On 24th August 2015 The Securities and Exchange Board of India (SEBI) paved the way for the merger of Forward Markets Commission (FMC) with SEBI. According to a press release issued by SEBI, its board has cleared the norms for commodity exchanges and brokers.

About FMC

Mumbai-headquartered FMC was set up in 1953 under the Forward Contracts (Regulation) Act (FCRA) as a statutory body under the aegis of Consumer Affairs Ministry. It was brought under Finance Ministry in 2013.

In the beginning, FMC was only regulating regional commodity exchanges and its role was expanded after the emergence of a national electronic trading platform in 2000.

At present, there are three national and six regional bourses for commodity futures in the country. Together, all the exchanges clocked a turnover of nearly Rs. 60/- lakh crore in 2014-15, down from over Rs. 101/- lakh crore in the previous fiscal.

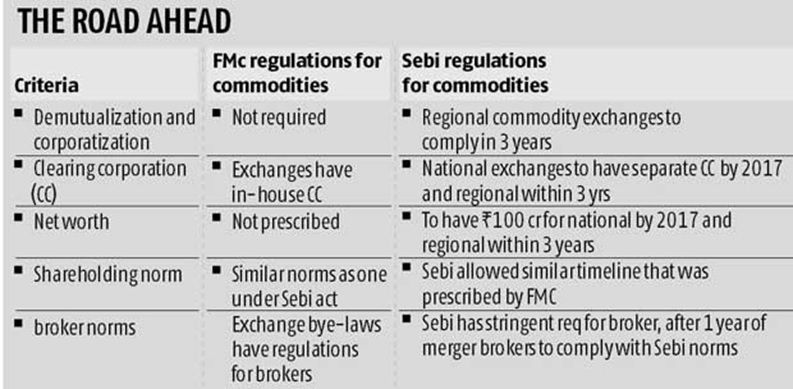

Compliances for New Regulations

The new regulations provide for compliance with Securities Contracts Regulation (Stock Exchanges and Clearing Corporations) (SECC) Regulations, 2012, which are currently required to be complied with by stock exchanges.

Major compliances include norms related to net worth, shareholding, a composition of the board, corporatisation and demutualisation and setting up various committees, turnover, and infrastructure.

To ensure non-disruptive transition, SEBI has prescribed specific timelines for aligning different provisions of the SECC Regulations:-

- Corporatization and demutualization of regional commodity derivatives exchanges – 3 years from the date of the merger.

- Availing services of a clearing corporation – 3 years from the date of the merger. Till then, clearing may continue with the current arrangement. However, the Commodity Exchanges shall ensure guarantee for the settlement of trades including good delivery.

- Net-worth – timeline as provided by FMC, i.e. May 05, 2017, for national commodity derivatives exchanges and within 3 years from the date of a merger for regional ones.

- Shareholding – timeline as provided by FMC, i.e., May 05, 2019, for national exchanges and within 3 years from the date of a merger for regional exchanges.

- Governing board norms – within 1 year from the date of a merger for national exchanges and within 3 years for regional exchanges.

- National commodity exchanges will need a net worth of at least 100/-Crores by May 2017, while regional stock exchanges have to adhere to the norm within three years of the merger.

- Commodity brokers compliant with commodity exchange bye-laws will be allowed registration with SEBI. They will have to apply within three months of a notification in this regard. The markets regulator, however, added these entities will have to comply with SEBI regulations, including on net worth and track record, within a year.

Likely Effects -Post Merger

- Commodity exchanges need to apply to Securities and Exchange Board of India (SEBI) for launching a trading segment.

- SEBI to introduce scores for consumer grievance redress at the commodity exchanges.

- SEBI will define guidelines for arbitration mechanism.

- According to sources, commodity exchanges must comply with all regulations under the Securities Contract and Stock Exchange Regulations Act, 2012.

- They will be given a deadline to adhere to the rules.

- Commodity exchanges now do not have a separate clearing corporation for contracts, a requirement under the SEBI Act. SEBI will give commodity exchanges up to three years to have separate clearing corporations.

- Commodity exchanges will not immediately receive investments from domestic or foreign investors as the Reserve Bank of India has advised SEBI to maintain the status quo pending approval from the government.

The merger of FMC with SEBI will be completed on September 28, 2015. Following this, commodity exchanges and their broker members will be regulated by SEBI, paving the way for repealing of the Forward Contracts Regulation Act, 1952, which currently governs the commodity exchanges.

A separate SEBI commodity cell has been created similar to its market regulation department. More units will be created within SEBI’s surveillance, legal and investigation departments for the commodity market.

Belying commodity market expectations, SEBI does not appear to be in favor of introducing new products, such as options and trading on indices at least for one year from the day FMC-SEBI comes into effect.

Overall SEBI’s move is in the right direction as it will eventually promote an integrated system.

{kind=link}