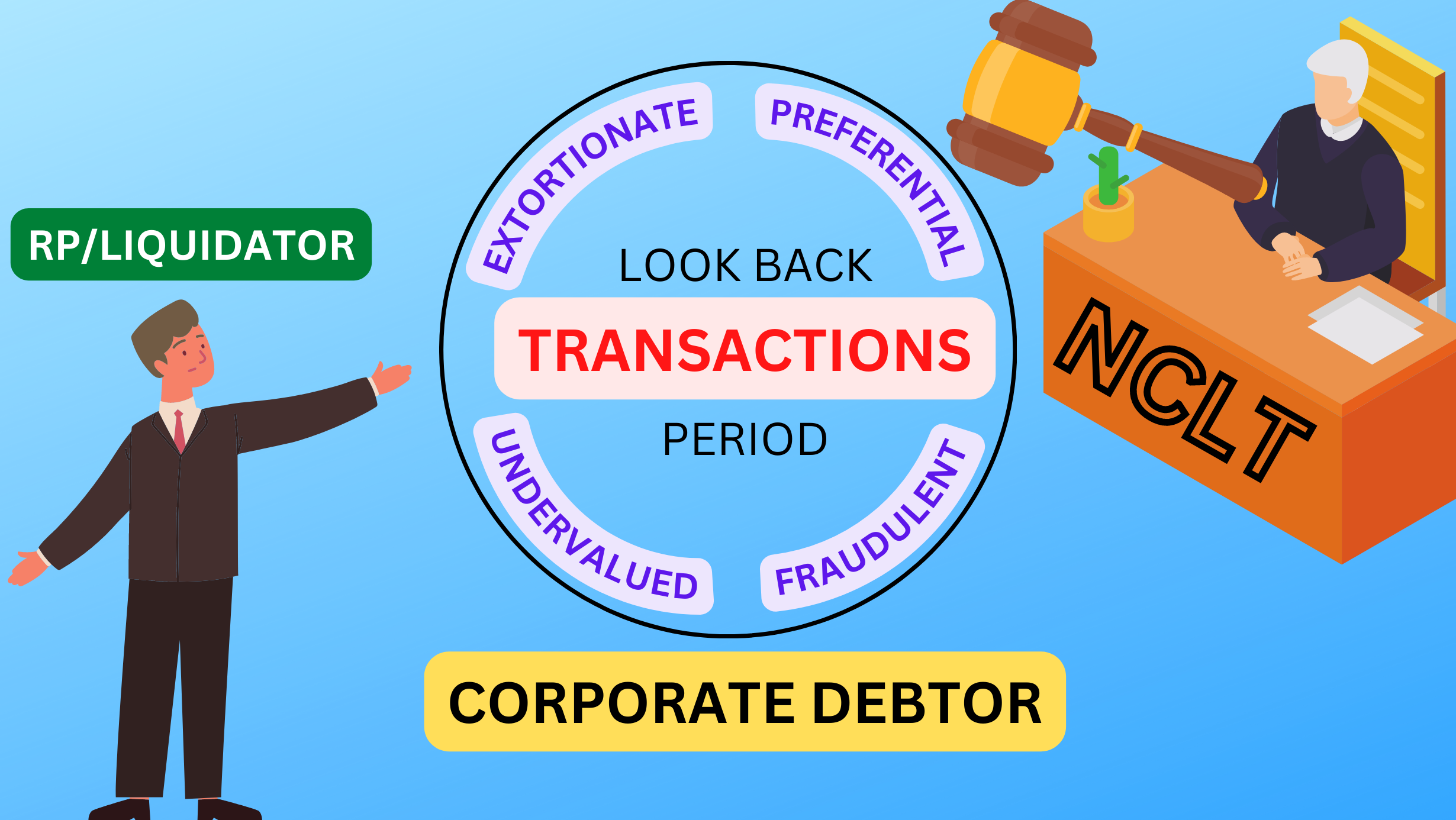

The Code has identified set of transactions, whereby a Corporate Debtor may lose value, in the run-up to commencement of the Corporate Insolvency Resolution Process (CIRP). They are known as Avoidance Transactions, comprises Preferential Transactions, Undervalued Transactions and Extortionate Transactions and Fraudulent Transactions, comprises fraudulent trading or wrongful trading. The Code requires the CIRP to recover the loss made through these transactions. These avoidance transactions and fraudulent trading together are known as PUFE (Preferential, Undervalued, Fraudulent and Extortionate) Transactions.

The Code empowers the National Company Law Tribunal (Adjudicating Authority) to claw back the value lost through PUFE transactions, based on an application of an Insolvency Professional (IP), either as Resolution Professional (RP) or Liquidator. Sections 43, 45, 50, 54F, and 66 of the Code require the RP or Liquidator to file applications in respect of PUFE transactions with the Adjudicating Authority during the CIRP or liquidation process.

To ensure that the RP files an application without fail, the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) provide timelines, requiring the RP to form an opinion if the CD has been subjected to any PUFE transactions, by 75th day of commencement of the CIRP, make a determination by 115th day, and file an application by 130th day with the Adjudicating Authority, for appropriate relief. This timeline has been held to be directory because the CD must not suffer loss for lapse on the part of the RP.

Nature of Transactions

1. Preferential Transactions: – As per Section 43 of IBC, Transactions where RP or liquidator as the case may be is of opinion that the corporate debtor has at a relevant time given a preference in such transactions as below: –

- there is a transfer of property or an interest thereof of the corporate debtor for the benefit of a creditor or a surety or a guarantor for or on account of an antecedent financial debt or operational debt or other liabilities owed by the corporate debtor; and

- the transfer under clause (a) has the effect of putting such creditor or a surety or a guarantor in a beneficial position than it would have been in the event of a distribution of assets

2. Undervalued Transactions: – As per Section 45 of IBC, Transaction is undervalued where the corporate debtor–

- makes a gift to a person; or

- enters into a transaction with a person which involves the transfer of one or more assets by the corporate debtor for a consideration the value of which is significantly less than the value of the consideration provided by the corporate debtor, and such transaction has not taken place in the ordinary course of business of the corporate debtor.

3. Extortionate credit transactions: As per Section 50 of IBC, where corporate debtor has been a party to an extortionate credit transaction involving the receipt of financial or operational debt during the period within two years preceding the insolvency commencement date.

Authority to make an application in case of Undervalued Transaction

You must log in to read the rest of this article. Please log in or register as a subscriberRead more