After completing its internal restructuring, Akzo Nobel India Limited (“Akzo Nobel”) announced a complete exit from the decorative paint business. In recent years, India’s paint industry has witnessed significant transformation. Once dominated by a few key players, the sector has seen new entrants such as the JSW Group and the Aditya Birla Group, each aiming to become the market leader. The acquisition of Akzo Nobel was seen as a strategic opportunity for these new players to gain a substantial foothold. Ultimately, the race was won by JSW Paints Limited, a company of the JSW Group, marking a pivotal move in its growth ambitions

JSW Paints Limited (“JSW Paints”) is a part of JSW Group. JSW launched JSW Paints in 2019, which is today one of India’s fastest-growing paint companies, with a diverse portfolio of decorative paints and industrial coatings. With a long-standing history of product and process innovation, consumer-resonant brand marketing, state-of-the-art manufacturing facilities and an expanding, pan-India distribution network, the company aims to revolutionise the Indian paints industry. The equity shares of the company are not listed on any bourses.

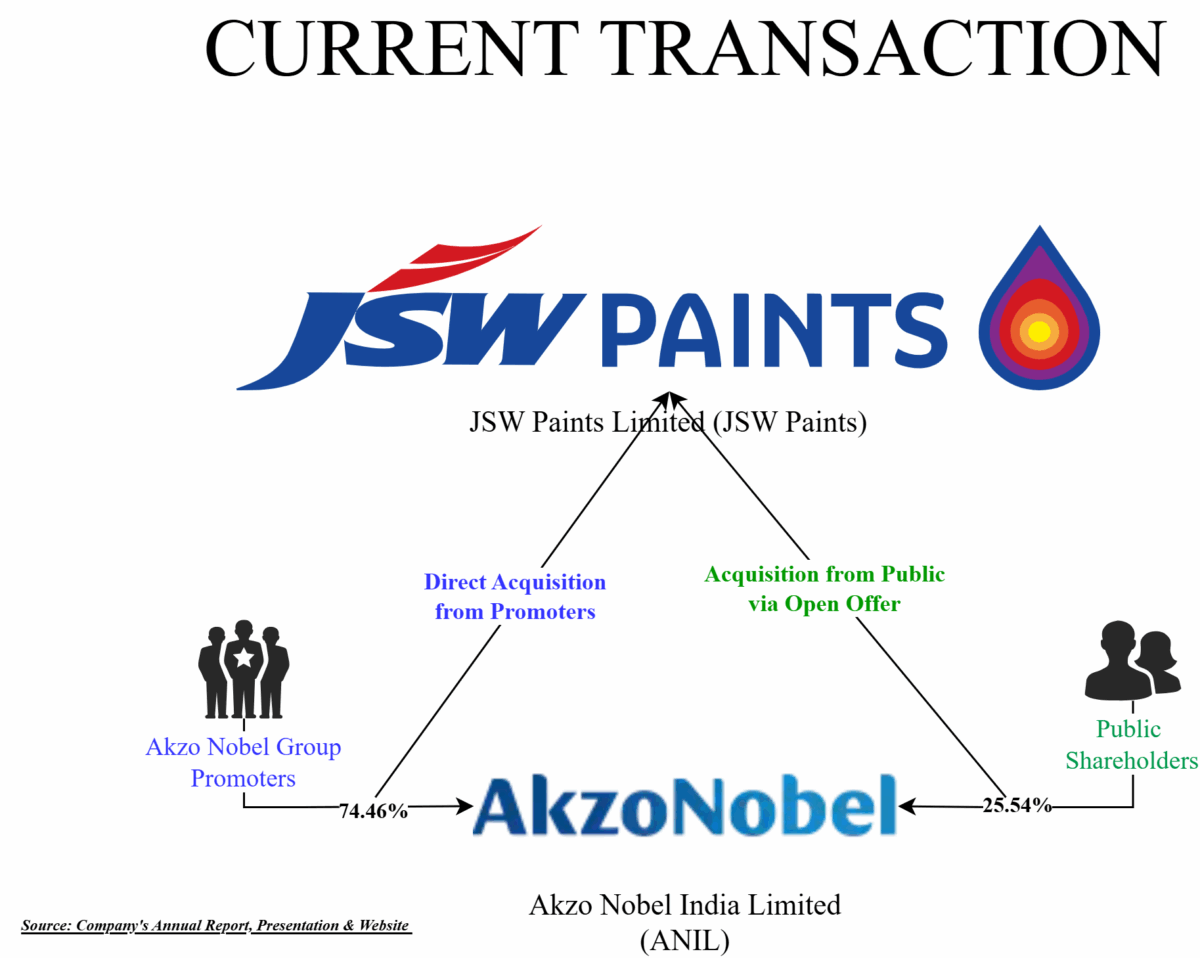

Akzo Nobel India Limited (“Akzo Nobel” or “ANIL”) is an Indian arm of a multi-national company engaged in the manufacturing of a wide range of paint products (Decorative and Coatings) through iconic global brands, including Dulux, International, Sikkens and Interpon. Akzo Nobel N.V. is the main international holding company of the Akzo Nobel Group. Currently, promoters control 74.46% equity stake of ANIL. The equity shares of ANIL are listed on nationwide bourses.

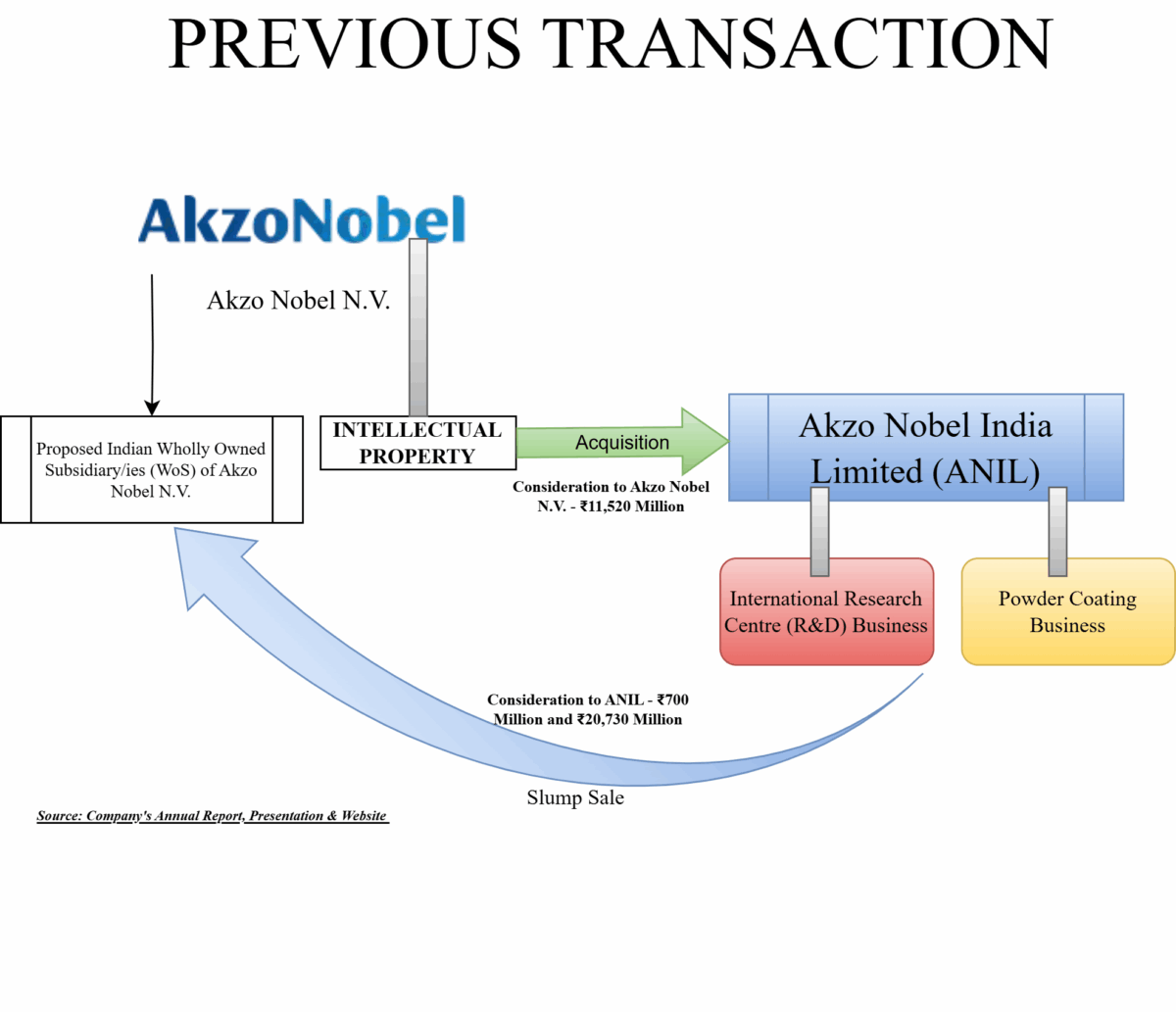

Foreign promoters decided to have only a decorative paint business in ANIL. To achieve the same, ANIL approved the following transactions to make ready for sale:

- Slump sale of “Powder Coating Business” for 20730 million to a proposed to be incorporated Indian wholly owned subsidiary of Akzo Nobel N.V through a Business Transfer Agreement and

- Slump Sale of the “International Research Centre (R&D) Business” for 700 million to a proposed to be incorporated Indian wholly owned subsidiary of Akzo Nobel N.V through a Business Transfer Agreement and

- Acquisition of the intellectual property for 11520 million pertaining to the decorative paints business of ANIL from the ultimate holding company.

We have covered this transaction in detail in our March 2025 issue.

The Proposed Transaction

JSW Paints Limited entered into a share purchase agreement with the promoters of Akzo Nobel, i.e. Akzo Nobel Group, to acquire the entire controlling stake, i.e. 74.76% of Akzo Nobel.

The total consideration for acquiring a 74.46% stake in Akzo Nobel India Limited will be up to ₹9,403.21 crore. This amount includes a contingent consideration of ₹447 crore and certain other adjustments as specified in the Share Purchase Agreement. Following the acquisition of the controlling stake, JSW Paints will also make an open offer to acquire the remaining public shareholding of 25.54%, as the residual stake is less than 26%, in accordance with SEBI regulations.

The difference between the price agreed with the promoters and the open offer price arises due to the pricing guidelines prescribed under the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (“SEBI SAST Regulations”). While the consideration paid to the promoters is a mutually negotiated price between the parties, the open offer price is determined based on the volume-weighted average market price of the shares over the 60 trading days immediately preceding the public announcement, as mandated by the SEBI SAST Regulations.

Rationale for the transaction

The primary motivation behind JSW Paints’ acquisition of Akzo Nobel India is to scale up with well-known and premium brands to secure the fourth position in the rapidly growing and increasingly competitive Indian paint industry. The acquisition will significantly enhance JSW Paints’ presence in urban markets, where it currently has limited play. Moreover, it provides JSW Paints with the scale and brand strength needed to move closer to its ambition of becoming one of the top three players in the sector.

From Akzo Nobel’s perspective, the decision to divest its stake stems from the company’s limited local capabilities and distribution reach, which have constrained its ability to fully capitalize on the market’s growth potential in India.

It is evident that Akzo Nobel India has experienced a lower growth rate compared to the industry leader, Asian Paints. Additionally, its operating margins have remained relatively low, and the company has followed a policy of distributing most of its profits to shareholders, leaving limited room for reinvestment. However, at the same time, its Return on Capital Employed have improved drastically.

In this context, a change in ownership and management could unlock the company’s growth potential and align it more closely with the broader sectoral trajectory. However, maintaining a kind of return on capital employed for going forward, especially for the merged entity, will likely to be a challenge.

JSW Paints will pay a 4.5% royalty on the sales of liquid coatings business to Akzo Nobel Netherlands, while JSW through Akzo Nobel India has intellectual property rights for decorative paints (sold under Dulux brand), it has entered a technological alliance with Akzo Nobel Netherlands for liquid coatings (sold under International and Sikkens brands).

Open Offer

The transaction also triggered a compulsory open offer as per SEBI regulations. Pursuant to the same, JSW Paints announced an open offer for the acquisition of up to 1,14,95,979 fully paid-up equity shares of Akzo Nobel India Limited, representing up to 25.24%* of the Voting Share Capital at a price of ₹3,417.77.

Further, basis the outcome of the open offer, shares to be acquired from promoters would be proportionately reduced so that JSW Paints holding shall not exceed 75% of the total paid-up capital.

Interestingly, JSW Paints Limited is giving the open offer along with JTPM Metal Traders Private Limited (“PAC 1”) and JSW Eduin Fra Private Limited (“PAC 2”, and together with PAC 1, “PACs”), in their capacity as persons acting in concert. Both PAC 1 & PAC 2 are owned by the Jindal family.

The key reason for using PACs could be to have flexibility in raising funds and final debt equity structure in the merged entity and also consider how to remain listed if more shares come under the open offer. The same was done by JSW group during the past acquisition, namely Bhushan Steel.

Shareholding pattern of JSW Paints on diluted basis:

Funding of the transaction & way forward

According to the management of JSW Paints Limited, the acquisition will be funded through a balanced mix of internal accruals and support from financial creditors, including private equity investors. The contribution from each source is expected to be approximately equal. However, there is currently no clarity on whether the funding structure will be adjusted based on the outcome of the open offer.

The management has also indicated the possibility of a reverse merger, wherein JSW Paints could be merged into Akzo Nobel India. This potential move would not only facilitate an indirect public listing for JSW Paints but also provide an exit route for private equity investors participating in the transaction. Beyond operational synergies, the reverse listing represents a significant opportunity for JSW Paints arising from the acquisition

Valuation & Competitive landscape

Financials of JSW Paints & Akzo Nobel

Please note that the Powder Coatings Business & the International Research Centre (R&D) Business contributed ~11% & 1.36% respectively of the total income of Akzo Nobel in FY 2023-24 which is now stands transferred. Further, both businesses constituted ~11 % & 0.48 % of the net worth of the Company as per the audited balance sheet of the FY 2023-24. Further, there will be additional savings on account of royalty which was INR ~140 crore in FY 2025.

Clearly, Akzo Nobel has demonstrated a far stronger performance track record compared to JSW Paints, which is still in the process of establishing its market presence. Another reason for superior margins and returns is Akzo Nobel is having premium products and a significant presence in tier 1 cities vis-à-vis JSW Paints being mass player in tier 2 & 3 cities. JSW Paints revenue has been hovering in the range of INR 2000 crore for the last 3 years. For JSW, acquiring Akzo Nobel is not just strategic—it is essential to scale operations, gain a ready customer base, and drive a turnaround in its paints business.

Interestingly, Akzo Nobel India is also expected to receive significant cash inflows from recent internal transactions with its parent group. These surplus funds can be effectively deployed by JSW Paints to repay the borrowings raised to fund the acquisition. This not only strengthens the financial position of the combined entity but also supports a cleaner path to an eventual merger.

Given the expected loan repayments and likely exit of private equity investors onboarded by JSW, a full-scale merger between Akzo Nobel and JSW Paints seems imminent.

Conclusion

The proposed acquisition opens multiple strategic doors for JSW Paints. With strong backing from the JSW Group—known for executing well-structured acquisitions through a mix of debt and equity—this deal could replicate past success stories. For Akzo Nobel’s promoters, the acquisition offers a timely exit and sale to strategic and strong buyer who will be able to scale the business in a challenging environment. Let us know how much it is value accretive for the minority shareholders in the long run.