Technical Ammonium Nitrate (TAN) is an important chemical used in various industries, including mining, construction, and agriculture. Its primary use is as a component in explosives, where it is mixed with other chemicals to create an explosive compound that can be used for mining and construction.

The global TAN market is expected to grow significantly in the coming years due to increased demand from various industries. Factors such as the growing population, increasing construction and mining activities, and rising demand for high-quality fertilizers are expected to drive the demand for TAN.

Recently, Deepak Fertilisers and Petrochemicals Corporation Ltd. announced an internal rejig of its growing Technical Ammonium Nitrate business which shall entails it to house it in a separate wholly-owned subsidiary.

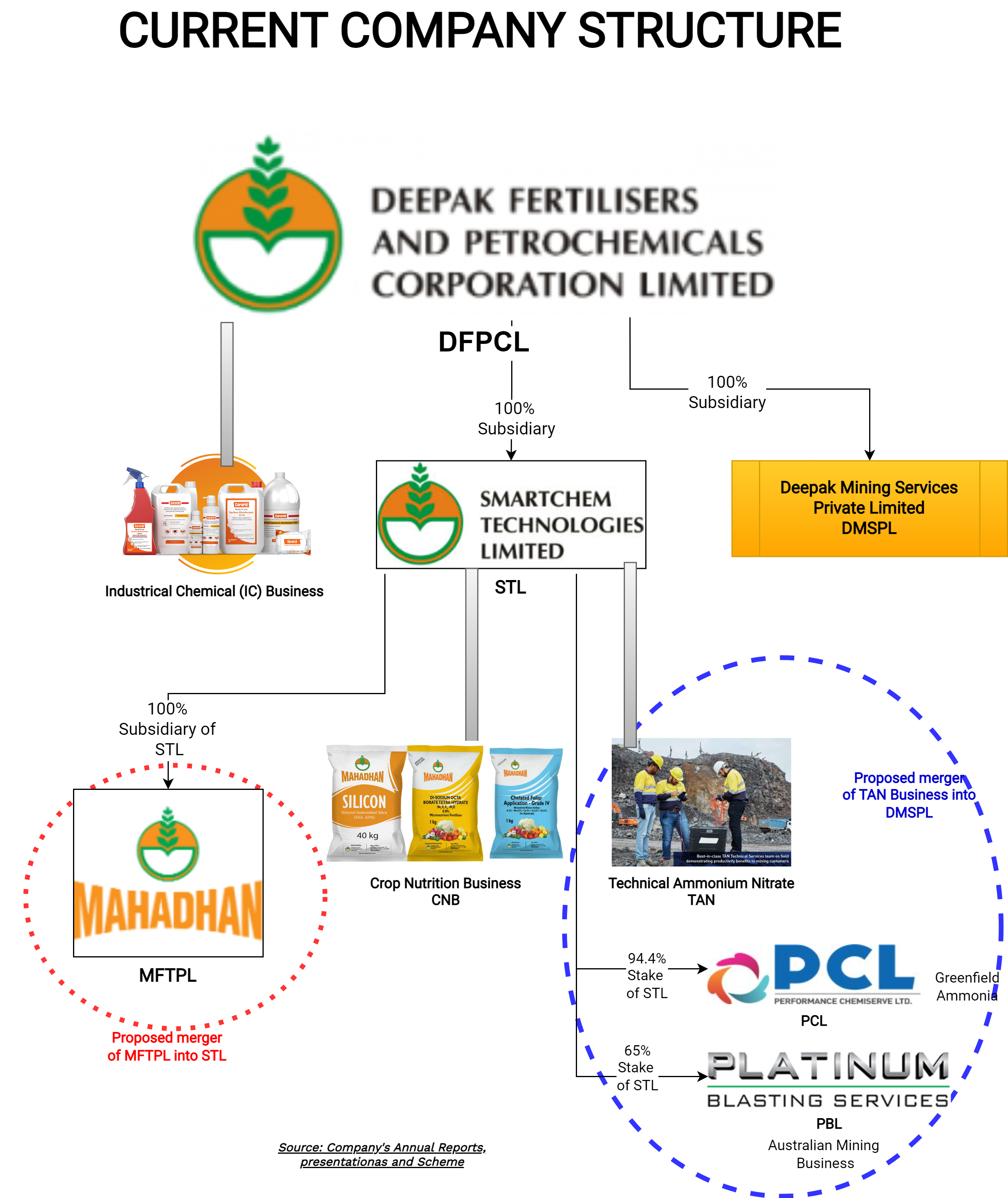

Deepak Fertilisers and Petrochemicals Corporation Ltd. (DFPCL) is among India’s leading manufacturers of industrial chemicals and fertilisers. The company is engaged in manufacturing of following businesses:

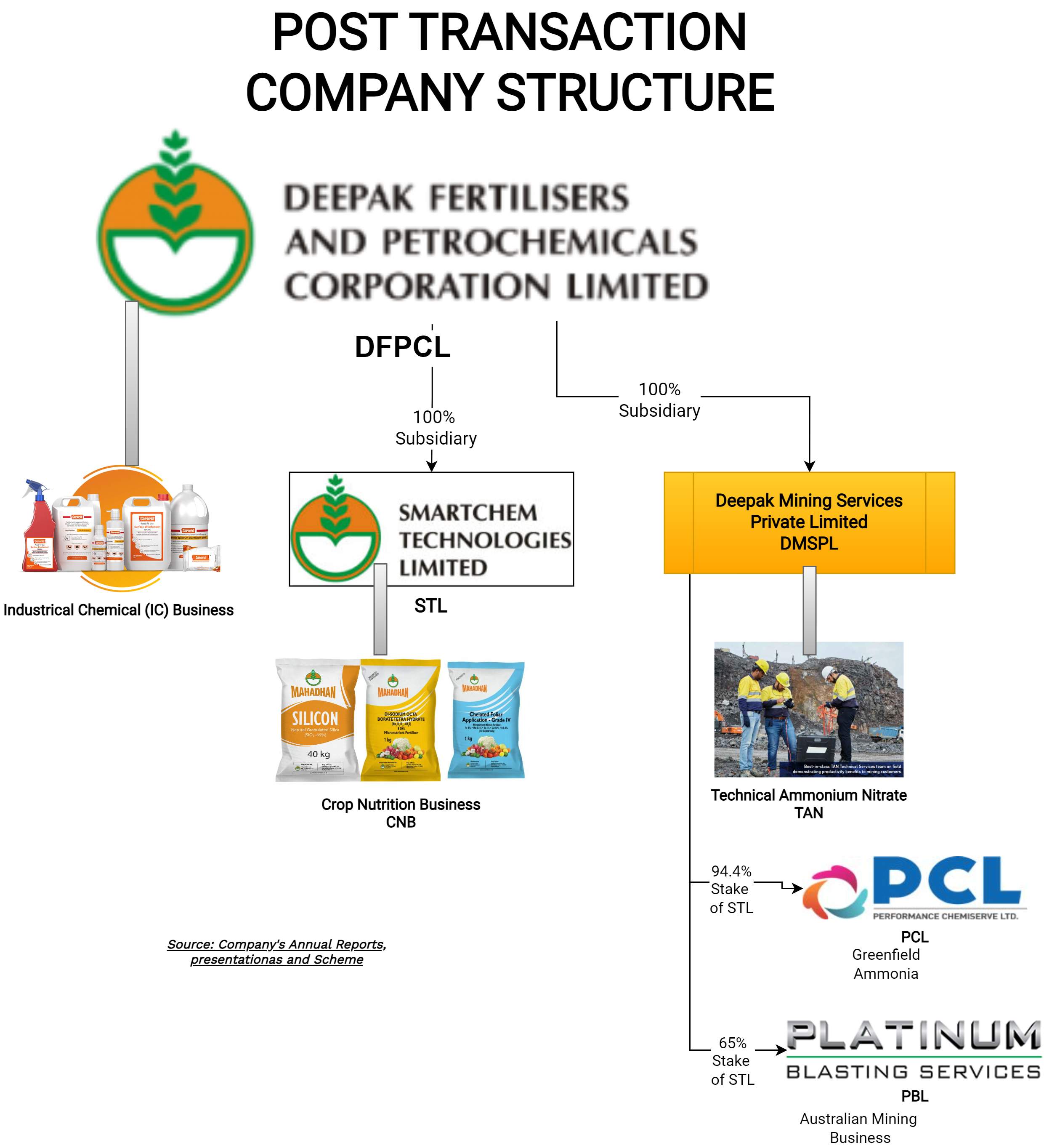

- Industrial Chemicals (IC), through DFPCL

- Technical Ammonium Nitrate (TAN), and Crop Nutrition business (CNB) through wholly owned subsidiary; Smartchem Technologies Limited (“STL” or “Demerged Company”).

The equity shares of DFPCL are listed on nationwide bourses.

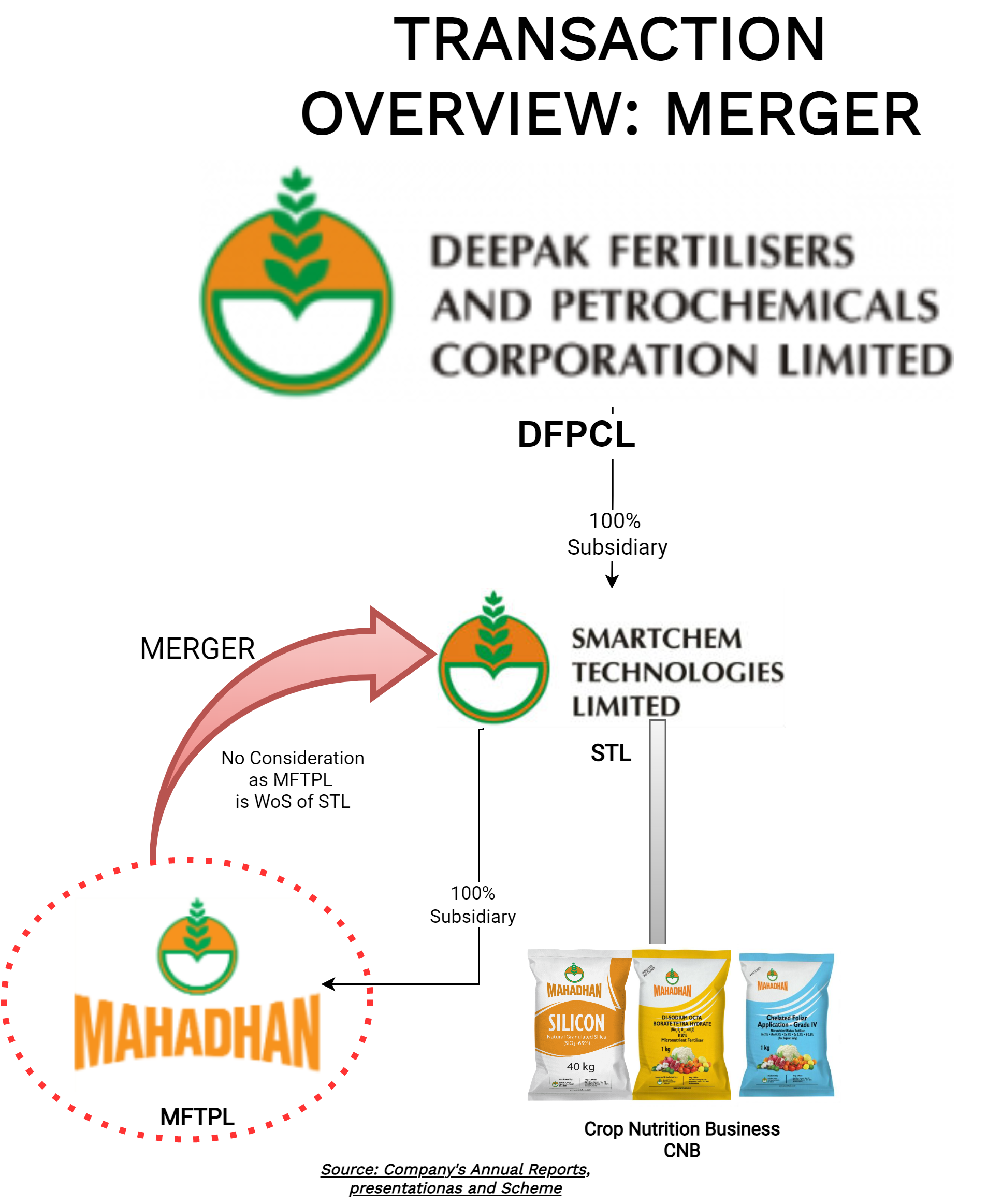

Mahadhan Farm Technologies Private Limited (MFTPL) is engaged in the business of manufacturing water-soluble fertilisers. MFTPL is a wholly owned subsidiary of STL.

Deepak Mining Services Private Limited (DMSPL) was incorporated with the objective of providing consultancy to mining companies in India inter alia to the entire value chain of the mining business. However, currently it has no business activities. DMSPL is a wholly owned subsidiary of Deepak Fertilisers and Petrochemicals Corporation Limited.

Current Structure of the Group:

Past Transaction

In order to enable better realisation of potential of the businesses of DFPCL as well as yield beneficial results and enhanced value creation, on 29th March 2016, the Board of Directors of DFPCL approved the Scheme of Arrangement amongst the Company and its wholly owned subsidiaries: SCM Fertichem Limited and Smartchem Technologies Limited involving:

- Slump Exchange of TAN & Fertiliser business of DFPCL to SCM Fertichem Limited

- Subsequent demerger of TAN & Fertiliser business from SCM Fertichem Limited to Smartchem Technologies Limited

[rml_read_more_subscriber]

Proposed Re-structuring:

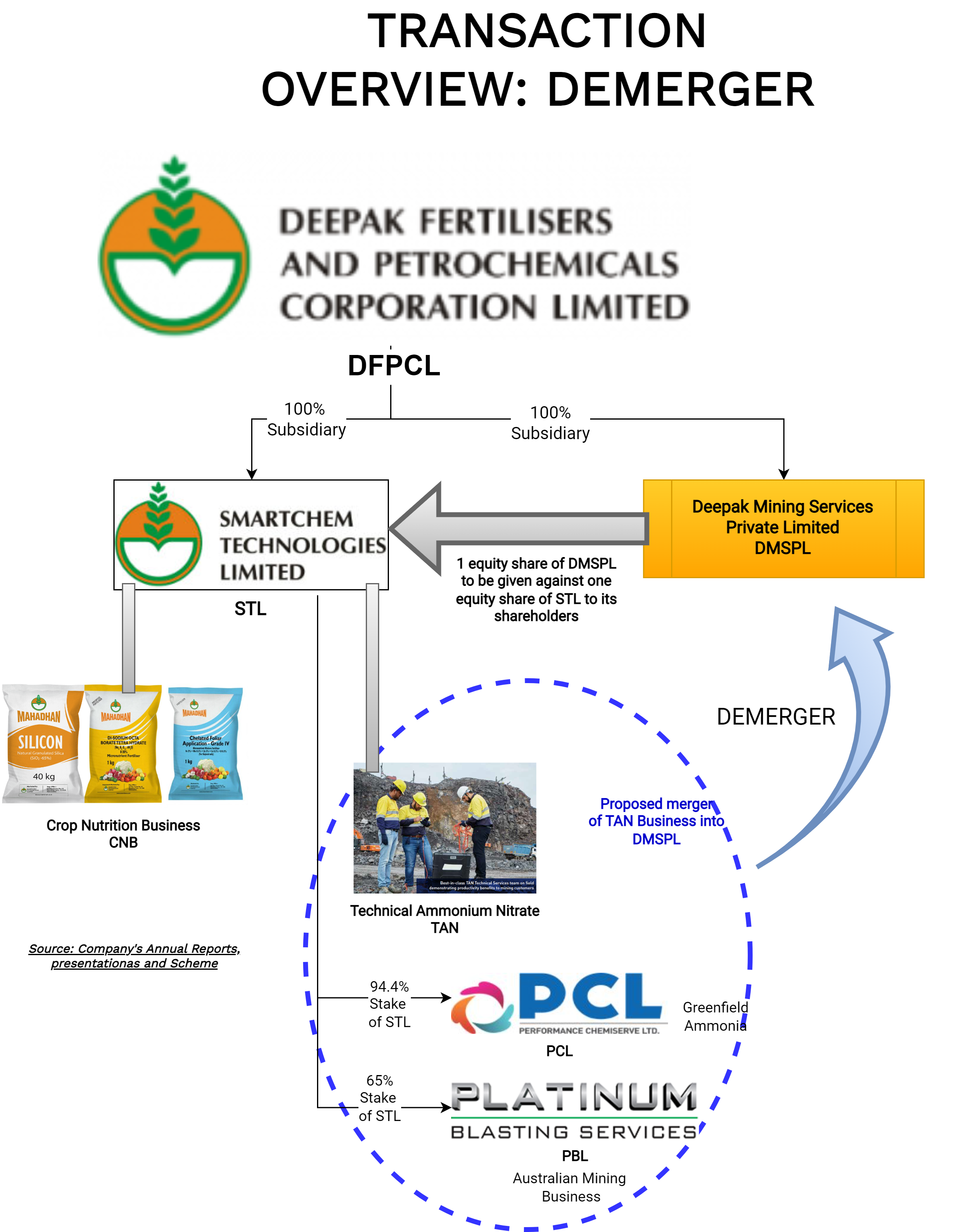

The Board of Directors of DFPCL at their meeting held on 15th December 2022 have accorded its in-principle approval to the Composite Scheme of Arrangement (“Scheme”) between Smartchem Technologies Limited, Deepak Mining Services Private Limited and Mahadhan Farm Technologies Private Limited and their respective shareholders in accordance with the provisions of Sections 230 to 232 read with Section 52 and other applicable provisions of the Companies Act, 2013 and the rules framed thereunder. The Scheme inter-alia provides for:

Demerger of the TAN Business (Mining Chemicals) from Smartchem Technologies Limited to Deepak Mining Services Private Limited

Rationale’s as envisaged by the management:

- The arrangement will result into creating holistic business entities housed in identified corporate entities.

- Focused Leadership: Over the last five years, the focus of both TAN and CNB business has evolved from commodity to specialty, with an increased emphasis on solutions. Both independent entities to have individual growth plans, focused leaderships and strategies to maximise its growth prospects.

- Consumer-focused Orientation Strategy: There is no product, seasonality, markets, branding, or value proposition overlap between CNB and TAN businesses. Consumer-focused orientation strategy likely to get impacted if the CNB and TAN work culture remains intermingled.

- Demerger to Unlock the True Potential: Enable sector-specific strategic and financial investments in respective businesses.

Amalgamation of Mahadhan Farm Technologies Private Limited, being a wholly owned subsidiary of Smartchem Technologies Limited, with Smartchem Technologies Limited

Rationale’s as envisaged by the management:

- Simplification of the corporate structure.

- Economies of Scale: Strengthening customer service, distribution network, overall economies of scale for all the business verticals.

The Appointed Date for the proposed demerger & merger is 1st January 2022.

Transferred TAN undertaking includes greenfield ongoing Ammonia project & Australian Mining Business. The reason as envisaged for transferring Ammonia business with TAN, Ammonia Business has been funded and incubated by TAN business being the largest consumer of Ammonia.

Consideration:

1 (One) fully paid-up equity shares of face value of INR 10 each of DMSPL shall be issued and allotted to the shareholders of STL for every 1 (One) fully paid-up equity shares of face value INR 10 each held in the Demerged Company.

As STL & DMSPL both wholly owned subsidiaries of DFPCL, there will not be any change in shareholding pattern pursuant to the demerger. One of the key reasons for discharge of consideration could be to comply with provisions of the Income Tax Act, 1961.

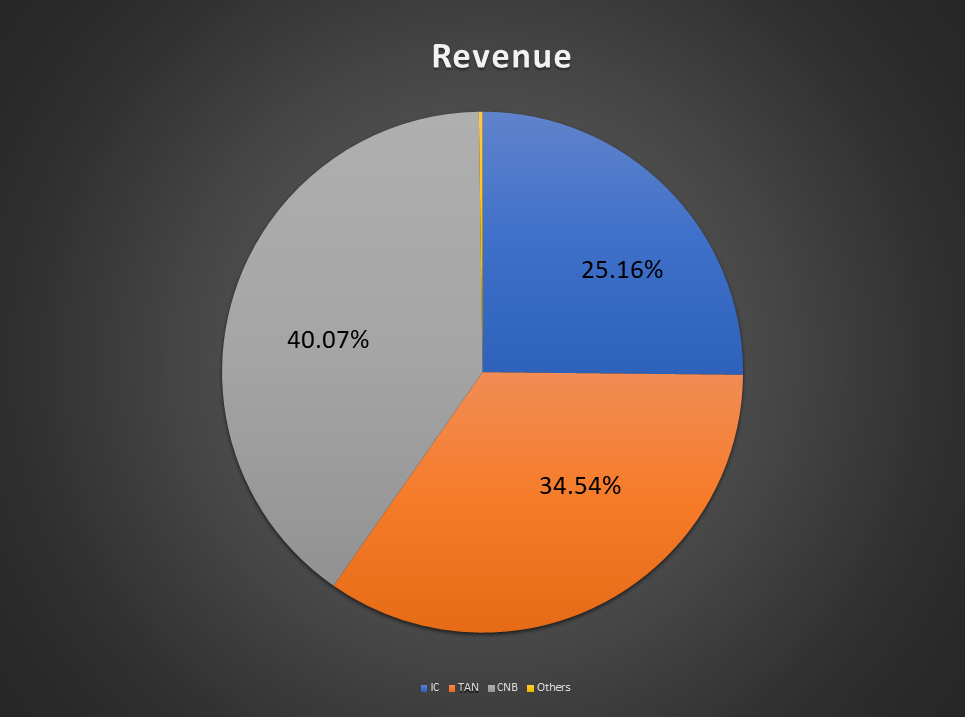

Overview of the current consolidated business of DFPCL:

Based on FY 2022 revenues:

IC business which is being carried by DFCPL amounts for circa 25% of the total revenue while STL (TAN + CNB) accounts for circa 75% of the total revenue.

TAN Business

DFPCL through STL is one among the top producers of TAN in the world & largest producer in India. TAN business accounts for more than 1/3rd of total DFCPL business. Being into value-added products, the margins of TAN are better than other business verticals. The Company secured 44% Market Share in the Domestic TAN market in FY22. The group is also doing forward integration for finished products of TAN (Cartridge and Bulk explosives) required by the Mining and Infrastructure industries.

The Company, to meet the rising demand for TAN, is expanding capacity in its existing Taloja plant and setting up a greenfield TAN manufacturing plant in the Eastern Coast of India. The plant is expected to start production in 2024 and ideally positioned to capitalise on the strong demand growth in the East and adjoining Central regions. Pursuant to this, the capacity will increase by 3,76,000 MTPA from the existing capacity of 4,86,900 MTPA. The total capital outlay for the project is estimated to be Circa INR 2200 crore.

Common Resources

It appears that apart from several fixed assets (including factory premises) some of the business verticals like Ammonia caters to both CNB & TAN. Ammonia business is getting transferred along with TAN. Treatment for other common assets needs to examine.

Investment by International Financial Corporation

In 2019, STL allotted certain Compulsorily Convertible Debentures (CCDs) to International Financial Corporation. In October 2020, it further invested aggregating its investment to INR 210 crore. From the terms of the CCDs, it appears that the conversion ratio will be determined based on the valuation at time of conversion. The proceeds were mainly used for working capital & capital expenditure (significantly relating to Ammonia & TAN) business. It is not clear whether these CCDs will remain in Smartech or Partly/fully transferred as part of the demerger to DMSPL.

Interestingly, despite issue of CCDs to IFS by STL, in press release for the demerger by DFCPL, STL is mentioned as wholly owned subsidiary. Further, press release, as well as NCLT application order dated 25.01.2023, does not provide for any swap ratio for those CCDs.

Financials

Performance of DFCPL in last 5 years:

INR in Crore

Clearly, on account of bulk-to-specialised chemicals & over increase in prices, DFCPL's overall performance improved significantly.

The performance of Chemical division of STL (mainly TAN) is as below:

INR in Crore

Segment-wise performance of STL for FY 2022:

* Please note that the Fertiliser business is a cyclical business.

Conclusion

In 2015, DFCPL restructured its Fertiliser & TAN business to a wholly owned subsidiary through a complex yet interesting structuring. The move was mainly to facilitate growth & inviting a partner if needed. The rationale as mentioned at the time for housing TAN & SNB division into a separate subsidiary was production capacities being interchangeable and TAN can also be potentially used as fertiliser.

Clearly, there is change of strategy for the group as a whole. In yet another restructuring for its TAN business, the intention seems to be either inviting partners and/or evaluating possibilities of separate listing in near future. Appointed Date of 1st January is to achieve separation as on 31st March, 22 considering TAN business performance for Q4 Fy22.