-

Astral Poly Technik Limited manufacture and market the advanced CPVC plumbing system.

-

During last FY 14-15, the company acquired 80% stake of Seal IT services Ltd (UK) & 76% of Resinova Chemie Limited (India).

-

During last week, company announced it will acquire remaining 24% stake of Resinova from Mr. Vijay Parikh in cash & at same time make a preferential allotment to Mr. Vijay Parikh.

-

What is the reason for such structure instead of directly merging Resinova into Astral & How both acquisition pawing way to Astral?

THE TRANSACTION

The Board of Directors of Astral Poly Technik Ltd approved of two simultaneous but independent transactions:-

- Acquisition of balance 24% of equity share capital of Resinova Chemie Limited (Subsidiary of the Company) at a value of INR 73 Crores from Mr. Vijay Parikh. Post-acquisition, Resinova Chemie Limited will become wholly owned subsidiary of Astral Poly Technik Ltd.

- Preferential Issue of maximum 14, 04,762 Equity Shares to Mr. Vijay Parikh at INR 420/- per share or at a price determined by Chapter VII of SEBI ICDR Regulations, whichever is higher.

ACQUIRER COMPANY: – ASTRAL POLY TECHNIK LIMITED (ASTRAL)

Astral Poly Technik Limited was established in 1999 with a single-minded purpose to manufacture absolutely the best plumbing & drainage system in India. Today, Astral offers one-stop solution for various piping requirements such as Plumbing (Hot & Cold), Drainage, Underground, Rain water harvesting, Sewage, Industrial, Fire Sprinklers, Agri Pipes etc.

Astral Poly Technik Limited is the first licensee of Lubrizol of USA and has equity joint venture with Specialty Process LLC of USA to manufacture and market the most advanced CPVC plumbing system.

In the year 2007, the company came out with an IPO. Today its shares are listed on both BSE and NSE.

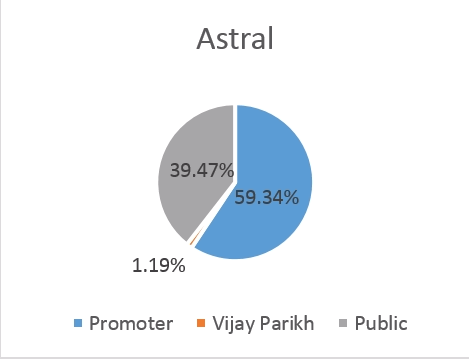

Pre- preferential allotment Shareholding Pattern

TARGET COMPANY I: – SEAL IT SERVICES LIMITED (SEAL IT)

Seal IT is in the business of manufacturing of comprehensive range of sealants, adhesives, building chemicals and allied products under the brand name “Bond-it”. Manufacturing facility of Seal IT is situated at Elland, UK. The main customers are Builders, Merchants, DIY, Sealant Applicators, Roofing Contractors, Roofing Distributors, Industrial Bitumen Manufacturers / Flooring Contractors, Flooring Distributors, Carpet Shops, Architects/Council Export/Wholesalers and Cash & Carry. Presently, Seal IT is exporting its products throughout Europe, Africa and Middle East.

TARGET COMPANY II: –RESINOVA CHEMIE LIMITED (RESINOVA)

Lead by Mr. Vijay Parikh, Resinova is in the business of manufacturing and marketing highly diversified range of adhesives and sealants and allied products under the different brand name viz. “Bondtite”, “Resibond”, “Bondset”, “Solvobond”, “Vetra”, “Brush bond” and “Zesta” etc..The company has two manufacturing facilities located in Kanpur. Resinova’s supply chain network consists of 11 branch offices and more than 1,700 channel partners reaching out to around 4,00,000 retail outlets across India. Resinova is amongst the leading players in epoxy adhesives sector in India.

CURRENT TRANSACTION

The Board of Directors of Astral in its meeting held on 17th September, 2015 decided to acquire balance 24% equity stake in Resinova owned by Mr. Vijay Parikh on terms and conditions as per the Share Purchase Agreement (SPA) executed on 17th September, 2015.

On the same day, both the parties also executed Share Subscription Agreement (SSA) whereby Mr. Vijay Parikh agreed to subscribe to 14,04,762 equity shares of the Company at a price of Rs. 420 or at a price determined by Chapter VII of SEBI ICDR Regulations, whichever is higher.

INR in crore

| Particulars | Amount |

| Consideration paid to Mr. Vijay Parikh for acquisition of Resinova | 73 |

| Amount to be received from Mr. Vijay Parikh from preferential allotment | 59 |

The company probably does not want to mix its adhesive business operation with Resinova in the immediate future. Mr. Vijay Parikh will continue to be Managing Director of Resinova so the company will continue its growth under his control. Thus instead of merging Resinova, Astral is preferring to have 100% acquisition.

Post Preferential Allotment shareholding Pattern

RATIONALE

ASTRAL

Substantial Presence in Adhesive Business

Acquisition of these two entities will resultantly strengthen Astral’s adhesive business. After the acquisition, Astral total adhesive business crossed INR 300 crores.

Comprehensive Product Portfolio

Post-acquisition Astral will have a presence across all categories including epoxy putty, epoxy adhesive, silicon sealants, solvent cement & cyanoacrylates.

Expansion of its network

Resinova’s 1,700 channel partners will help astral to expand its foot print in North & West India. Seal IT will help Astral to expand its presence in Europe, Africa and Middle East. In future astral can use this network to sell its plastic products also.

VIJAY PARIKH

Mr. Parikh’s post allotment stake in Astral will go up to 1.19%. He will get entry to other product portfolio of Astral. As he will continue to be Managing Director of the Resinova, day-to-day operations of Resinova will remain under his control only.

FINANCIAL

INR in crore

| Particulars | Plastic Products | Adhesives |

| As on 31st March 2015 | ||

| Revenue* | 1207 | 255 |

| EBIT | 122 | 10 |

| EBIT Margin | 10.10% | 3.92% |

| Net Assets* | 526 | 120 |

*:- figures are excluding eliminations.

| Particulars | Resinova | Seal IT | Astral

(Standalone) |

Astral

(Consolidated) |

| As on 31st March, 2015 | ||||

| Revenue | 203 | 138 | 1253 | 1430 |

| EBIT | 15 | 7 | 117 | 132 |

| EBIT Margin | 7.38% | 5.07% | 9.33% | 9.23% |

| PAT | 9 | 6 | 68 | 76* |

| Net Profit Margin | 4.43% | 4.34% | 5.42% | 5.31% |

| EPS | 23.19 | NA | 6.03 | 6.64 |

| Fixed Asset# | 22 | 22 | 305 | 368 |

| Fixed Asset Turnover Ratio | 9.23 | 6.27 | 4.10 | 3.88 |

*:- After minority adjustment. #:-Excluding intangibles

VALUATION

| Particular | Resinova | Seal IT | Astral

(Consolidated) |

| Enterprise Value | 287.64# | 69.3# | ~5227 |

| EV/EBIT | 19.18 | 9.90 | 39.59 |

| EV/Sales | 1.42 | 0.50 | 3.65 |

| Price/Book value per share | 6.59 | 3.28 | 8.24 |

Above figures are subject to error. #:-Source Company Presentation

EV:- Market Cap+ Debt- Cash & Cash Equivalents

CONCLUSION

EBIT margins of both Resinova & Seal IT are more than Astral’s Adhesive Business. Further distribution network is another reason behind the whopping consideration. Astral can use distribution network of these two companies for selling its high margin plastic product, thereby increasing its overall profit.

{kind=link}

{kind=link}