IDFC and Shriram Group have agreed to merge to create a financial conglomerate and offer various types of retail and corporate loans. The companies will finalise the deal within 90 days (from mid-July 2017). If the deal finally happens and gets all regulatory clearances, then it can create a financial conglomerate that could become the country’s largest mass retail platform to deliver full range of financial products.

All the operating businesses of the two groups will come together under IDFC Ltd. While the contours of the deal are not yet known, it seems the retail consumer centric business of the holding company Shriram Capital – Shriram City Union Finance (SCUF) – will be merged with IDFC Bank. The transport finance business will remain a standalone non-banking finance company that would become a subsidiary of IDFC Ltd. If the deal goes through, Rajiv Lal promoted IDFC Bank will be the clear winner because of cross-selling benefits from Shriram Transport Finance Company (SHTF), which is a dominant pre-owned commercial vehicle financing player.

Strategically, the proposed merger is in the right direction because of the fact that IDFC Bank is struggling with execution and growth and Shriram Group has structural growth concerns. However, there will be challenges related to execution, regulatory approvals, capital allocations and holding company discount.

About the two companies

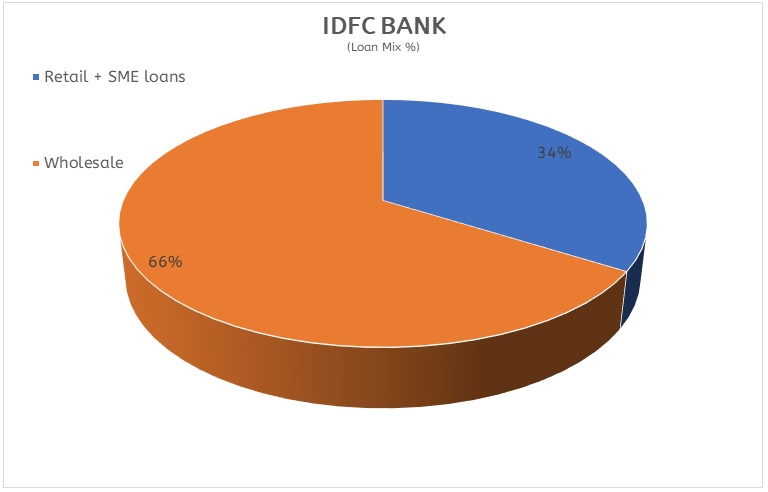

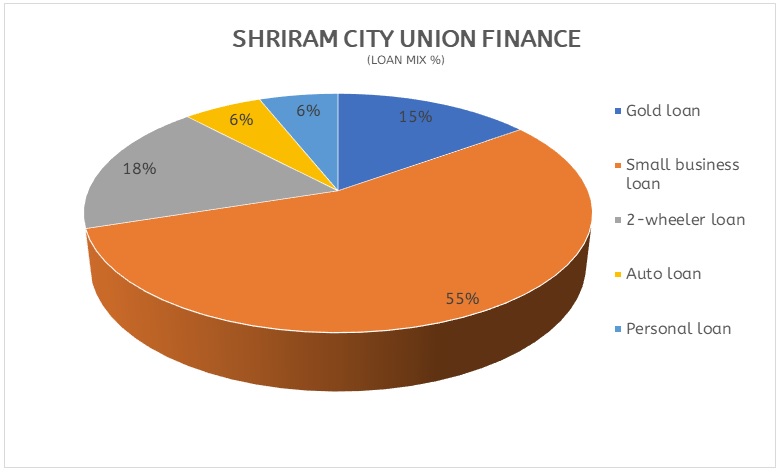

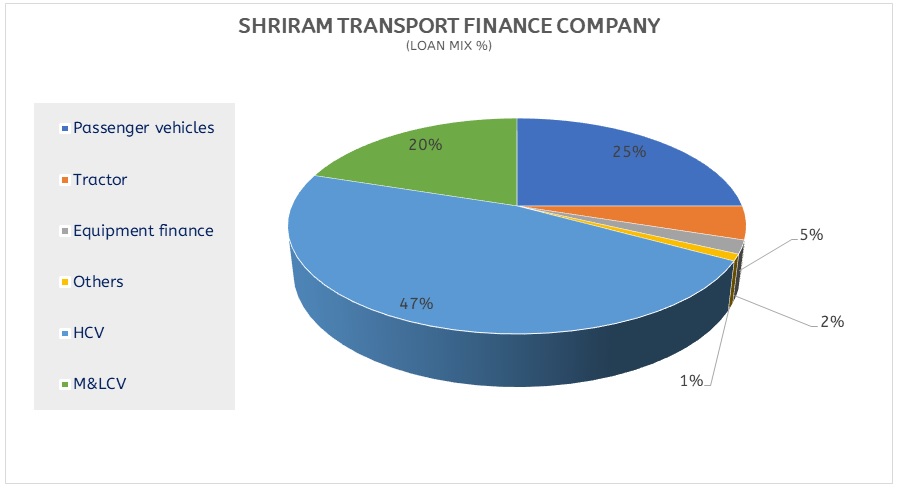

Shriram Group is backed by Piramal Group as Ajay Piramal has majority shares. Before becoming a bank in 2015, IDFC was into domestic infrastructure lending. Shriram Transport Finance Company (SHTF) has over Rs 40,000 crore in assets under management and is the country’s largest financer of commercial vehicles. Shriram City Union Finance offers home, auto and personal loans and both these companies are held by Shriram Capital, headed by Ajay Piramal as Chairman since 2015. He owns 20% in Shriram Capital and 10% each in both Shriram Transport and the Shriram City Union. Shriram Group has a loan book of over Rs 80,000 crore and IDFC and its banking arm IDFC Bank together have a loan book of Rs 60,000 crore.

IDFC owns around 53% stake in IDFC Bank launched in October 2015. The total assets of the two companies would be around $9 trillion. As IDFC already has a banking license, the likely merged entity will be called IDFC and not Shriram. The complex structure of the companies will require approval from Reserve Bank of India, Insurance Regulatory and Development Authority of India, Securities and Exchange Board of India and Competition Commission of India. The proposed merger may not be a catwalk as RBI may not allow a corporate entity into banking and has norms of capping promoters’ stake under 10%. After the merger proposal is cleared by the shareholders of both the companies, they will approach the regulators for approvals, which can take about a year and then the integration time.

Valuations

An analysis based on FY17 numbers indicate that the combined entity will have a loan book of Rs 1.5 lakh crore, profit-after-tax of Rs 2,800 crore and return on equity (ROE) of 9%. If the merger swap is based on current prices and assuming that IDFC Bank will be the combined company, it will lead to 25% dilution in IDFC Bank’s book value. However, given the higher ROEs for SHTF and SCUF, the deal is expected to be 15% earnings accretive.

If the merger takes place, IDFC Bank shareholders are likely to see their stock’s value rise. As the swap ratio has not been made public, it is too difficult to analyse how much Shriram Group companies shareholders will benefit. However, for IDFC Bank’s shareholders, it can be a positive outcome because the bank needs diversification to grow. To be sure, the merger will provide IDFC Bank a deeper retail presence and the Shriram Group low cost funds from the wholesale banking of IDFC Bank.

The deal would require a very favourable swap ratio for Shriram group investors. While the merged entity – IDFC Bank and Shriram City Union Finance – will see the bank’s asset size increase, neither of the companies have a liability book to match that. At present, mobilizing deposits for IDFC is a challenge. In fact, the stock prices of both IDFC and its bank have hardly seen an impressive breakthrough and trade at a discount to sector peers.

Given the market dynamics and the challenges of bringing a finance company in tune with banking laws, it will be better to keep Shriram Transport Finance Company untouched as the company has a niche in business of truck financing (around 25% of the market share), especially in the used category. With assets under management of over Rs 80,000 crore with Shriram Transport Finance Company, it will be indeed a big challenge for IDFC Bank to manage such a big company.

Deal impact on the companies

IDFC Bank: The merger will be beneficial for IDFC Bank as it will gain scale because of retail asset franchise and the ability to leverage on SCUF’s customer base. The merger will give IDFC Bank access to 2000 touch points and 10 million plus customers of the two Shriram group NBFCs, which will help it to generate retail deposits and fee income. The structure will enable IDFC to bring down its holding in IDFC Bank to around 40% without any significant dilution requirement and regulatory liquidity requirement will be managed because of excess reserve ratios at the bank. Post-merger, IDFC Bank will have 0.9% market share in loans. Execution challenges, technology integration and HR challenges would be some of the key risks.

Shriram City Union Finance (SCUF): The biggest benefit for SCUF will be access to low cost deposits. In the near to medium term, organic growth would have remain healthy for the company and the liability side would not be a concern. The impact will depend on the swap ratio. The shareholders of SCUF will now get a banking franchise, which is more beneficial in the long-run.

Shriram Transport Finance Company (SHTF): Post-merger, SHTF shareholders will be given shares of IDFC Ltd. The swap ratio will have to adequately compensated for it becoming an unlisted entity and shareholders indirectly getting mix of businesses as compared to pure-play niche commercial vehicle financing company. A key thing to watch out for is whether shareholders looking to own a moat commercial vehicle financing business would like to hold shares of a holding company with stakes in diverse NBFC, banking, asset management, insurance business.

IDFC Ltd: The company will become a holdco for all businesses. Apart from the existing asset management company, private equity, securities business and stake in the bank, the key attractions will be the insurance business and the transport finance business. It will have a consortium of businesses, creating several layers that will entail holding company discount and capital allocation challenges. Moveover, it aims at running two parallel lending franchises which not only will have regulatory challenges but also management issues and huge dilution needs.

Key challenges

The merger of IDFC Bank, which is a more urban-centric wholesale business, with SHTF and SCUF, which are more of rural play, looks like a merger with negligible business overlap. The foremost challenge will be top management bandwidth and the ability to manage such diverse business, especially under IDFC Bank which has just started its operations in 2015 and is seeing a big transition from wholesale-funded project financier to a universal bank.

Secondly, in the near term, SHTF and SCUF’s portfolio will be able to meet IDFC Bank’s priority sector lending obligation. However, the proposed merger will also imply higher SLR and CRR for both SHTF and SCUF portfolio. As the merged company will have high yielding portfolio, the future growth can be built around low-risk transaction-oriented business till the time liability franchise scales up.

Regulatory challenges will be one of the biggest challenges for the deal. One regulatory challenge would be housing an NBFC and a bank under the same Non-Operative Financial Holding Company (NOFHC) (IDFC Ltd) since RBI does not allow an NOFHC to have separate entities where the same business can be done across departments. Other challenges include integration-related issues, especially technology and workforce related. Ensuring the best interest of minority shareholders of SHTF which will be delisted will have to be kept in mind. Given the facts of the company, the merger looks structurally sound, but uncertainty prevails.