Recently NCLAT approved the scheme of arrangement of Reliance Jio Infocomm Limited (Jio Infocomm) and ‘Jio Digital Fibre Private Limited’ (Jio Fibre) and ‘Reliance Jio Infratel Private Limited’ (Jio Infratel) and their respective shareholders and Creditors. Scheme was previously approved by the NCLT which was challenged in the upper court “NCLAT’ by Income Tax dept, objections of tax department were eventually rejected by the NCLAT.

Scheme Details:

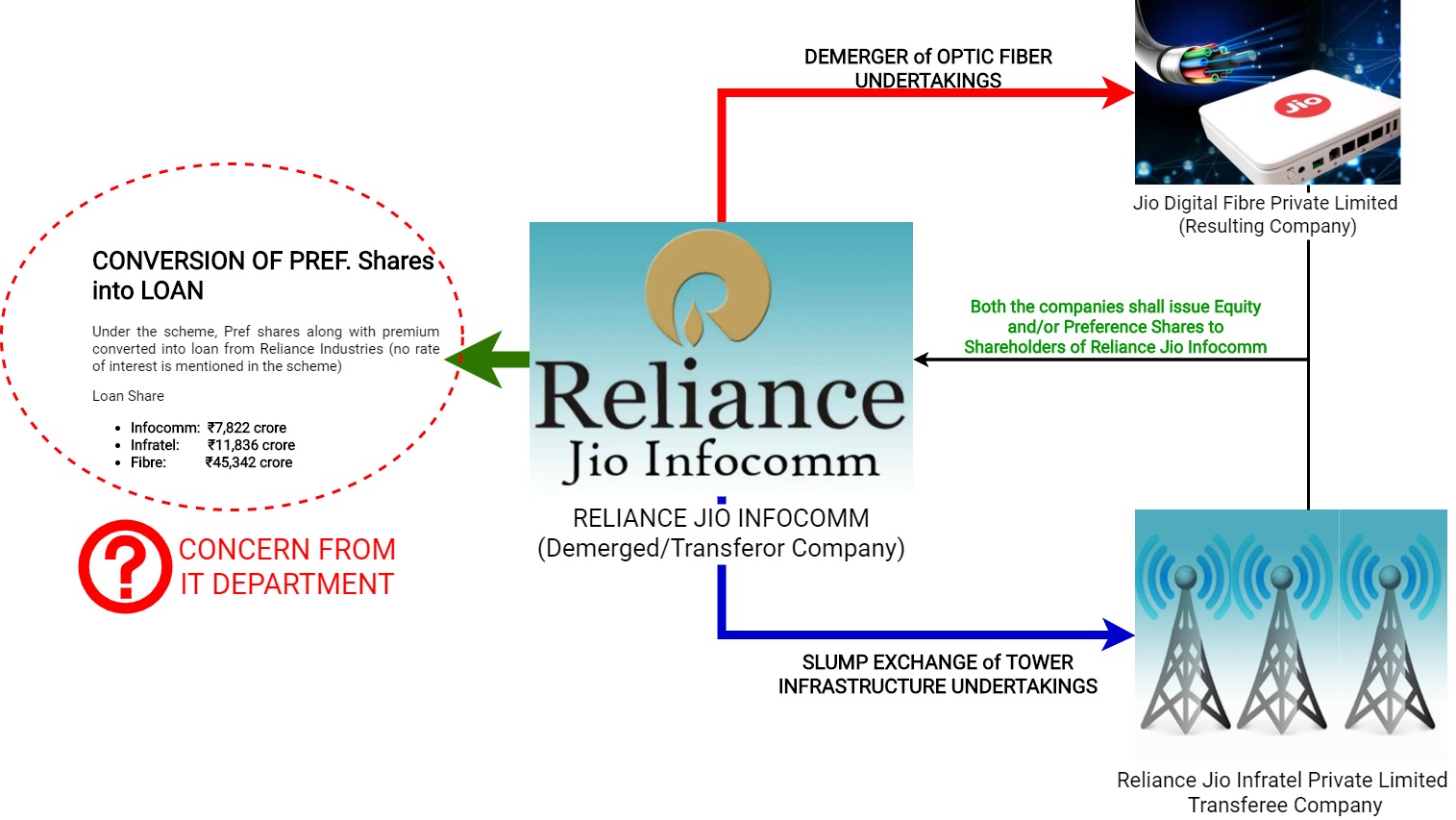

There were three different arrangements entered through the scheme, are as follows:

- Demerger of Optic fibre undertaking of Jio Infocom into Jio Fibre

- Slump Exchange of Tower infrastructure undertaking of Jio Infocom to Jio Infratel

- Arrangement with the shareholders of Demerged Company i.e. Reliance Jio Infocom for conversion of Preference share including premium (aggregating to Rs. 65,000 crores) into loan.

The Department raised objections in relation to the third arrangement envisaged through the scheme.

Transaction Overview:

Major concern/Question raised by IT Department:

As per the scheme, preference share capital and corresponding share premium (aggregating to Rs. 65,000 crs) would be cancelled and converted into an equivalent amount of loans from ‘Reliance Industries Ltd.’ And as part of the scheme allotted to three different undertakings i.e. to Jio Infocom Limited -Rs.7,822 crores, Jio Fibre – Rs.45,342 crores and Jio Infratel -Rs. 11,836 crores.

Such conversion is not as per provisions and in violation of Sec 55 (Issue and redemption of preference shares) and Sec 52 (Application of Premiums Received on Issue of Shares) and Sec 66 (Reduction of share capital) of the Companies Act, 2013.

Objections to non-compliance with the provisions of the Companies Act,2013 should have been raised by Registrar of Companies through Regional Director, surprising they did not raise any objections in the affidavit filed by them.

As a result of the conversion of preference shares into loan, the Scheme will result in Tax avoidance and loss of revenue to the government:

Tax Department argued that the conversion of preference shares along with premium will substantially reduce the profitability of Jio Infocomm and will act as a tool to avoid and evade taxes.

Further, it would also bring down the payment of dividend distribution tax (conversion of preference shares into loan and indirect release of the asset) which is again a way to avoid payment of taxes.

NCLAT reply on the Income tax queries:

- On question of Companies Act violation:

Whether any scheme is compliant of Section 55 of the Companies Act or not can be better examined by authorities under the Companies Act. It can be noticed and objected by the Competent Authorities i.e., Regional Director, North Western Region and the Registrar of Companies. And no observation regarding violation of Sec 52, 55 or 66 is made by the concerned authority. So NCLAT did not take objections by the Income Tax Department in consideration.

- On Tax avoidance and loss of revenue to the Government:

Without going to the record and without placing any evidence or substantiate the allegation by appearing before the Tribunal, it was not open to the Income Tax Department to hold that the Composite Scheme of Arrangement is giving undue favour to the shareholders of the company and results into tax avoidance.

The Income Tax Department, which sought for liberty to enquire into the matter, if any part of Scheme amounts to tax avoidance or is against the provisions of the Income Tax has been granted liberty take appropriate steps if so required in the course of income tax assessment proceedings under The Act.

Mere fact that a Scheme may result in reduction of tax liability does not furnish a basis for challenging the validity of the same.

Modification in the scheme:

Petitioner Companies modified the scheme to the effect that the Resulting Company (Jio Fibre) and the Transferee Company(Jio Infratel) shall provide an option to the shareholders of the Demerged Company (Jio Infocomm) and to the TransferorCompany (Jio Infocomm), at their discretion, to receive a part of the consideration in the form of preference shares, for demerger of Demerged Undertaking and transfer of the Transferred Undertaking respectively. It is further submitted that the aggregate consideration envisaged under the Scheme does not undergo any change pursuant to the aforesaid amendment.

Consideration:

We have taken consideration paid during the arrangement from the Mar-19 balance sheet of the respective companies

Demerger

Paid to the Equity shareholders

| Particulars | Consideration | FV | No. of Shares issued to Jio Infocomm shareholders in Jio fibre(In Crs) | Value (in Crs) |

| Class A -Eq. Share of Jio Fibre | 1 share for 9 shares | 1 | 500 | 500 |

| 10% Cumulative, Participating and Optionally Convertible preference shares | Diff b/w the value of the assets recorded in the books of JDFPL and book value of the assets transferred to JDFPL | 10 | 7,814 | 78,139.67 |

| 83,139.67 |

| Particulars | Nos | FV | No. of Shares in Jio Fibre on demerger | Value (in Crs) |

| Redeemable Preference share | 1 share for 100 shares | 10 | 12,50,000 | 1.25 |

Slum Exchange

Consideration will be Issued by Jio Infratel to Jio Infocomm

| Lump Sum consideration | Nos (in Crs) | FV/share | Value (in crs) |

| Class A -Eq. Shares | 200 | 1 | 200 |

| Class B -Eq. Shares | 5 | 10 | 50 |

| Transferee Company NewShares | 250 |

Other Points:

- Super-Fast Approval of the scheme (Board Meeting – 11/12/18, Shareholders & Creditors Approval – 18/02/2019 & NCLT order approving scheme -20/03/2019)

- First, preference shares are converted into loan liability and then both the arrangement (demerger and slump exchange) are executed so that loan apportioned to respective undertaking can be transferred.

- During the year 2018-19, Jio Infocomm and Jio Infratel shifted their registered office from Maharashtra to Gujarat (Jio Fibre is having its registered office in Gujrat only). This shifting of office is possibly done to save the stamp duty cost on demerger and slump exchange transaction and/or to get the faster scheme approval.

- As mentioned in the Mar-19 B/s of Jio Infocomm that all assets and liabilities pursuant to the arrangement (demerger & slump exchange) are transferred vested with respective companies, at their carrying values, on a going concern basis with effect from 31st March 2019. Jio Fiber has recorded Fiber undertaking assets at fair value which is higher by Rs. 64,208 crores in its books.

- Post transfer of fibre business undertaking and tower Infrastructure undertaking, Jio Infocomm will be left with digital service undertaking.

- Total non-current liabilities of Fibre undertaking transferred to Jio Fibre is Rs. 71,755 crs, out of which Rs. 45,342 crs pertains to conversion of preference share (including premium) into loan and remaining liabilities is other borrowings.

- Debt-Equity & Current Ratio:

| Particular | Jio Infocom | Jio Fibre | Jio Infratel |

| Debt Equity Ratio | 1.80 | 1.74 | 83.30 |

| Current Ratio | 0.22 | 0.17 | 0.20 |

Comments/Analysis:

Whether conversion of preference shares into loan is as per the provisions of Sec 55 of companies Act?

There is no specific provision in the Companies Act, 2013 which deals with the conversion of preference shares into loan, though section 55 deals with Issue and redemption of preference shares, but in given section it does not mention anywhere that preference shares can be converted into loan or any option is available to redeem / cancelation / convert such preference shares into loan. So, such conversion does not fall within the preview of Sec 55.

Whether Securities Premium can be converted into loan (Sec 52)?

Application of securities premium money (Sec 52) does not mention that securities premium can be converted into loan or its utilisation by way of conversion into loan.

Whether cancellation/conversion of preference share will amount to capital reduction as per Sec 66?

Cancellation and conversion of preference shares into loan is reduction of preference shares and similarly transfer of credit to Share premium account to loan is also reduction of share capital without complying the condition of Sec 66.

How scheme got approved, even though apparently it is in violation of companies act?

NCLT while approving the scheme of compromise and arrangement must look whether such scheme is not found to be violative of any provision of law and is not contrary to public policy.

Even though there were no objection raised from the Regional Director regarding violation of any companies act section, but prima facie it does look like that conversion of preference shares along with the premium amount into loan is violation of sec 55, 52 and sec 66 (reduction of capital), NCLT / NCLAT on its own should have looked into these provisions and provided clarity on compliance of these sections by the Jio Infocomm.

Contention raised by the Income Tax

Why Income tax went against cancellation of entire scheme instead of just cancellation of conversion of preference shares into loan which they believe is in contravention of provisions of law even though there were no objections raised with the demerger and slump exchange transaction.

Commercial implications:

One other way to look at the composite scheme is even if Income tax department does not accept the scheme for income tax computation, in terms of books ownership of both capital intense and assets heavy businesses of fibre and towers will be financed and owned by Reliance group with meagre capital infusion and in reality all equity required for both will be financed by the incoming partners. if one considers the difference between book value and fair value recorded by Jio Fibre getting credited to preference shares, then practically Reliance group will hold such huge assets with negative equity capital.

Conclusion:

Conversion of preference share including premium into loan is concerned it is still not clear how the provisions of Companies Act are complied with and how it is not a violation of relevant section of redemption of preference shares, utilisation of securities premium and reduction of capital. Since no questions were raised by the ROC regarding conversion violation, they have somehow failed in their responsibility of making sure the scheme comply with the provisions of the Companies Act.

As far as the Income Tax department is concerned, they should not have raised objection pertaining to violation of companies Act, since it is outside of their domain, and in case scheme violates any provisions of Income Tax Act, they can always take necessary action even after the scheme is executed.

Pritam Sangwan

You may also like

Add comment