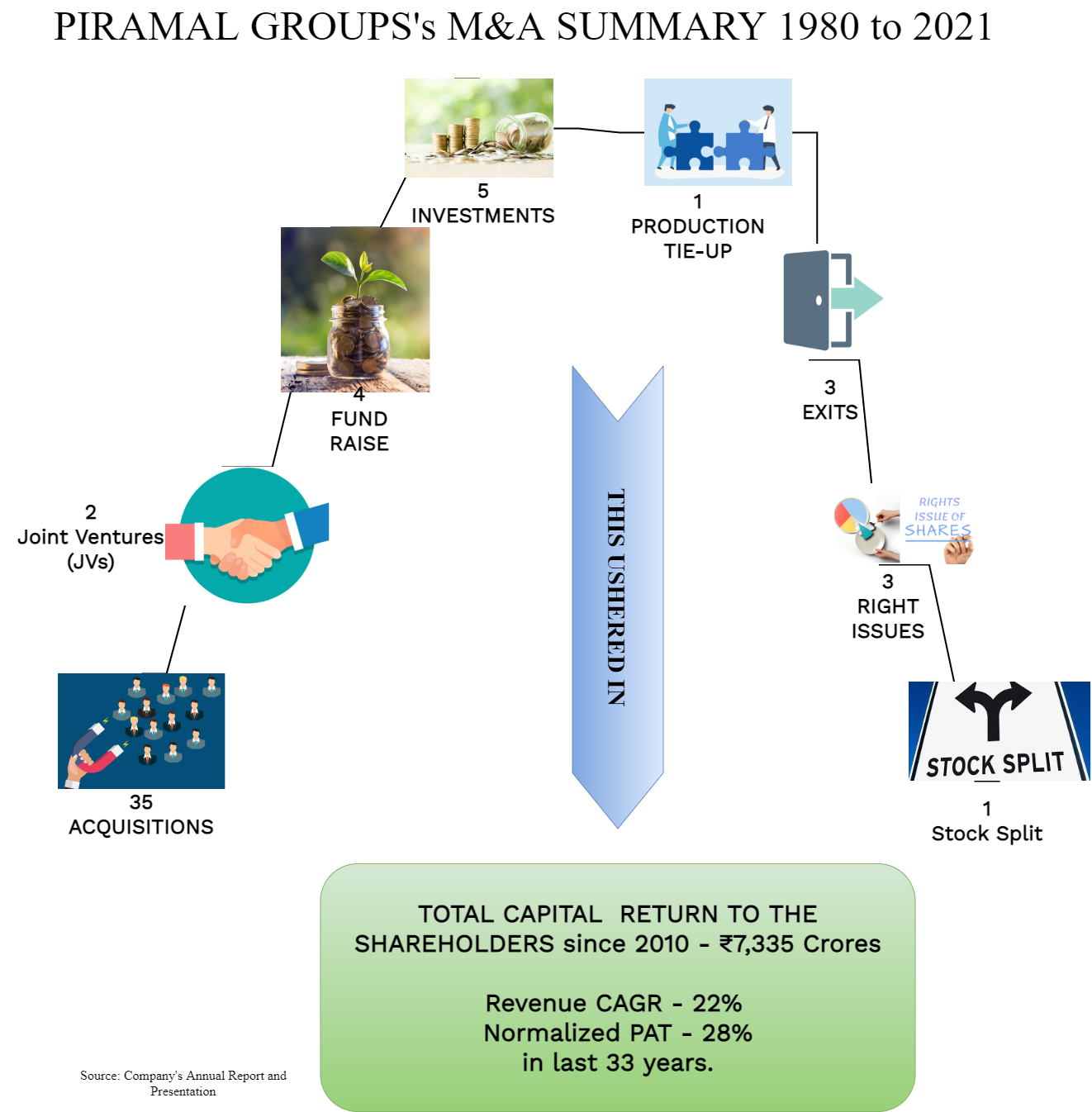

Ajay Piramal of Piramal Enterprises Ltd is an acute M&A Strategist, business savvy and smart negotiator. In the last 40 years, he created huge value for all stakeholders of Piramal Enterprises Ltd (‘PEL’, ‘Company’) by transforming the originally family business of Textiles, first into Pharma and then into Real Estate and Finance.

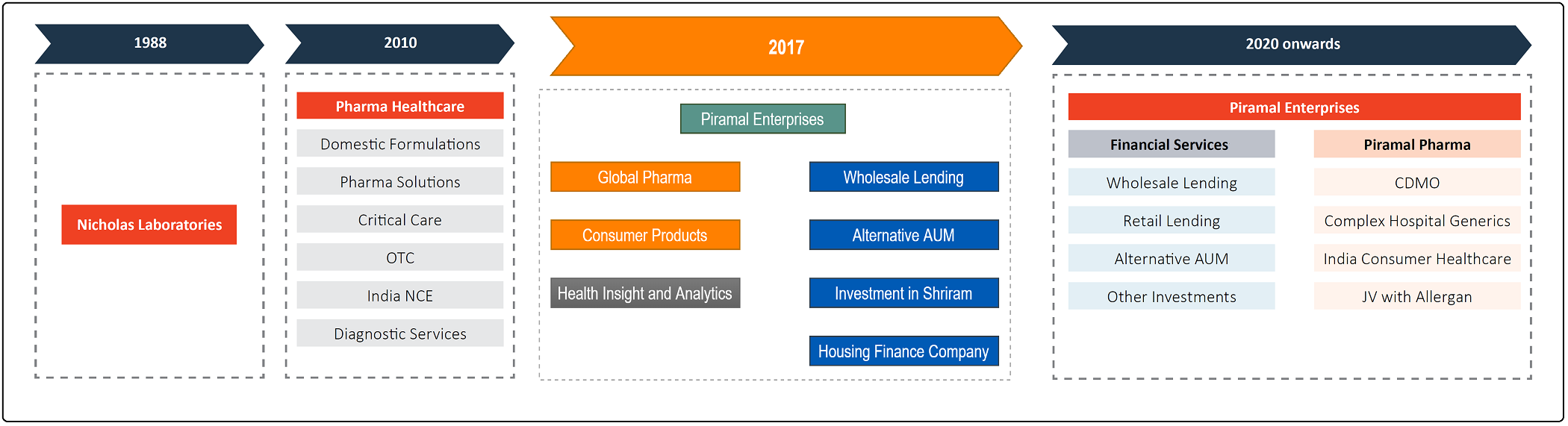

How PEL transformed from Pharma to Diversified Entity

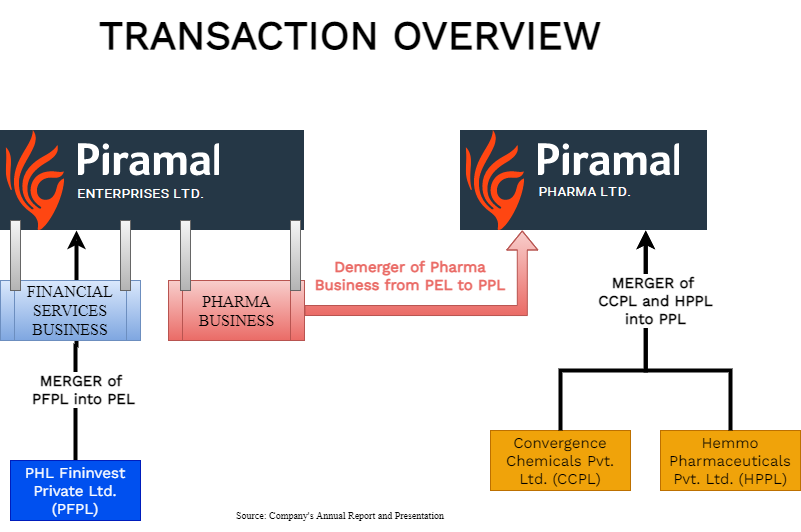

The present round of demerger into two separate focused entities started almost four years back by internal restructuring as follow: –

- Exited from non-core business of Healthcare Insight and Analytics.

- Brought Pharma business together in Piramal Pharma Limited (PPL).

- Created Separate management for both businesses.

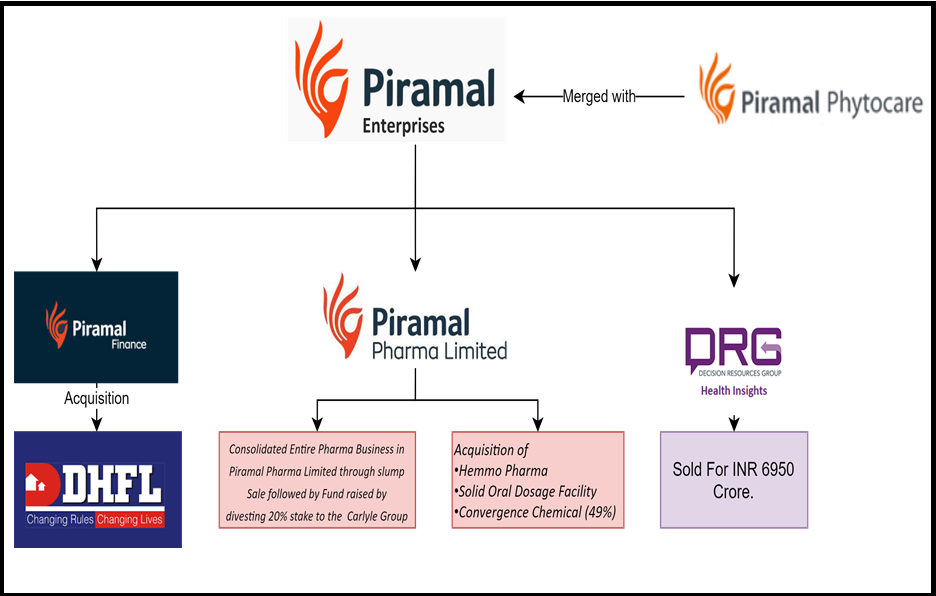

In FY 2019-20 as pre-curser to present demerger, PEL consolidated its entire pharma business through series of transactions as follow: –

- Slump sale of over-the-counter consumer healthcare products business (including the entire shareholding of the Company in Allergan India Private Limited) for an aggregate consideration of ₹ 2150 crores.

- Sale of the entire direct shareholding of the Company in: (a) Piramal Dutch Holdings N.V.; (b) PEL Pharma Inc.; and (c) Convergence Chemicals Private Limited, to PPL, for an aggregate consideration of ₹ 2,152 crores.

- Sale of the entire direct shareholding of the Company in Piramal Healthcare Inc. to PPL for an aggregate consideration of ₹ 185 crores to be discharged by way of issuance and allotment of equity shares of PPL to the Company.

The agreement date for the above tranches is 26th June 2020. PEL retains only One plant and OTC (Over the Counter) distribution business in PEL.

It further strengthened its every business as follow: –

Pharma/Healthcare Business

- Raise fund in Pharma Business from the Carlyle Group.

- Launched 15+ new products and 35+ SKUs (stock keeping units) including COVID related products.

- Leveraged technology for implementing 100% field automation and launched distributor management system.

- Invested heavily in brand building.

Financial Service Business:

- Increased product portfolio from 2 to 7 products in FY 2021.

- Expanded presence from 14 to 40 locations.

- Formed partnerships with select FinTech and Consumer Tech firms.

- Acquisition of DHFL (Dewan Housing Finance Corporation Ltd) through its subsidiary for ₹ 34,250 crores. Piramal group will pay 14,700 in cash to lenders and for balance 19,550 crores issue Non-Convertible Debentures.

- Reduction in the wholesale loan book.

Pre-Demerger Restructuring:

PEL also raised circa ₹ 18,000 crores –

By sale of

- Non-core business for ~₹6,950 crores

- Investments in Shriram Transport for ₹2,300 crores

- 20% stake in Pharma business to Carlyle Group for ₹3,523 crores.

Raising capital Through

- Preferential allotment to CDPQ of ₹1,750 crores.

- Right issue of ₹3,650 crores.

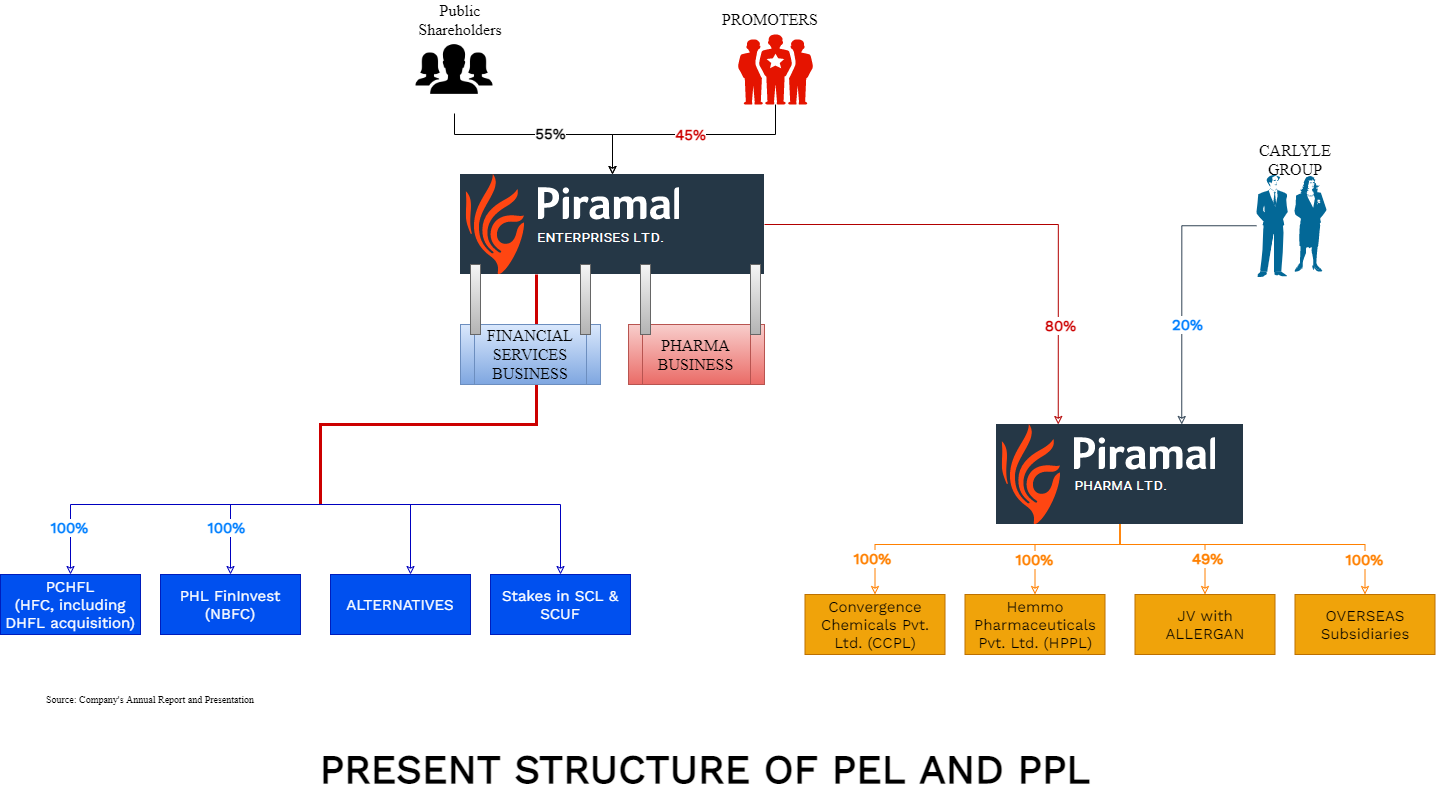

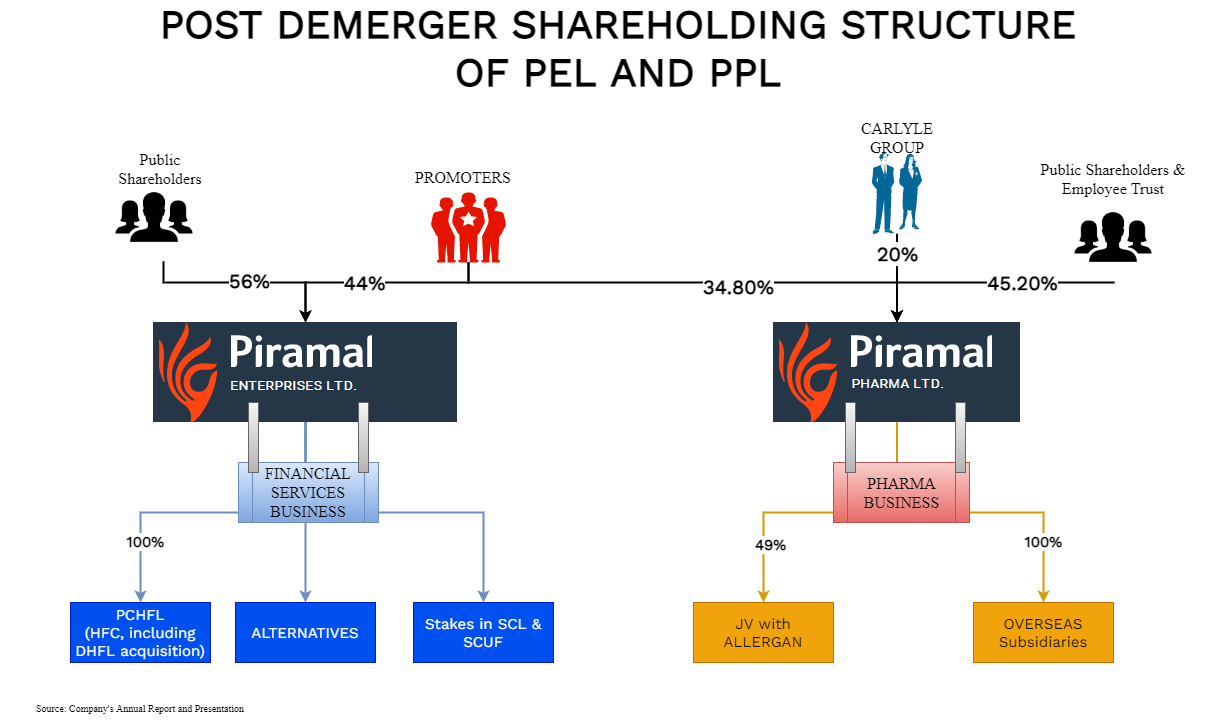

Post internal restructuring and funds raised in the last four years, the present structure of PEL is as follow:

Overview of the Companies

Piramal Enterprises Limited (‘PEL’) is engaged in the business of

- Providing financial services including retail and wholesale lending services, directly and indirectly, and

- In the pharmaceutical sector through its subsidiary, PPL, comprising

- Contract development and manufacturing organization services, ranging from discovery clinical development to commercial manufacturing of active pharmaceutical ingredients vitamins and mineral pre-mixes and formulations.

- manufacturing, selling, and distributing complex hospital generics including inhalation anaesthesia, injectable anaesthesia, intrathecal spasticity, and pain management and select antibiotics; and

- manufacturing, marketing, and distributing consumer healthcare product

Piramal Pharma Limited (‘PPL’) is primarily engaged in the business of contract development and manufacturing organization services, ranging from discovery clinical development to commercial manufacturing of active pharmaceutical ingredients, formulations; the business of manufacturing, selling and distribution of complex hospital generics including inhalation anaesthesia injectable anaesthesia, intrathecal spasticity and pain management and select antibiotics, and developing and marketing of consumer healthcare products.

Convergence Chemicals Private Limited (‘CCPL’) is Wholly Owned Subsidiary (WoS) of PPL, and it is engaged in the business of development, manufacture, and sale of specialty fluorochemicals.

Hemmo Pharmaceuticals Private Limited (‘HPPL’) is WoS of PPL, and it is engaged in the business of manufacturing and development of synthetic peptide, an active pharmaceutical ingredient.

PHL Fininvest Private Limited (‘PFPL’) is WoS of PEL and it is engaged primarily in the business of lending and investment.

The Transaction:

- The transfer by way of demerger of the Pharma Business Undertaking from PEL to PPL.

- The amalgamation of CCPL and HPPL with PPL (‘Pharma Amalgamations’).

- The amalgamation of PFPL with PEL (‘FS Amalgamation’).

The Pharma business undertaking consists of One plant and an OTC distribution business.

Rationale of the Scheme:

The scheme rationale is to simplify the corporate structure of PEL into two separate pure-play entities in Pharmaceuticals and Financial Services. both businesses have different risks and return profiled and group of investors who will be interested. Though the management was preparing for listing two businesses separately since almost the last 5 years, urgency for demerger of the pharma business could be to protect Pharma Business from leveraged Financial Services Business including the business of recently acquired DHFL through the insolvency process.

Shareholding Pattern:

Shareholders of PEL will get 4 (four) shares of the face value of ₹ 10 each of PPL for every 1 (one) share of Face Value of ₹ 2 each in PEL, in addition to their existing holding in PEL. We have arrived at likely paid-up capital and post-shareholding patterns of PPL based on the company’s presentation given to exchanges:

Carlyle Group held as on 31st March 2021 Compulsory Convertible Preference Shares (CCPS) of the face value of ₹ 10 each of ₹ 75 crores compulsorily and mandatorily to be converted into equity shares on 6th October 2021 at a price to be determined as per FEMA (Foreign Exchange Management Act) regulation. The number of shares issued on conversion is still not available in the public domain.

PEL held as on 31st March 2021 10,00,00,000 (ten crores) share warrants having face value of ₹ 10 each. Amount paid upon the same was only 0.1% and balance 0f 99.99% of the warrant price was payable by the warrant holders at the time of issue of equity shares against the warrant. The warrant was not exercisable prior to 6th October 2021. The exercise price is higher than Rs 10 or the other price as agreed between the two companies. each warrant was entitled to 1 equity share of PPL on 6th October 2021 on payment of balance amount of warrant and agreed on price. The number of shares issued on exercise of the warrants and the price at which such shares are issued is still not available in the public domain.

Financials:

Business-Wise Financials of PEL.

The above table depicts consistent growth in pharma business since FY17 and PBT have grown 400% in FY 21 from FY17.

As far as Financial Services Business is concerned, net assets have grown 2.6 times from FY17. The management systematically grew and consolidated both the vertical over a period of last decade both organically and inorganically.

We have not shown the HEALTHCARE INSIGHTS & ANALYTICS Business financials as that was exited in 2018.

Valuation:

The total valuation of PPL is circa ₹ 21,000 crores based on the issue of shares to Carlyle Group.

Taxation:

The transaction is tax neutral transaction as per section 2(19AA) of the Income Tax Act, 1961. In FY 2019-20 PEL transfer, the entire pharma business to PPL but retain only One plant and OTC distribution business in PEL. The reason for keeping this could be to satisfy the definition of Undertaking as specified in section 2(19AA).

Accounting Treatment:

The accounting treatment for the transaction is being done in compliance with appendix C of Ind AS 103. As the transaction is between common control entities.

Conclusion

Ajay Piramal built his empire less by understanding each industry deeply than thorough understanding the bigger picture of India's investing environment, and through smartly planned mergers and acquisitions. The Ajay Primal group has an excellent track record of creating value from M&A’s. In past, they did plenty of value-accretive M&A’s which has helped to grow both Financial & Pharma businesses. First time the group has acquired a loss-making company, DHFL which can be a game-changer for PEL. The latest move to have two focus entities will achieve not only liquidity for Carlyle Group and attract focus investors in each of the businesses with diverse risk and return profiles but also facilitate family separation for promoter as and when desired by swapping shares inter-se.

Add comment