Recently Hon’ble National Company Law Tribunal, Mumbai Bench (“NCLT”) sanctioned the Scheme of Arrangement (“the Scheme”) between Mukand Sumi Metal Processing Limited (“Demerged Company” or “MSMPL”), wholly owned subsidiary of Mukand Limited, with Mukand Limited (“Mukand”) and their respective shareholders and creditors under Sections 230 to 232 and other applicable provisions of the Companies Act, 2013 the rules and/ or regulations made thereunder.

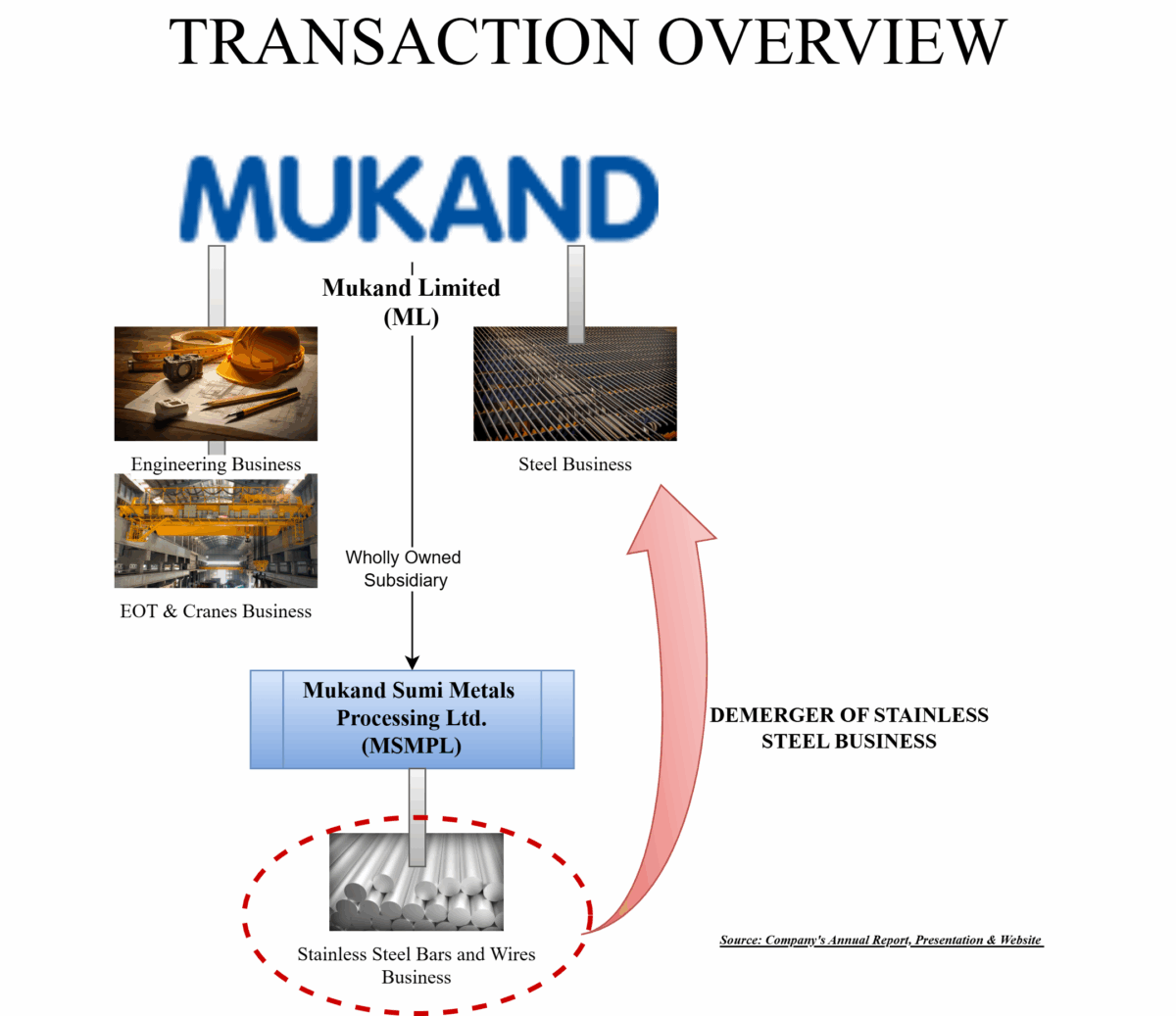

Mukand Limited is a multi-division, multi-product conglomerate which mainly deals in manufacture of special alloy steel / stainless steel, billets, bars, rods, wire rods, EOT cranes, material handling equipment, other industrial machinery, comprehensive engineering services and construction/erection services. The equity shares of Mukand Limited are listed on nationwide bourses.

Mukand Sumi Metal Processing Limited (“MSMPL”) is a wholly owned subsidiary of Mukand Limited which inter-alia, engaged in the business of stainless steel cold finished bars & wires and treasury & investment business.

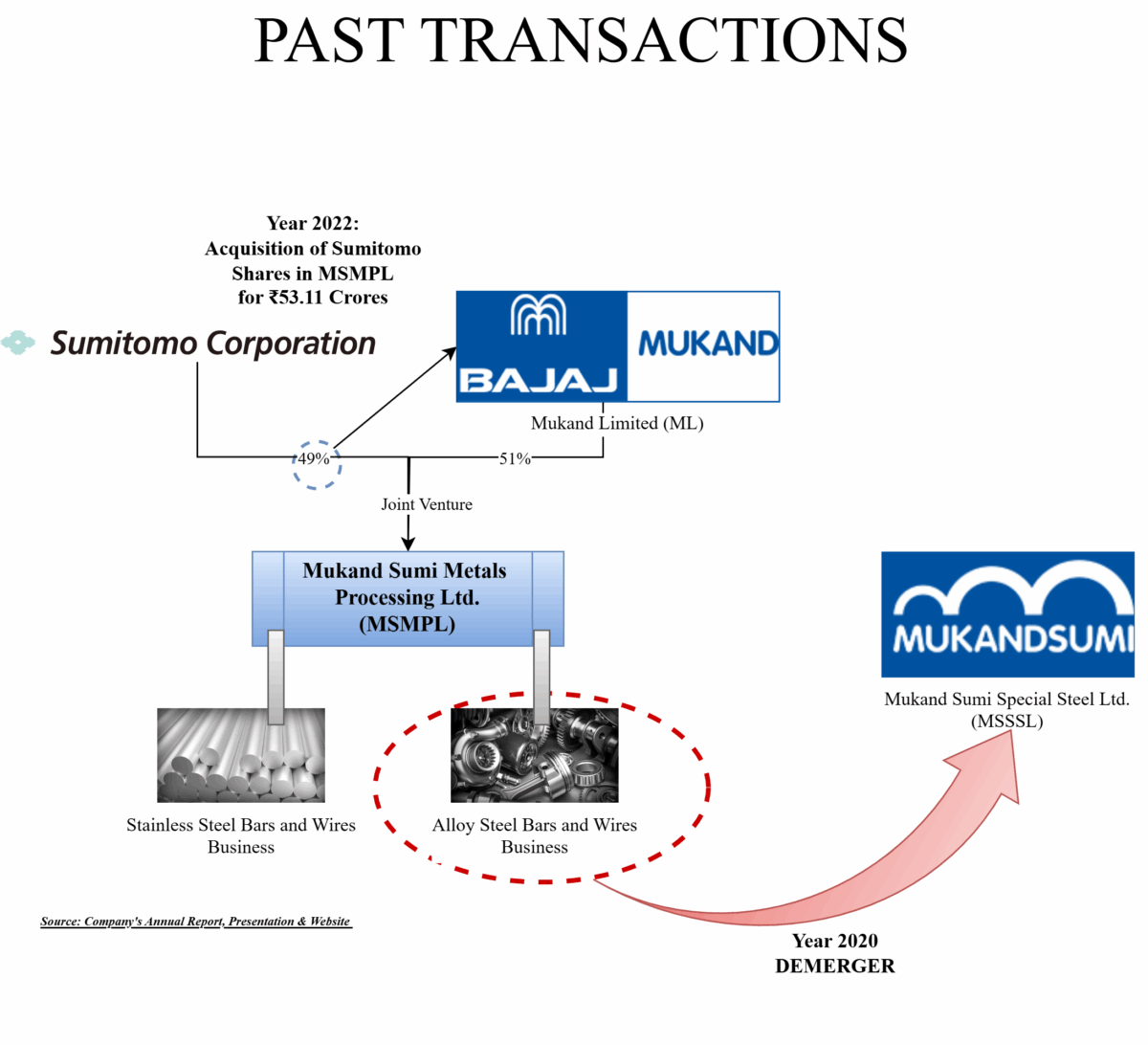

In 2020, MSMPL demerged its cold finished alloy steel bars and wires business to Mukand Sumi Special Steel Ltd. (MSSSL) has been approved by the National Company Law Tribunal (NCLT), Mumbai Bench vide its order dated June 30 2022. After demerger, MSMPL continues to carry on the business of cold finished stainless-steel bars and wires. Moreover, in terms of arrangement with Joint Venture partner–Sumitomo Corporation, Japan (SC), Mukund Limited purchased 50% equity stake of MSMPL from SC at a consideration of Rs. 53.11 Crore and MSMPL has become a Wholly Owned Subsidiary of Mukand Limited with effect from 30th September 2022.

Key events in chronological order:

- Demerger of Alloy Steel Bar business from MSMPL

- Exit of joint venture partner from MSMPL

- Demerger of Steel cold finished bars and wire business through the present scheme into Mukund Ltd

The Scheme provides for demerger of Stainless Steel Cold Finished Bars And Wires Undertaking of MSMPL, which is predominantly involved in the business of manufacturing and selling of stainless steel cold finished bars and wires, including inter alia all downstream operations for manufacturing of cold finished bars and wires, the processes of normalizing, annealing, drawing, peeling, grinding, pickling, coating and other processes in connection therewith. Effectively, through scheme, Mukand Limited up streamed its one of its business activities carried through MSMPL. The turnover of the Demerged Undertaking as on March 31, 2024, was INR 655.23 Crores which constitutes 12.55 % of the total consolidated turnover of Mukand Limited.

The Appointed Date for the Scheme of Arrangement is 1st April 2024.

Merger in the name of demerger?

As per the Hon’ble NCLT order, assets & liabilities getting transferred to Mukand Limited as on the appointed date are depicted below:

Thus, almost entire net assets are getting transferred pursuant to the above scheme. Interestingly, the order provides that the demerged company shall be dissolved without winding up. However, as per the scheme there is no such provisions which will result in winding up without dissolution of the demerged company. We believe this must be a typo error which companies will rectify through filling the necessary application before the Hon’ble NCLT.

Direct Tax Neutral Arrangement

As per the scheme & affidavit given by Mukand Limited to the Regional Director, the above demerger is in compliance with section 2(19AA) of the Income Tax Act, 1961. As per the conditions of section 2(19AA) of the act, shares are required to be issued by the resulting company to the shareholders of the demerged company holding not less than three-fourth in the value of the shares of the demerged company (other than shares already held therein immediately before the demerger by the resulting company in the demerged company).

In the present case, the entire share capital is held by the resulting company and its nominees. Thus, technically no shares are required to be issued and still it will amount to a tax compliant demerger.

Accounting Treatment & Classification of Reserve

The scheme also provides that post giving effect to the demerger, the demerged company shall adjust the debit balance of reserves including retained earnings under the head “Other equity” against credit balance of securities premium account to the extent of INR 84.69 crores.

Thus, the entire negative/debit balance of retained earning shall get adjusted against the securities premium account.

Post giving effect to the demerger, circa INR 74.29 crore (being net assets transferred on the demerger) shall get transferred (debited) to “Reserve Account” which shall again be adjusted for remaining balance in credit of securities premium account. Thus, in total post demerger:

Further, Resulting Company shall account for the Demerged Undertaking in its books as per the applicable accounting principles as laid down in Appendix C of the Indian Accounting Standard 103 (Ind AS 103) (Business Combination of entities under common control) notified under section 133 of the Act, the Companies (Indian Accounting Standard) Rules, 2015 and/or any other applicable Indian Accounting Standard as the case may be.

| Particulars | Demerged Undertaking | Remaining Undertaking |

| Net Asset Value in crore | 74.29 | 2.55 |

| % | 96.7% | 3.3% |

After recording assets & liabilities at its carrying values, the value of investment of the Demerged Undertaking held by the Resulting Company in the Demerged Company shall be adjusted and computed based on the proportion of net assets of the Demerged Undertaking being transferred in the total net assets appearing in the books of the Demerged Company on the day immediately preceding the Appointed date. Accordingly, the existing carrying value of the investment held by the Resulting Company in the Demerged Company after deducting the amount attributable to Demerged Undertaking of the Demerged Company as per this clause will be deemed as the new carrying value of the investment held by the Resulting Company in the Demerged Company.

| Investment in MSMPL in the books of Mukand Limited | 111 |

| Cancellation of Investment in the books of Mukand Limited | 107 |

| Revised investment in MSMPL | 4 |

Thus, on demerger circa INR 33 crore effect shall be adjusted (debited) to capital reserve (excluding inter-company adjustments).

Related Party Transactions

Key transactions done by MSMPL with Mukand Limited for FY 2024

| Particulars | Amount in Crore |

| Purchases | 608 |

| Services Received | 31 |

| Sales | 51 |

| Services Rendered | 5 |

MSSPL total revenue for FY 2024 was INR 655 crore and cost of material consumed was INR 623 crore. Thus, almost entire purchases are being made through Mukand Limited.

Stamp Duty

As there is no consideration for demerger from wholly owned subsidiary company to holding company, it is most likely there will be no stamp duty transaction.

Conclusion

The transaction is in fact a merger but structured as a demerger just to have the ease of set off losses and unabsorbed depreciation or any other regulatory reason. It seems by mistake NCLT mentioned in the order that the demerged company is dissolved, maybe presuming the same as a merger though in fact the scheme does not have clause for dissolution for obvious reason as this being the scheme of demerger.

This could be one of the innovative ways to consolidate subsidiary business with its holding company considering the thin difference between regulatory provisions applicable to merger vis-a-vis demerger after considering commercial aspects.