The latest failed acquisition of Hershey Co. has renewed the chocolate maker’s reputation as a company that can’t be bought.

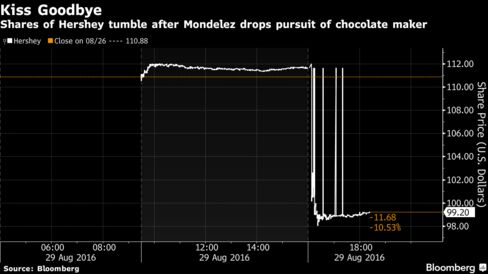

After Mondelez International Inc. abandoned merger discussions on Monday, Hershey shares suffered their worst decline in almost 14 years and left investors with a familiar taste. For years, Hershey has been the subject of takeover speculation. And for years, deal talks have sputtered and died.

The most recent rejection came after Mondelez proposed sweetening its offer to $115 a share, according to a person familiar with the situation. That was 18 percent higher than the stock’s price before deal talks were disclosed in June, but Hershey wanted to start the discussions at $125, said the person, who asked not to be identified because the negotiations were private. Turmoil at the Hershey Trust, the nonprofit organization that controls the company, also hampered merger talks.

“We do not believe another bidder is likely to emerge for Hershey,” Chris Growe, an analyst at Stifel Financial Corp., said in a report. “We believe Mondelez’s challenge in pursuing Hershey will likely dissuade other buyers from attempting a transaction.”

No Path Forward

Mondelez’s initial $107-a-share offer in cash and stock would have valued Hershey at about $23 billion. Hershey’s board said on June 30 that it unanimously rejected that bid. Talks continued, but Mondelez said on Monday that it saw “no actionable path forward toward an agreement.”

The announcement sent Hershey shares down as low as $98.75 in New York, a 12 percent plunge that erased much of their recent rally. The stock had climbed 25 percent this year through Monday’s close, with most of that gain coming when news of Mondelez’s approach became public.

Ending the pursuit of Hershey brought some relief to Mondelez investors, who may have been concerned about a takeover battle. Shares of the Deerfield, Illinois-based company rose as much as 4.8 percent to $44.09 in New York.

Mondelez Chief Executive Officer Irene Rosenfeld, who saw the deal as a chance to create the world’s largest candy company, lamented that the two sides couldn’t reach an agreement.

“Combining our two iconic American companies would create an industry leader with global scale in snacking and confectionery,” she said in Monday’s statement. “While we are disappointed in this outcome, we remain disciplined in our approach to creating value, including through acquisitions.”

Good Fit?

The merger would have given Mondelez a bigger share of the domestic market — a weak spot for the maker of Oreos and Triscuits. Hershey generated almost 90 percent of its revenue in North America last year, with the majority of that coming from selling chocolate in the U.S. Mondelez, meanwhile, has suffered from currency fluctuations and slowing overseas economies.

“The strategic fit with Mondelez was pretty compelling,” Bloomberg Intelligence analyst Ken Shea said. “Not a lot of other companies can do that kind of combination.”

Hershey owns the Cadbury license in the U.S., while Mondelez sells the candy in the rest of the world. Unifying that brand was considered part of the rationale for the merger.

But when Hershey snubbed the $107-a-share bid in June, it said that the offer “provided no basis for further discussion between Mondelez and the company.” Though Mondelez was willing to raise the price by $8 a share, Hershey demanded at least $125, said the person with knowledge of the matter. The Wall Street Journal previously reported on the negotiations.

Trust Upheaval

Then there’s the Hershey Trust. The $12 billion charity organization is in flux, with many of its directors headed for the exits. Hershey didn’t want to even consider a transaction with Mondelez until the charity’s board is reconstituted next year, another person familiar with the situation said.

Earlier Attempts

The trust has scuttled takeovers in the past. Nestle and Wm. Wrigley Jr. Co. both made offers to buy the company in 2002 before being rebuffed. The trust also has stood between Hershey and a deal with Cadbury, which was ultimately acquired by Kraft Foods.

Another wrinkle: The Pennsylvania attorney general has the right to review a deal to acquire Hershey. That’s because the trust is legally obligated to continue financing the Milton Hershey School. Because the organization is supported by profits from the chocolate company, the state can try to stop a sale if it determines that school funding is threatened.

To entice Hershey and its stakeholders, Mondelez offered some unusual concessions with its bid. The suitor pledged to keep the combined company in Hershey, Pennsylvania and retain the Hershey name, according to the Journal. With the trust’s recent upheaval, Mondelez may have felt like it picked the right time to pounce. It wasn’t.

Mondelez “misread the situation,” Pablo Zuanic, an analyst at Susquehanna International Group, said in a report. “In hindsight to us, it looks poorly planned.”

Recent Articles on M&A

Source: Bloomberg.com