In a major consolidation move in the Indian pharmaceutical sector, Torrent Pharmaceuticals Limited (“Torrent” or “Acquirer”) has announced the acquisition of a 46.39% controlling stake in J.B. Chemicals and Pharmaceuticals Limited (“JB” or “Target”) from global investment firm KKR, followed by a proposed merger of JB into Torrent. This strategic transaction marks one of the largest domestic pharma deals in recent years.

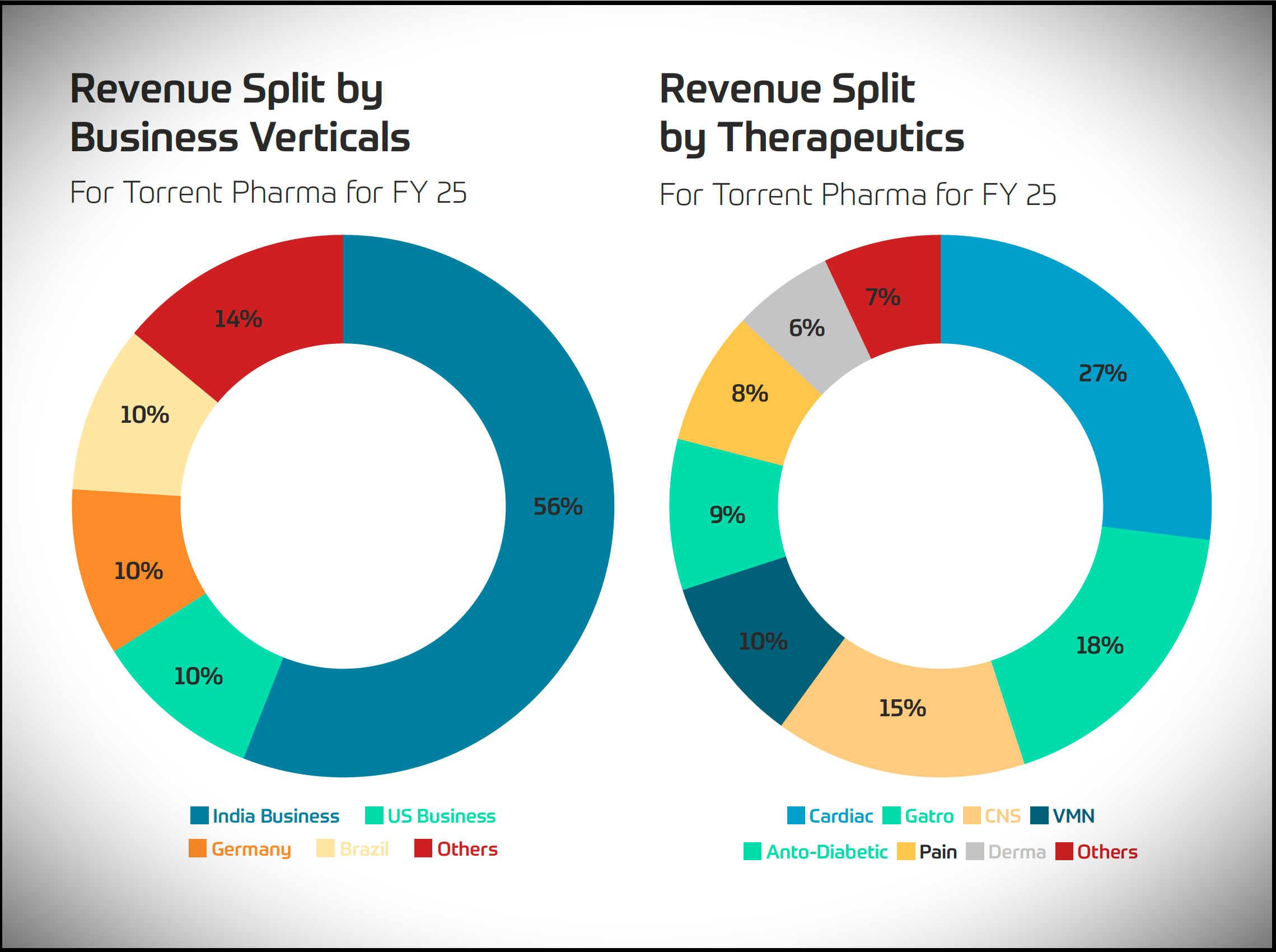

Torrent Pharmaceutical Limited (“Torrent” or “Acquirer”) is the flagship Company of the Torrent Group. It is amongst the Top 5 in the therapeutics segments of Cardiovascular (CV), Gastrointestinal (GI), Central Nervous System (CNS) and Cosmo-Dermatology. The equity shares of Torrent are listed on nationwide bourses.

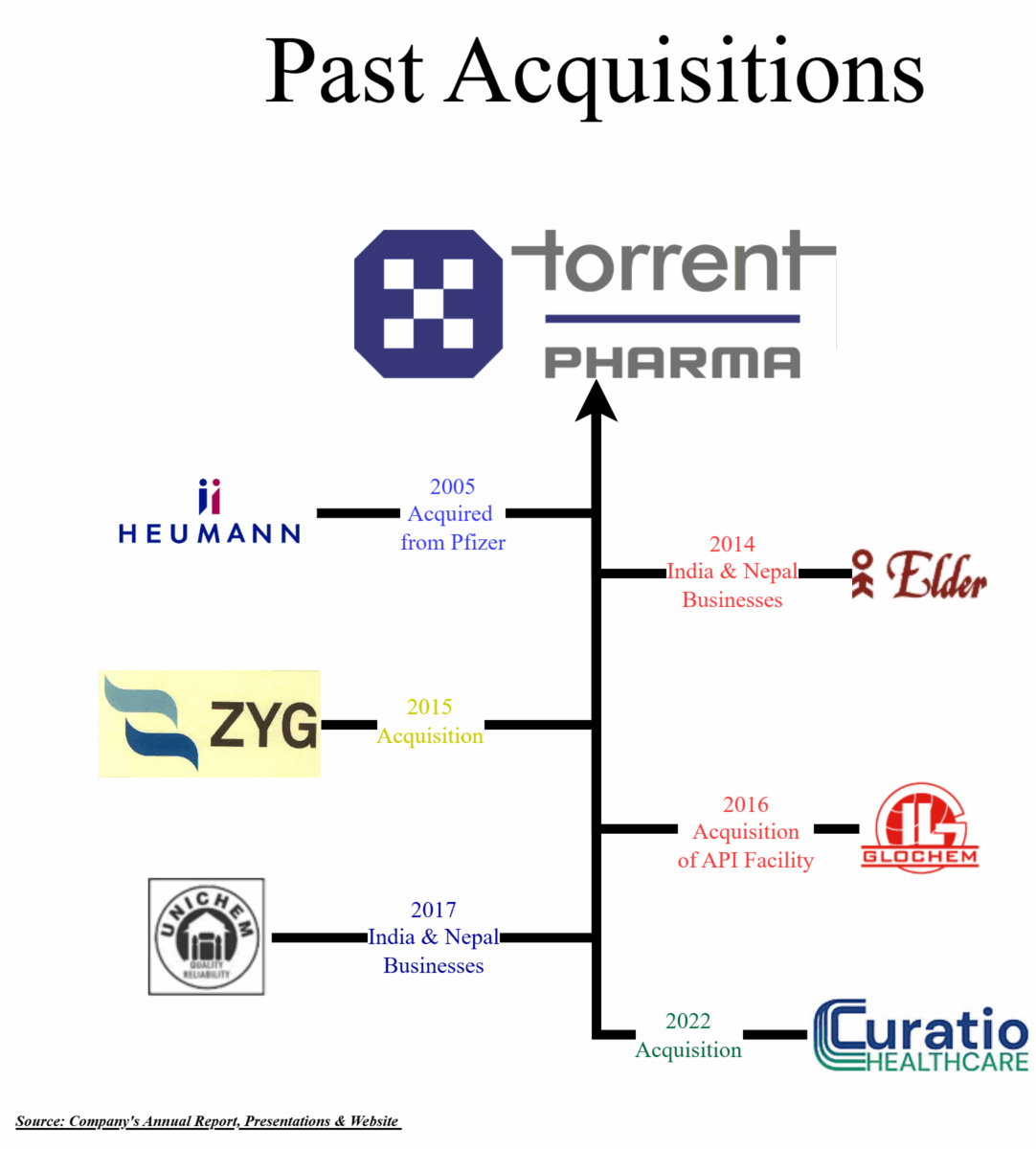

In the past, Torrent has grown significantly through the acquisition route. The Company has a history of successful acquisitions and its integration with existing business operations. Some of the acquisitions by Torrent are shown in this figure.

With its strong own business backed by successful acquisitions, Torrent has grown from INR 4172 crore revenue in 2014 to INR 11516 crore revenue in 2025.

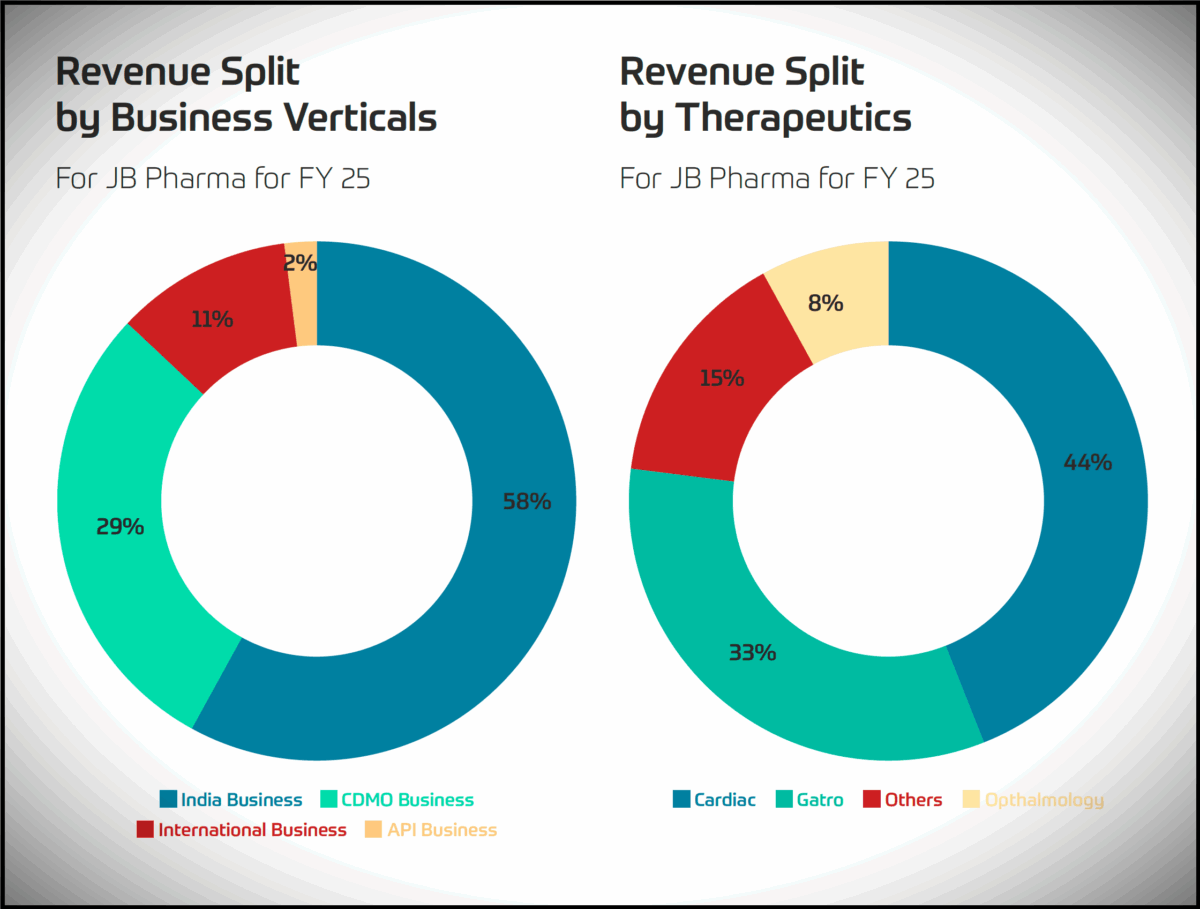

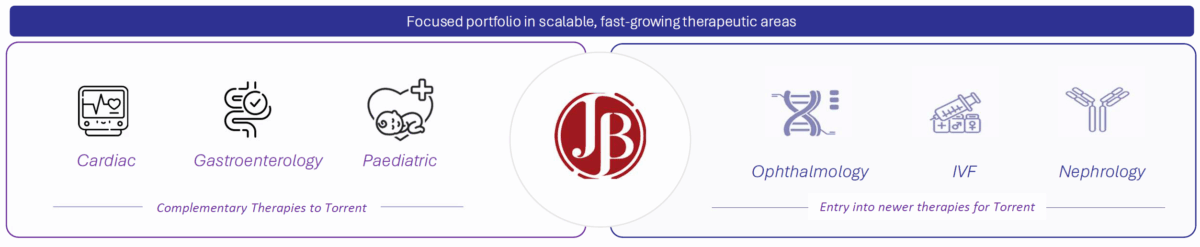

J.B. Chemicals and Pharmaceuticals Limited (“JB” or “Target”) is one of the fastest-growing pharmaceutical companies in India having high-quality products in the cardiac, gastrointestinal, and anti-infective therapeutic areas across the branded formulations. Besides its strong India presence, which accounts for the majority of its revenue, its other two home markets are Russia and South Africa. The company is also a leading CDMO player in the segment of medicated lozenges. The equity shares of JB are also listed on nationwide bourses.

In 2020, the global private equity firm KKR acquired a controlling stake in JB from the erstwhile promoters, Mody family for circa INR 3100 crore. The acquisition was followed by compulsory open offer by KKR, followed by change in management. and KKR took complete control over the company.

The Proposed Transaction

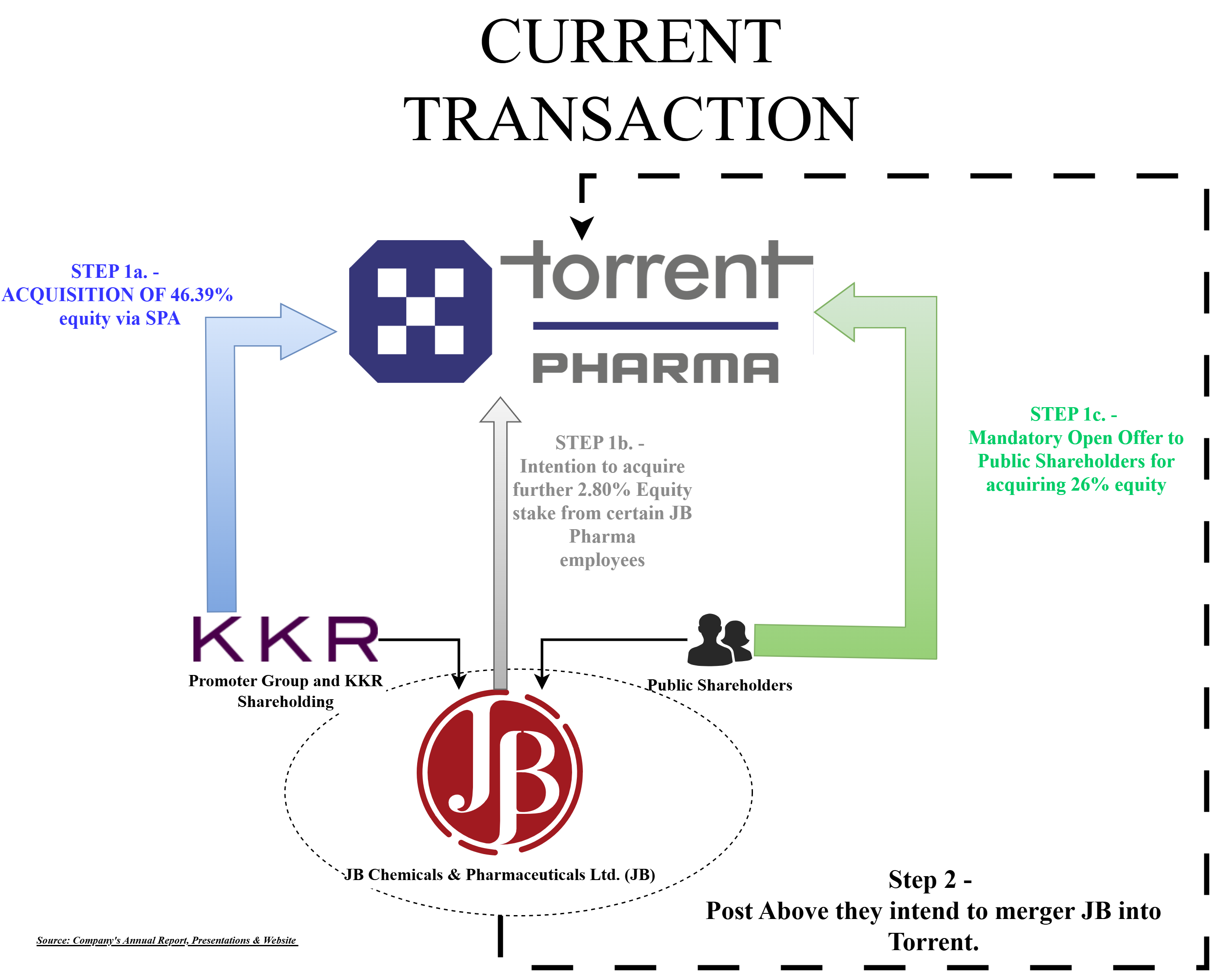

The proposed acquisition of JB by Torrent will be done in two stages.

- Acquisition:

- Acquisition of 46.39% equity stake (on a fully diluted basis) through a Share Purchase Agreement (“SPA”) at a consideration of INR 11,917 crores (INR 1,600 per share)

- Mandatory open offer to acquire up to 26% of JB Pharma shares from public shareholders at an open offer price of INR 1,639.18 per share.

- In addition to the above, Torrent has also expressed its intent to acquire up to 2.80% of equity shares from certain employees of JB Pharma at the same price per share as KKR.

- Merger between Torrent and JB Pharma through a scheme of arrangement.

The completion of the deal is estimated to take 15 to 18 months. The longest approval timeline is the Competition Commission of India approval, expected to take four to five months. Once CCI approval is obtained, the open offer takes approximately one month, followed by the merger process, which typically takes around 12-14 months.

Thus, total Torrent will spend circa ₹19,480 crore to purchase the upto 75.18% (subject to open offer) stake in JB and post that, JB will get merged with Torrent & remaining shareholders of JB will get shares of Torrent. Thus, effectively the proposed acquisition of JB will cost Torrent circa ₹26,000 crore which is almost same as present market cap of JB.

Rationale for the proposed Acquisition & Merger:

- Acquisition provides access to a fast-growing India franchise, with leading brands in the chronic segment, and entry into untapped therapeutic areas like ophthalmology

- Strengthens market share in the IPM for Torrent

- Operational synergies across multiple business functions

- Platform diversification: entry into the CDMO segment with long-term potential

- Consolidation in key international markets and greater ability to scale up

Both JB Chemicals and Torrent Pharmaceuticals have a long-standing presence in India and international markets. JB derives approximately 58% of its revenue from India, with the remaining contribution coming from over 40 countries. Torrent, similarly, generates around 56% of its revenue from the Indian market. The acquisition of JB offers Torrent an opportunity to further consolidate its position in key therapeutic areas such as Cardiovascular (CV) and Gastrointestinal (GI), while opening a new avenue of growth in the CDMO (Contract Development and Manufacturing Organisation) segment, which Torrent finds attractive.

While both entities have complementary portfolio in Cardiac and Gastro, Torrent will be able to diversify into Optho segment and enter the CDMO segment. Further JB presence in Russia and Nigeria will enable Torrent to expand its international market.

JB has 8 plants across 3 locations in Gujarat and has done massive capex of around INR 450 crore after the KKR acquisition to upgrade its facilities. Torrent on the other hand has well-diversified manufacturing facilities across India, including in Gujarat.

Consideration for the Merger:

Post-acquisition of the stake, JB will merge with Torrent. As a consideration for the merger, every shareholder holding 100 shares in JB Pharma shall receive 51 shares of Torrent. The entire shareholding of Torrent in JB will get cancelled.

Please note that, depending upon the pricing of QIP and the success of the open offer, the shareholding pattern will change. The above pattern is just for reference purposes.

| Particulars | Unit | Amount |

| Existing no. of equity shares- Torrent | 338,445,440 | |

| QIP Price of Torrent | per share | 3,214 |

| QIP Amount | Cr | 5000 |

| No. of Shares issued on QIP | 15,554,661 | |

| No. of Shares issued on merger (entire open offer subscribed) | 35,869,053 | |

| Revised no. of equity shares- Torrent (Open offer + QIP) | 374,314,493 | |

| Revised no. of equity shares- Torrent (No Open offer + No QIP) | 380,049,917 |

In the event the open offer is fully subscribed, Torrent intends to raise up to INR 5,000 crore through a Qualified Institutional Placement (QIP) of equity shares. Based on the current market price, this would result in an equity dilution of approximately 4% of the existing paid-up capital. From an equity dilution standpoint, full subscription to the open offer appears to be the more feasible and preferable outcome

Funding the transaction

The acquisition & open offer will be funded through debt & equity by Torrent. For this, Torrent has secured a credit line of upto INR 20,000 crore from a consortium of international bankers. Further, Torrent has also passed an enabling resolution to raise upto INR 5000 crore through Qualified Institutional Placement.

Consolidated position of Torrent as on 31st March 2025:

| Particulars | Amount in Crore |

| Networth | 7591 |

| Borrowings | 3202 |

| Cash & Cash Equivalent | 776 |

Considering the latest financials for Torrent, the acquisition is likely to be funded significantly from debt and equity (to raise money + consideration for a merger). If open offer does not garner any significant response, Torrent may not go for any equity raise.

As per the management, assuming control in Q4 FY26 and merger in FY27-28, the consolidated leverage without open offer would be roughly 1.8x, and at worst, if 26% of the open offer gets subscribed, it would be 2.8x at the end of FY27. Torrent expects to repay the debt within two and a half years. However, considering the above numbers, unless there is super growth & synergies coming out of this transaction, the above figures does not justify the management optimism.

Turnaround by KKR

KKR invested in JB Chemical back in 2020. Post-acquisition, KKR immediately started its plan to improve profitability and increase the penetration of brands owned by JB. Within 5 years, JB made 5 acquisitions to expand itself. Some of the key acquisitions are as follows:

- In FY 2024, the Company entered into a Trademark License Agreement with Novartis Innovative Therapies AG, Switzerland for a portfolio of 10 ophthalmology brands for the Indian market, which will be effective from January 2027 for a consideration of USD 116 million payable on or before December 31, 2026.

- The Company also entered into a promotion and distribution agreement with Novartis Healthcare Private Limited for the same portfolio for a period of three years starting December 2023 for a consideration of ₹ 12,500 lakhs for this exclusive promotion and distribution agreement.

- It has also acquired probiotics and reproductive brands for the Indian market from Sanzyme Private Limited for ₹628 crore.

- The Company acquired the brand Azmarda® indicated for heart failure patients with reduced ejection fraction (HFrEF) from Novartis AG, Switzerland for India

Clearly, through its 5 years of acquisition time, KKR concentrated on building more brands across the portfolio plus concentrated on more penetration of its existing brands.

KKR Gain

KKR invested circa INR 3100 crore to acquire a 54% stake in JB in 2020. In March 2025, KKR sold 5.77% stake in the open market for circa ₹1460 crore translating to ₹1625 per share. The current deal will help them to divest the entire remaining stake for ₹11917 crore.

| Particulars | Amounts in crore |

| Initial amount invested to buy controlling interest in JB | -3,100 |

| Sale of 5.77% stake | 1,460 |

| Sale of remaining shares to Torrent | 11,917 |

| Total gain | 10,277 |

| Returns (x) | 4.3 times |

Financials

In all parameters, Torrent numbers and ratios are better than that of JB. It will be interesting to see how Torrent is able to synergise its operations with JB and derive incremental returns out of it.

Key valuation multiple assigned

| Particulars | JB | Torrent |

| Tentative market cap (₹ Crores) | 26,000 | 115,000 |

| Enterprise Value/EBITDA | 25 | 32 |

| PE Ratio | 39 | 60 |

Conclusion

The proposed transaction marks one of the largest buyouts in the pharma sector. For KKR, the entire 5 years journey is a textbook case of private equity value creation for all stakeholders, followed by a successful exit. Torrent strengthens its product portfolio, geographic reach, and enters new business verticals like ophthalmology and CDMO.

The Competition Commission of India is likely to play the biggest regulatory approval challenge. There is a minor brand overlap in the probiotic segment, but Torrent is hopeful of a positive outcome regarding any potential divestments. The deal has been structured beautifully to take care of the commercial aspects of KKR, JB and Torrent.

There could be several commercial reasons for structuring the transaction in two steps rather than directly announcing a merger. For KKR, this structure facilitates a clean and immediate exit by tendering its stake for cash, instead of receiving Torrent shares and subsequently liquidating them, which will take at least one more year for cash out and there is no clear road for exit. For Torrent, it helps to manage dilution more efficiently, potentially limiting it to half of what would occur in a full merger scenario. However, this approach also necessitates significant cash outflow from Torrent to acquire KKR’s stake and meet the open offer obligations and delay the completion of the integration of both companies.