been done by MHL in FY 2022 when it announced the merger of several acquired wholly owned subsidiaries with itself.

| Particulars | Amount in lakhs |

| Total identified assets acquired pursuant to the merger | 9810 |

| Cost of investment in subsidiaries in the books of MHL | 12705 |

| Net impact transferred to other equity | (2895) |

A similar impact of the merger of Hitech with MHL would have been so large that it would have adjusted (~40-50%) of the standalone net worth of MHL significantly.

Direct Taxes

A compliant merger would have been ’Direct –Tax’ efficient vis-à-vis voluntary liquidation which is taxable in the hands of MHL. First tax incident would be under section 2(22)(c) of the income tax act 1961 which says any distribution made to the shareholders of a company on its liquidation to the extent to which the distribution is attributable to the accumulated profits of the company immediately before the liquidation shall be considered as “Deemed Dividend”.

Though precise numbers are not available, considering the MHL Annual report for FY 2022, the reserve & surplus of Hitech was ₹ 4,340 lacs as on 31st March 2022 immediately prior to the commencement of liquidation. Assuming the entire amount is accumulated profits, the deemed dividend in the hands of MHL is a maximum of ₹ 4,340 lacs. Depending upon the opted regime, MHL may have taken an exemption of this dividend on dividend distributed by MHL to its shareholders.

The remaining amount i.e., consideration deducted by the deemed dividend, will get taxed under section 46 of the Income Tax Act, 1961.

| Particulars | Amount (₹ lacs) |

| Value of distributed business (as per NCLT order) | 64,537 |

| Assumed Deemed Divided | 4,340 |

| Remaining amount /Consideration under section 46 | 60,197 |

| Less: Cost of acquisition | 63142 |

| Short term Capital Loss | -2945 |

Secondly, as per explanation 3 to section 32 (1) of the Income Tax Act, MHL may claim depreciation on intangible assets acquired other than goodwill which will provide an additional advantage.

As in both cases, merger vis-à-vis voluntary liquidation, there is a transfer of undertaking, same is exempt from any GST.

Conclusion

The entire transaction was structured and executed in a unique way. If one looks practically, it was in fact acquisition of the business on slump sale basis by the acquirer from an unrelated party. But if it would have been carried out as such it would not have been –

- Efficient for the target company’s promoters as consideration would have been required to be paid to the company and not directly to them.

- Merger of Hitech would have reduced its networth drastically and additionally may have lost tax breaks on some of the intangibles.

Additionally, slump sale would have resulted in tax in the hands of company plus consideration would have issued to the company instead of shareholders. Straight merger and demerger would not be commercially possible as revised deal with Hitech’s erstwhile promoters could have led to re-negotiations.. The distribution through voluntary liquidation appears to be done considering protecting the intangibles recorded and thereby net worth of MHL.