Vadilal Industries Limited (“VIL”) has long been synonymous with India’s ice‐cream market. In March 2025, the promoters of VIL—the Gandhi Family—finally resolved their intra‐family disputes and announced a comprehensive restructuring of both governance and corporate entities. Alongside a family arrangement to strengthen board independence and funding frameworks, VIL has approved a composite amalgamation (“Scheme”) to consolidate several promoter‐held entities—including Vadilal International Private Limited (“VIPL”), Vadilal Finance Company Private Limited (“VFCPL”), and Veronica Constructions Private Limited (“VCPL”)—into VIL.

One notable omission, however, is Vadilal Enterprises Limited (“VEL”), a listed sister company that acts as VIL’s exclusive distributor. Although VEL purchases virtually all of its ice‐cream inventory from VIL, the Gandhi Family has chosen not to include VEL in the current merger scheme.

Vadilal Industries Limited (“VIL” or “Transferee Company”) is engaged in the business of manufacturing, sourcing, processing, distribution and marketing of ice-cream, flavoured milk, frozen dessert, juices, milk lollies, milk ice, ice candies, ice lollies and other dairy products, and processed foods such as frozen fruits, vegetable pulp, ready-to-eat and ready-to-serve products. The equity shares of VIL are listed on the BSE Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”).

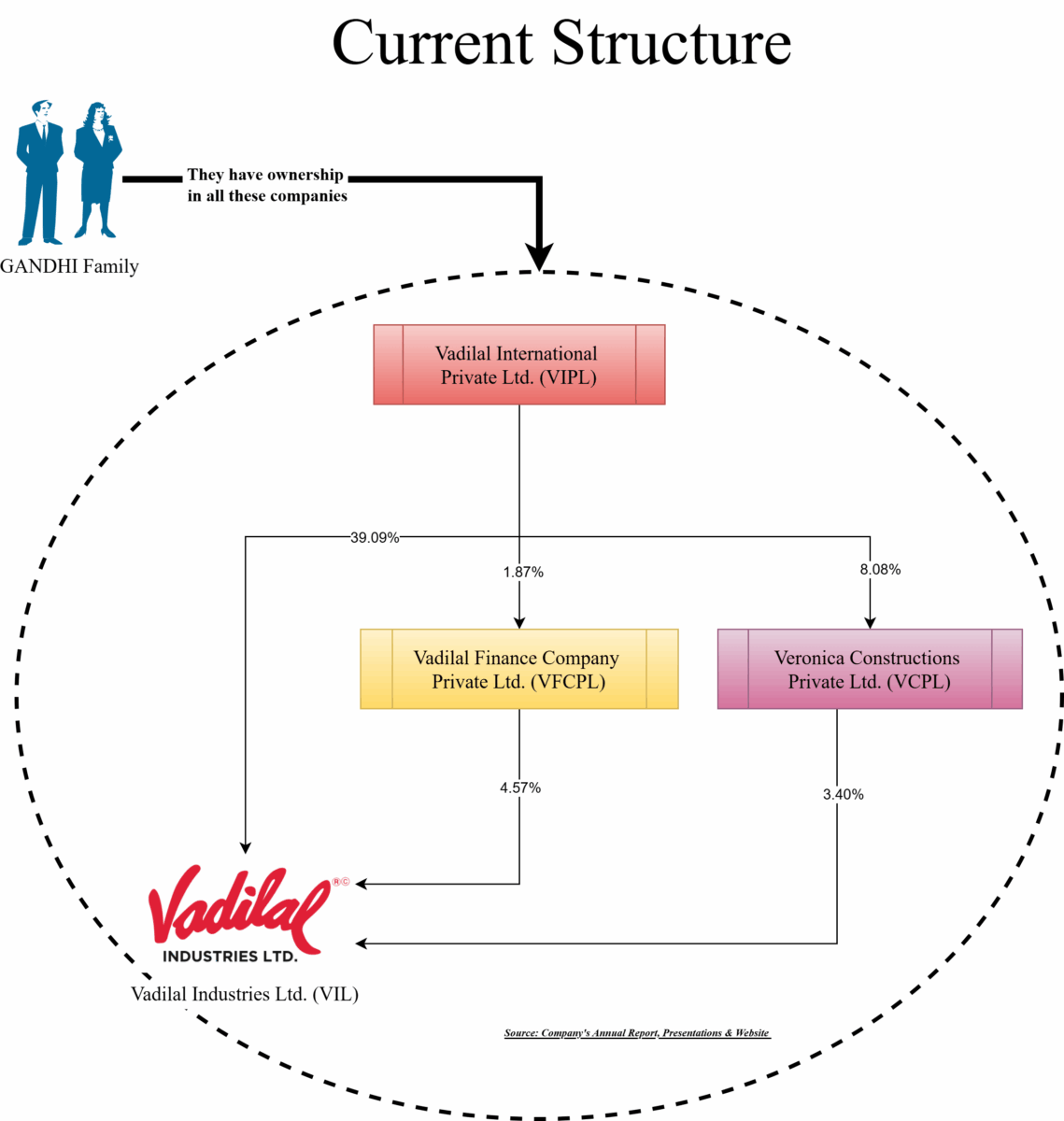

Vadilal International Private Limited (“VIPL” or “Transferor Company 1” is owned by the Gandhi Family and is engaged in the business of leasing non-financial intangible assets and is the owner of the intellectual property rights of the brand “Vadilal”. VIPL owns 39.09% equity stake in VIL 1.87% equity stake in VFCPL and 8.08% stake in VCPL.

Vadilal Finance Company Private Limited (“VFCPL” or “Transferor Company 2”) is also owned by the Gandhi family and is inter-alia engaged in trading activities. However, as per the latest financials, VFCPL has minuscule revenue. VFCPL owns 4.57% equity stake in VIL.

Veronica Constructions Private Limited (“VCPL” or “Transferor Company 3”) is also owned by the Gandhi family and is engaged in the business of development & construction activities, and trading activities. However, as per the latest financials, VCPL has minuscule revenue. VCPL owns 3.40% equity stake in VIL.

VCPL & VIPL also entered into a share purchase agreement with other Gandhi group companies to transfer their stake in Vadilal Chemicals Limited, thus making these companies hold only a stake in VIL, the brand and investment in other transferor companies.

Family Arrangement to resolve long-standing feud:

Members of the promoters and promoter group of VIL: Mr. Rajesh R. Gandhi, Mr. Janmajay V. Gandhi and Mr. Devanshu L. Gandhi, heads of the respective family branches of the Gandhi family (“Gandhi Family™”), executed a memorandum of family arrangement (“Agreement”).

Pursuant to the family settlement, the Gandhi Family has agreed to settle their inter-se disputes, and is desirous of restructuring the management of VIL to:

- maintain equality of interests and participation of all the promoters while maximizing shareholder value, and

- to establish a more robust framework of corporate governance by appointing independent professional management personnel for the management of the business and operations of VIL. Further, in view of the significance that the brand “Vadilal” holds in the business operations of VIL, the promoters are also desirous of housing the ownership of the brand within VIL, which is currently used by VIL under a non-exclusive license, for a limited period, from a promoter group entity. This will enable VIL to secure continued use of the brand, which will in turn enable it to sustain its strong market presence and seamlessly meet consumer demand, safeguard the interests of, and maximise the value for all stakeholders of VIL.

Key Terms of Family Arrangement / Governance Framework

Board of directors of the Company:

- Each of the three family branches of the Gandhi Family Members (each “Branch™) will have the right to appoint 1 director to the board of directors of the Company (“Board”) (“Nominee Directors™) (out of a total of at least 7 directors, such that majority of the Board is constituted by directors not being members of the Gandhi Family and/or any of their nominees).

- Apart from the above, the Board will have 4 non-executive directors (not being the Nominee Directors), including at least 3 independent directors appointed in accordance with applicable law and as per the policy for appointment of independent directors adopted by the Company.

- Each committee constituted by the Board will have 1 Nominee Director from among the Nominee Directors on the Board on a rotational basis to ensure equitable representation of each Branch on each committee of the Board.

- Each Branch also has the right to equal representation on the boards of directors of all subsidiaries of the Company.

Future funding requirement:

- The Company will be required to follow a waterfall mechanism in the event the Company needs further funding in the following manner.

- First, through the internal accruals of the Company and/or debt borrowings, second, through a rights issue to the existing shareholders of the Company, subject to the unanimous consent of each of the Branches and third, through a preferential allotment, subject to consent of the Branches.

Affirmative voting matters:

- The Gandhi Family Members have affirmative voting rights in relation to certain matters affecting their shareholding and interests in the Company including, any corporate restructuring of the Company and/or its material group companies, any decisions in relation to the brand ‘Vadilal’, change in the capital structure of the Company or issuance of fresh securities, creation of joint and several liability directly on the promoters of the group companies, any delisting of the securities of the Company, liquidation or winding up of the Company or any of its material group companies, etc.

Appointment/re-appointment/removal of independent directors, CEO, CFO and other key managerial personnel of the Company:

- The Gandhi Family Members have a right to identify and recommend candidates for appointment as the independent directors, CEO, CFO and other key managerial personnel of the Company as per the eligibility criteria and manner of appointment as set out under the policy for appointment of independent directors and/or the policy for appointment of professional ~ management personnel, as applicable, as adopted by the Company. Any appointment, re-appointment and/or removal of independent directors and professional management personnel will require the unanimous consent of each of the Branches.

Transfer restrictions on Gandhi Family Members:

- Right of First Refusal: Each Branch has a right of first refusal in case a Gandhi Family Member of any other Branch intends to transfer shares of the Company to a third-party purchaser.

- Tag Along Right: In case of transfer of shares of the Company, by one Branch to a third party, where pursuant to such transfer the third party purchaser acquires an aggregate of more than 10% of the total paid-up share capital of the Company, the other Gandhi Family Members have a tag along right against such third party purchaser in case of transfer by the third party purchaser to a competitor of the Company.

Scheme of Arrangement

The Vadilal group also approved of a composite scheme of amalgamation (“Scheme”) for the merger of the following promoter/promoter group entities of VIL with VIL:

- Vadilal Finance Company Private Limited (“VFCPL”);

- Veronica Constructions Private Limited (“VCPL”); and

- Vadilal International Private Limited (“VIPL”).

Essentially, through an amalgamation scheme, Vadilal group will consolidate the “Vadilal” brand into VIL and most promoter holdings in VIL are currently held through promoter entities which due to the merger shall usher in direct holding by the promoters.

Rationale for the merger as envisaged under the scheme:

All intellectual property in relation to the brand ‘Vadilal’ (“Brand”) is currently held by VIPL. The Brand is core to VIL’s business operations. VIL is currently using the Brand under a non-exclusive licensing arrangement with VIPL, which is due to expire in the year 2028. It is essential for VIL to secure the right to continuous use of the Brand for adapting to evolving consumer needs with agility and maximizing value for all stakeholders.

Accordingly, the proposed Scheme seeks to integrate the ownership of the Brand with VIL, which will result in inter alia the following benefits:

- eliminating the complexities arising from licensing of the Brand by streamlining the ownership of the Brand within the Transferee Company;

- enhancement of stakeholder value, and benefit to public shareholders of the Transferee Company, by ensuring direct and undiluted economic ownership of the Brand, a key intangible asset for the Transferee Company; and

- cessation of payment of royalties by the Transferee Company will positively impact the earnings and profitability of the Transferee Company, thereby contributing to the growth of operations of the Transferee Company.

The proposed amalgamation will result in streamlining and alignment of the shareholding of the promoter and promoter group of the Transferee Company which is held through multiple entities belonging to the promoter and promoter group of the Transferee Company and thereby result in simplification of the group structure by eliminating multiple companies and shareholding tiers, thus enabling focus on core competencies and resulting in efficiency of management, significantly contributing to future growth and maximising value for all stakeholders.

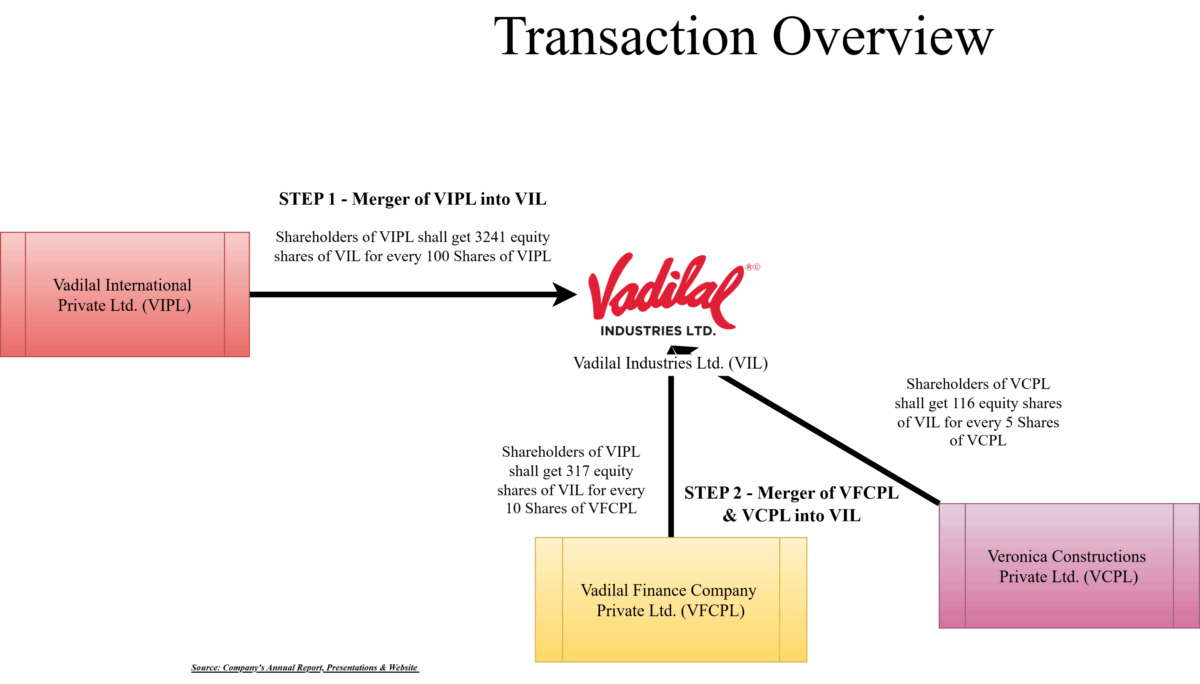

The “Appointed Date” for all mergers means the 1st day of April 2025 or such other date as may be approved by the Tribunal or any other Appropriate Authority. However, the merger shall be given effect in the following chronology:

- Merger of VIPL with VIL

- Merger of VFCPL & VCPL with VIL

The major reason for dividing mergers into two sub-parts and giving effect to VIPL merger first could be as VIPL holds investments into VFCPL & VCPL which shall transfer to VIL first and then get cancelled.

Share Capital & Swap Ratio

Swap Ratio

| For merger of VIPL into VIL | 3241 equity shares of VIL for every 100 shares of VIPL |

| For merger of VFCPL into VIL | 317 equity shares of VIL for every 10 equity shares of VFCPL |

| For merger of VCPL into VIL | 116 equity shares of VIL for every 5 equity shares of VCPL |

Pursuant to the merger of VIPL, which mainly has brand and equity investments in VFCPL and VCPL, VIPL will issue significant shares to promoters. On the consolidation of VFCPL and VCPL, equity shares held by them in VIL will get issue to the promoters directly.

Valuations

Valuation assigned to VCPL & VFCPL is aligned with their holding in VIL. For VIPL, the incremental valuation of around INR 1000 crore pertains to the “Vadilal” brand.

The shareholders of VIL have through e-voting ended on January 14, 2023, approved a resolution for the purchase of “VADILAL” brand for consideration not exceeding ₹ 676 crore plus taxes from VIPL. However, thereafter, no substantial progress has happened in the same. Finally, the brand is now getting transferred at almost 40% premium.

Royalty paid by VIL in the last 3 years

INR in lakhs

| Particulars | FY 2024 | FY 2023 | FY 2022 |

| Royalty Paid | 84 | 57 | 47 |

One really needs to ponder whether assigning a valuation of INR 1000 crore for a brand on which VIL pays a yearly royalty of less than a crore justifies.

Consolidated Financials for VIL

INR in Crore

| Particulars | FY 2025 | FY 2022 |

| Revenue | 1255 | 698 |

| PAT | 150 | 45 |

With increasing demand and streamlining of promoter control, VIL is likely to have a brighter future and margins.

Vadilal Enterprises Limited – Keeping it separate

Vadilal Group has another listed company named Vadilal Enterprises Limited. The company is not engaged in any manufacturing activity sells ice-cream bought from VIL and sell. Basically, acts as a distributor to VIL.

| Particulars | H1 FY 2025 | FY 2024 | FY 2023 |

| Sales | 760 | 999 | 930 |

| Purchase of Stock in trade | 553 | 776 | 756 |

| Purchase of Goods from VIL | 523 | 736 | 716 |

The crucial point to ponder is why Vadilal Enterprises Limited is also not getting consolidated with VIL as part of streamlining the structure? At first glance, merging VEL into VIL might appear logical—after all, VEL’s FY 2024 sales of ₹999 crore rely almost entirely on stock procured from VIL. However, there could be different commercial reasons like promoter stake in only 51% in Vadilal Enterprises Limited, valuation which is circa ₹1,000 crore compared to a yearly PAT less than INR 10 crore.

Conclusion

Vadilal’s post-feud restructuring is a bold step toward long-term value creation. The direct ownership of the brand within VIL, simplification of group structure, and enhanced board governance collectively mark a new chapter for the company and for promoter family.

While the exclusion of VEL from the current scheme leaves room for future consolidation, the current strategy clearly prioritizes brand integration and promoter alignment. In a competitive market that now includes large players like Hindustan Unilever which is also announced demerged of its ice cream business, Vadilal’s renewed focus on structure and scalability may offer the right scoop of success.