An equity share with differential rights is like an ordinary equity share, but it provides more or fewer voting rights to the shareholder. The difference in voting rights can be achieved by increasing or reducing the degree of voting power. Companies Act, 2013 allows shares with superior and inferior voting rights. For any company planning to get listed on the stock exchanges, SEBI will allow it to continue to have DVR with superior voting rights only to technology driven companies, obviously subject to certain conditions as discussed later in the article.

Issue of DVRs under Companies Act, 2013

Section 43 of the Companies Act, 2013 provides that Equity share capital can be –

- with voting rights or

- with differential voting rights as to dividend, voting or otherwise.

As regards issue of fresh DVR, a company is required to comply with the conditions contained in Rule 4 of the Companies (Share Capital & Debentures) Rules, 2014. Pursuant to the notification dated 5th June 2015, section 43 and conditions given under the rules does not apply to the private company limited by shares in respect of DVR if the memorandum or articles of association of the company provides so.

Conditions contained in Rule 4 of the Companies (Share Capital & Debentures) Rules, 2014 are as follows:

- Issue of DVR must be authorised by the Articles of Association (AOA) of the Company.

- Issue of DVR is authorized by an ordinary resolution at the General Meeting. In the case of companies having more than 200 members, companies are required to pass the resolution through postal ballot. For companies which propose to list their shares on the stock exchange must pass special resolution, the same has been covered in detail in the later part of this article.

- Shares with DVR shall not exceed 26% of the total post-issue paid-up equity share capital including equity shares with differential rights issued at any point of time. There is no bar on the quantum of superior or inferior voting right attached to the equity share which means Company may issue shares with differential voting rights which are having voting rights more than 26 % but total post-issue paid-up equity share capital shall not exceed 26% including shares with DVR issued at any point of time.

- Consistent track record of distributable profits for the last three years

The word “Distributable Profit” is different from the word “Profit”. Companies Act, 2013 does not define distributable profits but sub-section (2) of section 123 of the Companies Act, 2013 states the sources from which company can pay dividend accordingly one can interpret the word Distributable Profit. While Computing distributable profits any amount representing unrealised gains, notional gains or revaluation of assets and any change in carrying the amount of an asset or of liability on measurement of the asset or the liability at fair value shall be excluded. There exist some ambiguity regarding whether company which is in existence for less than 3 years is eligible to issue shares with DVR.

- No default in filing financial statements and annual return for three financial years preceding the financial year in which issue is proposed to be made.

- No default in payment of declared dividend to equity and preference shareholders.

It is important to note that existing ordinary equity shares of the company cannot be converted into equity shares with differential voting rights and vice versa.

Need of DVR for Start-up companies

Raising equity on a periodic basis leads to dilution of founder/ promoter’s stake, which can be effectively addressed through use of DVRs as a mode of capital raising. Companies issue equity share with differential rights for prevention of a hostile takeover and dilution of voting rights. It also helps strategic investors who do not want control but are looking at a reasonably big investment in a company.

Start-up companies usually incur losses in the initial years after its incorporation. Start-up companies which are Private Companies Limited by shares and not fulfilling the conditions given under Rule 4 of the Companies (Share Capital & Debentures) Rules, 2014 can still issue shares with DVRs if the memorandum and articles of association of the company provides so. Start-up companies which are public company limited by shares and proposed to list its shares on the stock exchange will have to comply with provisions under the Companies Act, 2013 along with rules, regulations given by SEBI.

Framework for Issuance of Differential Voting Rights (DVR) Shares by Companies*

In the case of listed company with the apprehension of possible misuse of Differential Voting Rights (shares with superior voting rights), SEBI had prohibited the issue of such shares on July 21, 2009. However, shares with inferior voting rights were permitted by SEBI.

Despite the benefits of the DVRs, very few companies have issued DVR shares having inferior voting rights reasons being low Market Price as compared to the ordinary shares, unattractive dividends, discomfort with losing voting powers.

SEBI in its meeting dated 27th June 2019 has approved a framework for issuance of differential voting rights shares along with amendments to the relevant SEBI Regulations whereby it has allowed issuance of DVR only if they will be offerings of Superior Voting Rights to the Allottees.

Only technology driven (as per the definition in Innovators Growth Platform) companies are allowed by SEBI to list their Ordinary Shares in the form of IPO on the Main Board, though the company has already issued Superior Voting Rights Shares (SR Shares). However, while allowing the said listing of the Ordinary Shares, it has put the following restrictions:

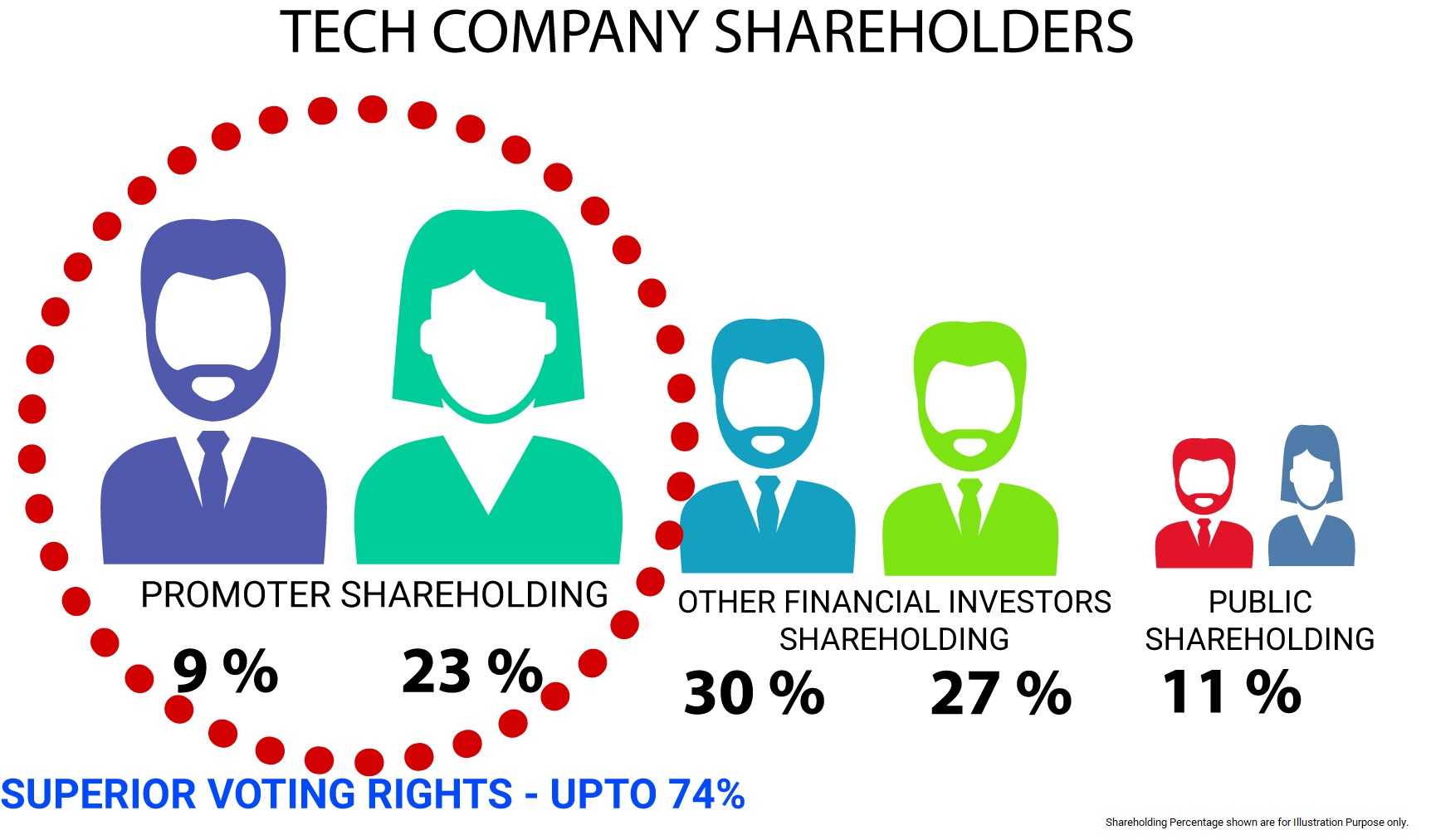

- A shareholder having shares with Superior Voting Rights (SR Shares) needs to be part of Promoter Group holding an executive position in the company and having a minimum combined net worth of Rs. 500 crores.

- The issue of SR Shares will only to the promoters /founders of the company by passing special resolution in the general meeting of the company.

- The promoters /founders must have held these shares for minimum 6 months prior to the filing of Red Herring Prospectus

- The SR shares will have voting rights in the ratio of minimum 2:1 to maximum 10:1 compared to ordinary shares.

- After the IPO, the SR Shares will be required to list on the Stock Exchange, but they will remain under Lock in till they get converted into Ordinary shares. Even, the SR Shares can neither be transferred amongst promoters nor its pledge/lien will be allowed.

- The SR Shareholders will have only additional rights of voting as compare to ordinary shareholders. But the same would be maximum up to 74%. That means, to pass any special resolution subject, 1% voting by outsiders would be required.

Enhanced Corporate Governance

Companies which have issued SR Shares will be required to comply with enhanced Corporate Governance provisions in terms of the SEBI (LODR) Regulations, 2015 i.e.

- At least ½ of the Board shall comprise of the Independent Directors irrespective of the status of the Chairperson whether Executive or Non-Executive

- 2/3rd of the Committees (excluding Audit Committee) shall comprise of Independent Directors. Audit Committee shall comprise of only Independent Directors as against present requirement of 2/3 Independent Directors.

On this background, the Nomination and Remuneration Committee will also require to increase their no. of Independent Directors from present requirement of 50% to 66% and for Stakeholder Relationship Committee from 1 Independent Director to 2/3 of total no. of Directors. The Companies which require to constitute Risk Management Committee will also be required to have the 2/3 no. Of Independent Director as against no present requirement as such.

This will ensure that promoters/founders having SR Shares will not take any biased decision beneficial to the selected class of shareholders.

Coat-tail Provisions

SEBI has defined certain circumstances under which Post-IPO, the SR equity shares shall be treated as ordinary equity shares in terms of voting rights:

- Appointment or removal of independent directors and/or auditor

- Transfer of control by promoters

- Related party transactions in terms of SEBI(LODR) Regulations involving SR shareholders.

- Voluntary winding up

- Amendment in MOA and AOA

- Initiation of a voluntary resolution plan under IBC;

- Utilization of funds for purposes other than business

- Substantial value transaction based on materiality threshold as prescribed under SEBI(LODR),2015.

- Delisting or buy-back of shares; and

- Any other provisions notified by SEBI in this regard from time to time.

By this provision, the matters which are crucial for the company’s existence and for its business have been specifically exempted from this framework of issue of SR Shares to avoid their misuse by the SR Shareholders against the interest of the Company.

Sunset Clause

The SR Shares will be automatically converted into ordinary shares after 5 years of their listing on the Stock Exchange. Company can extend their tenure further by 5 years after obtaining Shareholders’ resolution, however, the SR shareholders shall not vote on this resolution.

Even in case of demise or resignation of the SR shareholders, merger or acquisition resulting in change in control of the company, the SR Shares will be compulsorily converted into ordinary shares.

Fractional Rights Shares

Henceforth, the Issue of fractional rights shares i.e. shares with lower voting rights as compared to Ordinary Shares, by existing listed companies is not allowed. However, their need would be reviewed over a period, after starting use of issuance of SR Shares in the Market.

Conclusion

SEBI has introduced this allowance of SR Shareholding by promoters/founders of companies which are technology driven only to raise huge capital without losing the operating control. This allowance of SR Shareholding will attract the Foreign Direct Investments in the Technology Sector of India since their founders are interested in their Control and Management than gaining in the form of Dividend.

Additionally, these measures will also boost small and medium scale entrepreneurs to come out with start-up or Companies having optimum Assets, where they can attract outside funds without compromising on control or management of their venture. On the background of recent takeover of Mindtree Ltd. by L&T which was claimed as hostile, the introduction of SR Shares will be of benefit to the Stakeholders in the Financial Market.

1 comment